The US has a particularly punitive tax regime on individuals. Not only are they taxed on their worldwide income but even if they move abroad they are still taxed. Even if you renounce your US citizenship there is a big expatriation tax to pay. They used to try to collect tax for another ten years...

By contrast, companies are only taxed on the profits they earn within the US and can employ all kinds of strategies to reduce tax by earning profits offshore. Though I am against double taxation of income (taxed at corporate and then again at individual level) this kind of lopsided tax regime is unfairly taxes different companies at different rates and makes the whole tax system look manifestly unfair.

Sunday, April 29, 2012

Saturday, April 28, 2012

Government Wimps Out and Makes Super More Complicated

So the government will increase the superannuation contributions tax to 30% but only for people who earn more than $300k per year. This is said to reduce the budget deficit by $1 billion. But if there are only 128,000 people earning more than $300k per year the total is:

128,000*$25,000*.15 = $480 million

To get to $1 billion you either have to assume that they are all over 50 with less than $500k in super in their accounts, or use 30% by mistake in the calculation. So everyone from $180k to $300k per year in income will get a 30% concession and those of us earning between $80k and $180k will get a 23% concession. But those earning more than $300k only a 15% concession. Of course, this doesn't make a lot of sense and makes super more complex. It would make much more sense to abolish the concessional tax on contributions and if that is too severe an increase in tax also cut the rate on superannuation earnings a little. This would make the system much simpler by getting rid of the distinction between concessional and non-concessional contributions, salary sacrificing etc. Of course, Labor is still hoping that public servants and maybe some others earning between $80k and $300k a year will still vote for them. So they haven't raised their tax.

128,000*$25,000*.15 = $480 million

To get to $1 billion you either have to assume that they are all over 50 with less than $500k in super in their accounts, or use 30% by mistake in the calculation. So everyone from $180k to $300k per year in income will get a 30% concession and those of us earning between $80k and $180k will get a 23% concession. But those earning more than $300k only a 15% concession. Of course, this doesn't make a lot of sense and makes super more complex. It would make much more sense to abolish the concessional tax on contributions and if that is too severe an increase in tax also cut the rate on superannuation earnings a little. This would make the system much simpler by getting rid of the distinction between concessional and non-concessional contributions, salary sacrificing etc. Of course, Labor is still hoping that public servants and maybe some others earning between $80k and $300k a year will still vote for them. So they haven't raised their tax.

Monday, April 23, 2012

Saturday, April 21, 2012

Budget Cuts and Superannuation

Here in Australia we are now in the run-up to the annual federal government budget announcement. All kinds of ideas that might be in the budget are always floated in the run-up. One big one in the last few days is the idea of cutting superannuation tax concessions. Superannuation is the Australian retirement account system. It is very complex due to the nature of the tax regime. At the moment contributions are taxed at 15% rather than at people's marginal tax rate. Earnings of the funds are taxed at concessional rates and there is no tax when the money is withdrawn and once you are in the withdrawal phase there is no tax on earnings either. The latter two concessions were introduced by the previous Liberal government. So the most likely outcome is to remove the concessions for contributions. This will be a further step towards making our system like the US Roth IRA. But we will still be tax fund earnings which is the main contributor to complexity in the Australian system.

Even though obviously it is personally a bad thing for contributions to be taxed more, I think it is a sensible move. Why should high income earners get such a big concession and low income earners none? * It is the easiest way to push the budget towards surplus without raising tax rates or cutting welfare payments. All government departments in Canberra are already getting massive cuts to their operating budgets, but really there just aren't that many public servants in Canberra that this can make a really big difference, especially as in the short-term they are getting redundancy payments. I would be in favor of cutting some of the family welfare payments that the former Liberal government introduced and that Joe Hockey seems to regret, but I can't see Labor doing that.

* Of course you can flip this argument and say we should have a flat tax and super contributions are a good first step towards a flat tax. But that ain't happening any time soon...

Even though obviously it is personally a bad thing for contributions to be taxed more, I think it is a sensible move. Why should high income earners get such a big concession and low income earners none? * It is the easiest way to push the budget towards surplus without raising tax rates or cutting welfare payments. All government departments in Canberra are already getting massive cuts to their operating budgets, but really there just aren't that many public servants in Canberra that this can make a really big difference, especially as in the short-term they are getting redundancy payments. I would be in favor of cutting some of the family welfare payments that the former Liberal government introduced and that Joe Hockey seems to regret, but I can't see Labor doing that.

* Of course you can flip this argument and say we should have a flat tax and super contributions are a good first step towards a flat tax. But that ain't happening any time soon...

Thursday, April 19, 2012

Houses, Google Rant...

We continue looking at houses... As we look more we gradually understand better what we are looking for. Houses vary a lot in location, age, style etc. Our ideal house now has a much smaller garden and is very new. This means it has windows already fitted with flyscreens for example - you can add them to houses from the 1950s and 1960s but they will be really ugly. Also it means that the bathroom will be much bigger and usually have a separate bath and shower. All the older houses in our price range have tiny bathrooms and it would be very hard to expand them. The whole house would need to be rebuilt and I don't think we want to do that. The houses in the new suburbs are typically on very small blocks (=parcel of land) of around 400 square metres. If the house is a single storey, little land is left over. We don't want to live in those suburbs anyway due to transport issues. We're looking now more at the 600 square metre block versus the 1200 square metre block shown in this post.

As far as finance goes we've had a deposit in a single account growing for the last 2 months now. The lender said the money needs to be there for 3 months before they can lend. It started at $71k and is now $88k. I aim to keep saving to at least $100k. I guess in a month we'll go back and see the lender again. In the meantime we can't really buy anything, and certainly not at an auction. Anyway, most houses do not sell at auctions though many are put up for auction.

When I tried to log on to Blogger today I found myself in the "new" interface. Somewhere, there was a button for the old one and I got back to my familiar world. This button is no longer available though on Google Analytics. I think the new Gogole interfaces are worse than their predecessors. What I don't understand is why when more and more people are using laptops, phones, and tablets to access the web Google is going to interfaces with heaps of white space which can only be really seen properly on a huge desktop screen? At least Reader allows you to get rid of some of the white space and was tolerable after that. But it doesn't look like the Blogger interface has that option. Please let me know if you find it. I also hate Microsoft Office's post 2004 versions - Word 2008 is OK but Excel was horrible and what I've seen of the even newer versions on PCs is no better. So I use Word 2008, Entourage 2008, and Excel 2004. I try to avoid Powerpoint. But when I use it I switch between 2004 and 2008. It's particularly annoying that when you open 2004 Excel graphs in 2008 they are completely reformatted and a total mess in many cases... And 2004 Powerpoint slides don't always look right in 2008 either...

Tuesday, April 03, 2012

Platinum Capital Launches Share Buyback

A lot of Australian closed end funds - known as listed investment companies in Australian jargon - have been trading well below net asset value since the Global Financial Crisis. Some like Platinum Capital (PMC.AX) used to trade at a premium to NAV probably because of accumulated undistributed franking credits.* Some funds have introduced capital management plans to try to boost their share prices. PMC recently announced that it was implementing a share buyback and also it is now posting the daily NAV on its website. I have about 20,000 PMC shares...

* Franking credits are credits for Australian corporation tax paid that are distributed with dividends in Australia. These can be used to reduce investors' personal tax bills. If distributed dividends are less than profits, undistributed franking credits will accumulate. This is what drives the relatively high dividend yield of Australian stocks. They are not included in stated net asset value.

* Franking credits are credits for Australian corporation tax paid that are distributed with dividends in Australia. These can be used to reduce investors' personal tax bills. If distributed dividends are less than profits, undistributed franking credits will accumulate. This is what drives the relatively high dividend yield of Australian stocks. They are not included in stated net asset value.

Monday, April 02, 2012

Moominvalley March 2012 Report

As usual, everything is expressed in US Dollars unless indicated:

Spending this month included a hotel bill that has since been refunded. Without that we spent $4622 despite traveling overseas for 10 days. Because the Australian Dollar fell, investment income in USD terms was negative, but adjusting for the changes in exchange rates we would have made $13,129. Net worth increased by $3,786. But in Australian Dollar terms net worth rose by $A26k to a record $A605k.

Investment returns were -1.10% in USD terms compared to 0.71% for the MSCI World Index and 3.29% for the S&P 500. The Australian stock market languished in relative terms even in local currency terms. In AUD terms we made 2.80%. Our cash allocation is now 15.51% of net worth. Up from 14.78% in February.

For a few more details you can check me out on NetWorthIQ.

Spending this month included a hotel bill that has since been refunded. Without that we spent $4622 despite traveling overseas for 10 days. Because the Australian Dollar fell, investment income in USD terms was negative, but adjusting for the changes in exchange rates we would have made $13,129. Net worth increased by $3,786. But in Australian Dollar terms net worth rose by $A26k to a record $A605k.

Investment returns were -1.10% in USD terms compared to 0.71% for the MSCI World Index and 3.29% for the S&P 500. The Australian stock market languished in relative terms even in local currency terms. In AUD terms we made 2.80%. Our cash allocation is now 15.51% of net worth. Up from 14.78% in February.

For a few more details you can check me out on NetWorthIQ.

Sunday, April 01, 2012

Preliminary Monthly Report

Doing the accounts for March this morning... Looks like we hit a net worth of $A600k for the first time, partly because of the fall in the Australian Dollar to $US1.03 this month. But I'm noticing that quite a lot of our investments are hitting all time highs in terms of the profit we have made on them. These are:

CFS Developing Companies Fund

CFS Diversified Fund

PSS(AP) (Snork Maiden's superannuation fund)

Qantas

Celeste Australian Small Companies

Acadian Global Equity Long-Short

Argo Investments

CFS Geared Global Share Fund

Some others are also quite close to peak profit levels. Of course a lot of other investments are still way down from their peak profit level or are underwater... Two common themes among the winners are small cap stock funds and recent investments. Small caps have been doing very well - they usually do at the beginning of the business cycle, which is why we have invested in them quite heavily. Recent investments haven't yet had a chance to lose money :)

Our house-buying fund has reached $A82,973 from $A77,386 last month. The goal is to reach around $A100k.

Apart from computing rates of return, I use the monthly accounting to check up on whether all our retirement contributions have been properly made by our employers, whether the fees we are being charged are correct, and whether we have been paid money we are owed. I found that my superannuation provider has been charging around $A100 a month for "inbuilt benefits" since I cut my member contribution to zero in September. This makes no sense to me as there is nothing in the prospectus (PDS) about increased fees if you cut your contributions. It does say that you can't get optional life insurance etc. and in fact the fund refused me the coverage, which I tried to get. So I think they are now charging me for coverage that I don't have. I sent them an e-mail querying this...

Anyway this is how our Australian superannuation accounts are doing:

The green line is Snork Maiden's account and the blue line my current account, both of which we are contributing to. The red is my account from when I worked in Australia previously. I rolled it over into a commercial fund manager and it is invested rather riskily. Hence the big fluctuations. We have now managed to save $100k in our new super accounts.

I'm also still owed money for travel to a conference back last November, and for consulting over the last six months. In the latter case, government budget cuts and local circumstances look like I lost the gig now (right after my security clearance was finally approved at the end of February, but it would be nice to get paid for what I already did! The conference money is also owed by another university. My own employer is actually great at reimbursing money. I submitted a bill for our recent overseas trip this Tuesday and already the money was in my account on Friday!

CFS Developing Companies Fund

CFS Diversified Fund

PSS(AP) (Snork Maiden's superannuation fund)

Qantas

Celeste Australian Small Companies

Acadian Global Equity Long-Short

Argo Investments

CFS Geared Global Share Fund

Some others are also quite close to peak profit levels. Of course a lot of other investments are still way down from their peak profit level or are underwater... Two common themes among the winners are small cap stock funds and recent investments. Small caps have been doing very well - they usually do at the beginning of the business cycle, which is why we have invested in them quite heavily. Recent investments haven't yet had a chance to lose money :)

Our house-buying fund has reached $A82,973 from $A77,386 last month. The goal is to reach around $A100k.

Apart from computing rates of return, I use the monthly accounting to check up on whether all our retirement contributions have been properly made by our employers, whether the fees we are being charged are correct, and whether we have been paid money we are owed. I found that my superannuation provider has been charging around $A100 a month for "inbuilt benefits" since I cut my member contribution to zero in September. This makes no sense to me as there is nothing in the prospectus (PDS) about increased fees if you cut your contributions. It does say that you can't get optional life insurance etc. and in fact the fund refused me the coverage, which I tried to get. So I think they are now charging me for coverage that I don't have. I sent them an e-mail querying this...

Anyway this is how our Australian superannuation accounts are doing:

The green line is Snork Maiden's account and the blue line my current account, both of which we are contributing to. The red is my account from when I worked in Australia previously. I rolled it over into a commercial fund manager and it is invested rather riskily. Hence the big fluctuations. We have now managed to save $100k in our new super accounts.

I'm also still owed money for travel to a conference back last November, and for consulting over the last six months. In the latter case, government budget cuts and local circumstances look like I lost the gig now (right after my security clearance was finally approved at the end of February, but it would be nice to get paid for what I already did! The conference money is also owed by another university. My own employer is actually great at reimbursing money. I submitted a bill for our recent overseas trip this Tuesday and already the money was in my account on Friday!

Monday, March 05, 2012

Moominvalley February 2012 Report

The numbers are mostly in now. As usual, everything is expressed in US Dollars unless indicated. February managed to squeeze in three pay checks and so "other income" which is mainly salary is particularly high. But we actually got less retirement contributions credited and so that number is a little lower than normal. Investment income was also good with about a 1/3 from the gain in the Australian Dollar, again near record highs. above $US1.07. Expenditure was on the high end above $5k. Partly due to car registration ($A959...) and spending on an upcoming trip ($A741). Also, Snork Maiden applied for Australian citizenship ($A260). Net worth increased $38k ($A26) to $624k ($A579k). Both all time highs.

Investment returns were 3.67% in USD terms compared to 5.08% for the MSCI World Index and 4.32% for the S&P 500. The Australian stock market languished in relative terms. And due to the gain in the Aussie Dollar investment returns were only 1.95% in AUD terms. As a result our allocation to Australian stocks fell... well allocation to everything except cash fell. Our cash allocation is now 14.3% of net worth. Up from 4.7% in January.

For a few more details you can check me out on NetWorthIQ.

Sunday, March 04, 2012

Australian House Price Index

The US has the Case-Shiller indexes and now Australia has a potentially tradeable house price index too.

Friday, March 02, 2012

February 2012

More data than usual is delayed this month so I'm planning to wait to report fully when I have a bit more. As you can see from NetWorthIQ we exceeded a net worth of $US600k for the first time and we also hit a new record high net worth in Australian Dollar terms, though it is still below $A600k. We moved a lot of money into cash over the month. Our house-buying account now has $A77,386. But that is still at the low end of the necessary 10% deposit.

Thursday, March 01, 2012

Moominmama Portfolio Performance February 2012

A respectable rate of return and most asset classes did well with the USD falling a little against Sterling and Euros. The MSCI World Index gained 5.08% and the S&P 500 4.32%. So the non-US equities beat the market a little.

Sunday, February 26, 2012

National Savings Certificates and Lloyds Bank

We finally have managed to get a UK national savings certificate worth about £40k that was in my father's name only transferred to my mother's name. My father died almost ten years ago. The truth is though that we didn't start trying to fix this till recently. My brother dealt with getting a lawyer etc. to complete the UK probate and get this sorted out. They wouldn't accept the inheritance documents from the country where my father died...

But now we have the problem of what to do with the certificate. They will only allow us to cash it out if we transfer the money to a bank in the UK. But my mother's bank, Lloyds (which I was once a customer of too*) is extremely difficult to deal with, even though my brother has a power of attorney. In my brother's words:

"the people in the branch don't really care and the call center is worse. They all stick very closely to the letter of their regulations. I have a limited power of signature there. They don't respect faxes, generally ignore letters, don't use email... in short useless. The problem appears to be that it is a regular banking account and they are not set up to work internationally. When I tried to make a transfer of GBP 700 to the UK lawyer for the probate they said I could only do it if a came into the branch, so I did it in the end from UBS..."

They'll only do anything if they talk to my mother on the phone but then they will likely decide that she is incompetent... So even closing the account seems impossible. To complicate things further, my mother still has a small pension that is paid into this account.

So it looks like we will keep the certificate renewing in her name now.

* My first bank account was with Lloyds. I entered some competition where they opened an account with £10 in it. That was back in 1983 I think. I got rid of the account some time around 1997 probably and no longer have any financial connection to the UK.

But now we have the problem of what to do with the certificate. They will only allow us to cash it out if we transfer the money to a bank in the UK. But my mother's bank, Lloyds (which I was once a customer of too*) is extremely difficult to deal with, even though my brother has a power of attorney. In my brother's words:

"the people in the branch don't really care and the call center is worse. They all stick very closely to the letter of their regulations. I have a limited power of signature there. They don't respect faxes, generally ignore letters, don't use email... in short useless. The problem appears to be that it is a regular banking account and they are not set up to work internationally. When I tried to make a transfer of GBP 700 to the UK lawyer for the probate they said I could only do it if a came into the branch, so I did it in the end from UBS..."

They'll only do anything if they talk to my mother on the phone but then they will likely decide that she is incompetent... So even closing the account seems impossible. To complicate things further, my mother still has a small pension that is paid into this account.

So it looks like we will keep the certificate renewing in her name now.

* My first bank account was with Lloyds. I entered some competition where they opened an account with £10 in it. That was back in 1983 I think. I got rid of the account some time around 1997 probably and no longer have any financial connection to the UK.

Friday, February 17, 2012

Snork Maiden's Job Made Permanent

She had the interview about four weeks ago but had to wait till today to get confirmation that her position which was a temporary one has been converted to a continuing one. This also means a promotion to what would be the assistant professor level if she was at a university rather than a government lab.

Meeting a Lender

Today we went to meet with a mortgage lender. We didn't get far though. I thought I would be OK that I had easily accessible money in managed funds but they want to see at least a 5% deposit held in cash for at least 3 months. So I've been busy selling some of Snork Maiden's managed funds - mainly a bond fund - and redrawing money I had deposited into my margin loan account since last August and we now have $A70k in cash in Australia. I'm aiming for a 10% down-payment. So we now meet the 5% requirement and are well on our way to the 10% down-payment (assuming the house we buy would be $750k +).

Tuesday, February 14, 2012

Sydney is the 7th most expensive city in the world to live in and 50% more expensive than New York. As Melbourne is 8th, I'm sure Canberra is also in the top 10. To bear in mind when reading my blog and comparing to US costs and prices :)

Sunday, February 12, 2012

2012 Forecast

If the stock markets do well, the Australian Dollar stays high, and we don't buy a house we might hit $US800k this year... Buying a house would reduce net worth by about $50k due to purchase costs - mostly "stamp duty". If the Australian Dollar fell to its purchasing power parity level we'd more likely be at $US600k. If the stock market is flat we'd probably be $100k lower. I doubt after two negative years in Australia there will be a third negative year. I also doubt the Australian Dollar would really fall to 70 US cents... But $US500-800k is probably a good range to expect. In AUD expect $A600-800k.

It is looking like Snork Maiden's job will be converted to a permanent position (and a promotion) but the paperwork is still being processed...

It is looking like Snork Maiden's job will be converted to a permanent position (and a promotion) but the paperwork is still being processed...

Friday, February 10, 2012

Commonwealth Bank Don't Seem to Want to Lend Money

So we (Snork Maiden and me) went into a Commonwealth Bank branch and talked to the person at the customer service desk about getting pre-approved for a mortgage. She said she would get someone to call us about setting up an appointment. After a week, no-one has called us. So I next thought I'll phone the bank to set up an appointment. But I got into the automatic phone system and without a "phone banking password" I couldn't continue to talk to anyone. I don't have one because usually I do everything online. This would stop any new customers either... I could send them an e-mail, but instead I will go to the central branch in Canberra first and see if that works. Otherwise, we'll have to go to a different bank, it would be nice though to have everything consolidated together...

Tuesday, February 07, 2012

One Million Kilometres

I'm planning a trip next month to a neighboring country and just realized I will hit 1 million kilometres of flying during my flight there. I've kept a spreadsheet of my travel from when I first moved to the US and hadn't flown much yet recording all flights I've ever been on. A professor in an environmental studies class noted he didn't have a car but had flown as far as the moon and back (I think that is what he said) and so wondered if he was hypocritical and I wondered how much I'd flown. I use a piece of software called anAtlas to compute the distances. It's a long way to go to match George Clooney's character :)

Yes, I didn't fly anywhere until I was 18 years old.

Yes, I didn't fly anywhere until I was 18 years old.

Sunday, February 05, 2012

Saving and Buying a House

This graph explains our sudden interest in the housing market. It shows monthly saving in Australian Dollars outside of retirement accounts and not including investment income or losses. The dark line is a 12 month moving average. Negative numbers mean that we spent more than we earned in that month. The main reasons for that have been major international trips or moves and a period of unemployment when I was single back in 2001-2 followed by an international move. The record high saving in 2001 is due to a termination payment when my job ended.

There is a recent move up to a much higher level of saving, which means that we could, in theory, afford mortgage payments that are going to be $2000-$4000 more than our current rent (plus other housing costs). As you can see, there's never been a saving level like this in my financial history. After we moved back to Australia in 2007 saving was minimal and then jumped to about $3k per month for a short while. So we definitely could not afford to buy a house during that period. I now have a permanent job. Snork Maiden is still waiting to find out if her job will be converted to permanent status.

Wednesday, February 01, 2012

Moominmama Portfolio Performance January 2012

As usual, this much more conservative portfolio returned less than the stock market or the Moominvalley portfolio. And with dissaving rather than saving it is off the historic highs. The strongest performing asset classes were Brazilian and Asian stocks. But all categories gained money.

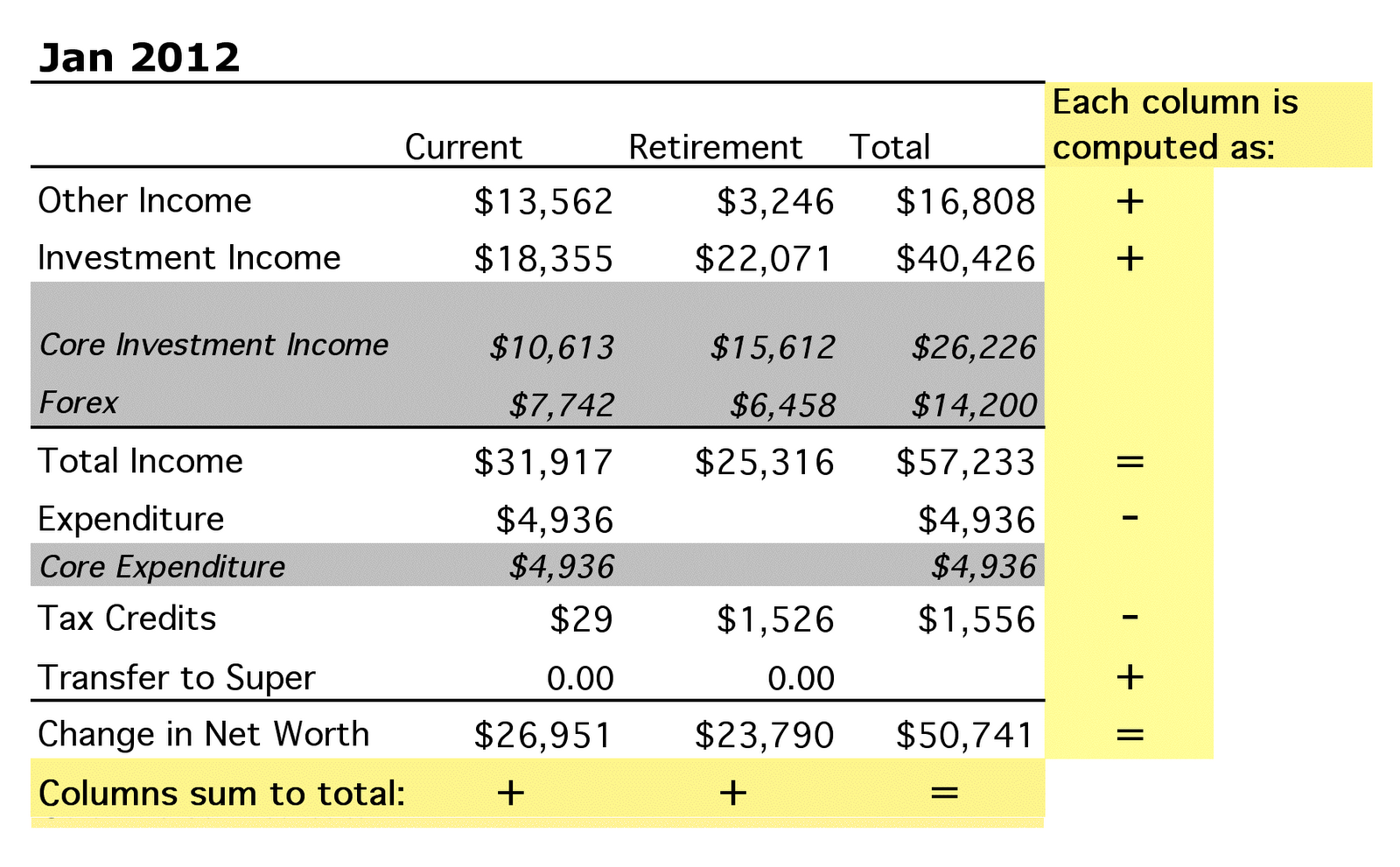

Moominvalley January 2012 Report

This was a good month with decent market returns, a relief after a year where most months we were losing money. The big news is that we hit a record net worth in both Australian Dollars and US Dollars. Here is what it looks like in AUD:

The new net worth is $A553k. The previous high water mark in Australian Dollars was $A527k in August 2007, which was the month Snork Maiden and I merged finances in preparation to move to Australia. So in that sense we have finally recovered from the trauma of the GFC (and the costs of moving to Australia) but profit levels are very depressed and so in that sense we haven't recovered at all. It's mostly down to saving:

As you can see from both these graphs, non-retirement savings is the main driver. We also hit a new high in USD at $US586k. The previous high was $US574k in April last year. The income /expenditure accounts in US Dollars look like this:

Investment income was high and the Australian Dollar gained to almost $US1.06. Expenditure was higher than last month but within recent norms. Net worth increased by $US50k ($A30k).

The MSCI World Index gained 5.84% in USD terms and the S&P500, 4.48%. We gained 7.55% in USD terms (4.05% in AUD terms and 4.90% in currency neutral terms). We reduced cash and net loans and the allocation to large cap Australian stocks increased most (to 44.76%) due to market performance. US stocks were our highest performing asset class.

The new net worth is $A553k. The previous high water mark in Australian Dollars was $A527k in August 2007, which was the month Snork Maiden and I merged finances in preparation to move to Australia. So in that sense we have finally recovered from the trauma of the GFC (and the costs of moving to Australia) but profit levels are very depressed and so in that sense we haven't recovered at all. It's mostly down to saving:

As you can see from both these graphs, non-retirement savings is the main driver. We also hit a new high in USD at $US586k. The previous high was $US574k in April last year. The income /expenditure accounts in US Dollars look like this:

Investment income was high and the Australian Dollar gained to almost $US1.06. Expenditure was higher than last month but within recent norms. Net worth increased by $US50k ($A30k).

The MSCI World Index gained 5.84% in USD terms and the S&P500, 4.48%. We gained 7.55% in USD terms (4.05% in AUD terms and 4.90% in currency neutral terms). We reduced cash and net loans and the allocation to large cap Australian stocks increased most (to 44.76%) due to market performance. US stocks were our highest performing asset class.

Failed Auction

We went to our first home auction today. There was a big crowd but in the end only 4 people seem to have registered to bid in the auction. The auctioneer called for bids and no-one bidded. Not even "$500k" say. Maybe those people were just too embarassed to say they weren't bidding? So the auctioneer went inside and phoned the vendor and came back and made a bid (he's allowed to make one) at $820k. No-one bidded and the house was passed in without sale. It will now be remarketed with a fixed price. It will be interesting if that will be at $820k or less. This is a further sign that the property market is softening here. There are few auctions now. Most properties are marketed with fixed prices and there are a lot for sale compared to the number that have sold recently. A year or two ago it was mostly auctions.

P.S.

This house that we saw last weekend has already been slashed by $70k. It started way too high of course.

Saturday, January 28, 2012

House Hunting

The last couple of weekends we have been to open houses in neighborhoods we might like to live in. I think the nicest house we've seen is this one. We're not really serious about this at this stage, just trying to get a feel for the market. Definitely it seems that houses recently put on the market are asking for ridiculous prices and dropping them over time. This one was $990k-$1,040k. Given the market here the price is reasonable. The garden is really beautiful with several mature trees.

We saw one earlier in the day that wanted $1.22m for what I thought wasn't as nice (though Snork Maiden disagrees). That house has only just been put on the market. We were the only people at the showing and the owner is trying to sell without an agent.

With one exception all the agents we have encountered were driving luxury cars - Mercedes, Audi, Porsche Cayenne etc.

Wednesday, January 18, 2012

Concessional Contribution Cap and Unisuper

Unisuper say they are concerned that the Australian government will not index the concessional superannuation limit this year. The issue is that employers in the university sector are contributing 17% of employees stated salaries to the Unisuper superannuation fund. In other words, for someone earning $A100k per year they contribute $A17k to this retirement fund in addition to the salary they pay. Somewhat similar to the "matching contribution" idea in the US, though no match is required from the employee. This is greatly in excess of the 9% which the government mandates employers to pay.

The problem for high earning employees is that the limit on pre-tax (or concessional or salary sacrifice) contributions is $A25k a year. I'm just below this threshold at the moment. Probably, when our salaries go up in July I'll be over it. Concessional super contributions are taxed at 15% rather than your usual marginal tax rate (mine is 37% + medicare). If you try to contribute too much the fund will accept the money but the government taxes it at the top tax rate - 46.5% (including medicare). So a little bit of my salary will get taxed at the top rate and then stuffed in an account I can't access for at least another 13 years...

The logical thing would be to reduce the contribution from 17% for high earners and pay that out to employees as extra salary. But that seems to be too simple for the convoluted Australian super system. Instead, Unisuper just lobbies the government to raise the cap. I guess it's not in their interest to reduce contributions and the unions who negotiated this deal (which I don't belong to) don't care that some full professors have to pay some extra tax.

It won't amount to much money for me, but it just seems silly. For those earning more than $A180k a year, the rate is no higher than their usual marginal tax rate.

The problem for high earning employees is that the limit on pre-tax (or concessional or salary sacrifice) contributions is $A25k a year. I'm just below this threshold at the moment. Probably, when our salaries go up in July I'll be over it. Concessional super contributions are taxed at 15% rather than your usual marginal tax rate (mine is 37% + medicare). If you try to contribute too much the fund will accept the money but the government taxes it at the top tax rate - 46.5% (including medicare). So a little bit of my salary will get taxed at the top rate and then stuffed in an account I can't access for at least another 13 years...

The logical thing would be to reduce the contribution from 17% for high earners and pay that out to employees as extra salary. But that seems to be too simple for the convoluted Australian super system. Instead, Unisuper just lobbies the government to raise the cap. I guess it's not in their interest to reduce contributions and the unions who negotiated this deal (which I don't belong to) don't care that some full professors have to pay some extra tax.

It won't amount to much money for me, but it just seems silly. For those earning more than $A180k a year, the rate is no higher than their usual marginal tax rate.

New Investment: Argo Investments

Back in 2008 I blogged about traditional Australian Listed Investment Companies. These have lower management fees than Australian index funds and in the long-run seem to slightly beat the index by selecting investments and selling options. I finally made an investment in Argo investments. The current book price relative to net asset value is better than Australian Foundation or Djeriwarrh and unlike Milton it is marginable at CommSec. They also have an annual share purchase plan, which I might participate in. I started small with 1900 shares - just a bit less than $A10k.

This investment is despite really being overweight in large cap Australian share according to my criteria and desiring to increase liquidity. My last post showed that our allocation to large cap Aussie stocks, though still high has been coming down. And I think we can increase liquidity and invest a little.

And I'm not even sure it makes sense to borrow money at CommSec's high rates. The alternatives are to borrow at lower rates via Interactive Brokers (but I need to get money into the account and do currency conversions along the way) or invest in the CFS Geared Share Fund. The latter has a very high management expense but they access funds at lower interest rates. Also, holding this investment with Interactive Brokers probably will make it hard to participate in dividend reinvestment and the share purchase plan. I guess I'll do a bit of each. None is ideal.

This investment is despite really being overweight in large cap Australian share according to my criteria and desiring to increase liquidity. My last post showed that our allocation to large cap Aussie stocks, though still high has been coming down. And I think we can increase liquidity and invest a little.

And I'm not even sure it makes sense to borrow money at CommSec's high rates. The alternatives are to borrow at lower rates via Interactive Brokers (but I need to get money into the account and do currency conversions along the way) or invest in the CFS Geared Share Fund. The latter has a very high management expense but they access funds at lower interest rates. Also, holding this investment with Interactive Brokers probably will make it hard to participate in dividend reinvestment and the share purchase plan. I guess I'll do a bit of each. None is ideal.

Thursday, January 12, 2012

Annual Review: Part III

This is what happened to asset allocation over the year:

Cash and bonds went up and large cap Australian stocks went down. This is due to market weakness and a purposeful policy of increasing liquidity in recent months. The large cap Aussie stock weighting fell from 51% last December to about 43% now. In the long-run for diversification reasons I'd want to get that smaller still but it is hard to resist the benefits of franked dividends.

Cash and bonds went up and large cap Australian stocks went down. This is due to market weakness and a purposeful policy of increasing liquidity in recent months. The large cap Aussie stock weighting fell from 51% last December to about 43% now. In the long-run for diversification reasons I'd want to get that smaller still but it is hard to resist the benefits of franked dividends.

Saturday, January 07, 2012

Annual Review: Part II

Not sure how serious this annual review is going to be. I'm just going to post what I feel like. This is what happened to net worth in Australian Dollars over the course of the year:

We ended the year with somewhat higher net worth but retirement savings actually declined while non-retirement savings overtook retirement savings for the first time since the onset of the financial crisis. This trend will continue this year, I think. Maybe once I turn 50 I might increase retirement savings above the tax concessional level * as the money can be accessed from age 60.

This chart shows underlying story:

Persistent saving throughout the year in both types of accounts and persistent investment losses at a similar rate on both.

*$A25k a year for each of us can go in after 15% tax. Contributions above this rate are taxed at our marginal rates.

We ended the year with somewhat higher net worth but retirement savings actually declined while non-retirement savings overtook retirement savings for the first time since the onset of the financial crisis. This trend will continue this year, I think. Maybe once I turn 50 I might increase retirement savings above the tax concessional level * as the money can be accessed from age 60.

This chart shows underlying story:

Persistent saving throughout the year in both types of accounts and persistent investment losses at a similar rate on both.

*$A25k a year for each of us can go in after 15% tax. Contributions above this rate are taxed at our marginal rates.

Friday, January 06, 2012

Debit Card Fraud

I got an e-mail from HSBC in India today telling em to phone a US number because my debit card may have been used fraudulently. I did a Google search for the number and came up with what looked like an HSBC site with that number on it. So I called up and soon was speaking with someone in India. They asked for a lot of identifying detail but it wasn't what I was used to banks asking for. I started getting suspicious and started Googling them while talking to them and found some sites claiming that that number was a fraud. I stopped the conversation after they claimed that they had cancelled my debit card and refused to give them more information. I asked them whether they could prove they were from HSBC and they had no answer to that. All the guy could say was that he worked for the fraud department.

I then went to my regular HSBC site and phoned the regular customer service number. They told me that yes my card had been cancelled and it was a legit call. The woman there arranged to send me a new card.

Was I overly suspicious? The bank has a problem if people might think that legitimate workers for the bank are fraudsters.

My card was only defrauded for $6 in the original transaction. I was much more worried about the guys I was now talking to ripping me off for a lot more.

I then went to my regular HSBC site and phoned the regular customer service number. They told me that yes my card had been cancelled and it was a legit call. The woman there arranged to send me a new card.

Was I overly suspicious? The bank has a problem if people might think that legitimate workers for the bank are fraudsters.

My card was only defrauded for $6 in the original transaction. I was much more worried about the guys I was now talking to ripping me off for a lot more.

Thursday, January 05, 2012

Weird Price Discrimination

So we were in Dick Smith (electronics store) about to buy something that costs $A250. Snork Maiden asked the cashier if any deals were available. He looked at his computer for a while and said - I can give you a two year extended warranty and reduce the price to $A225 - the price of the item was now only $A170 and the warranty $A55. This makes no economic sense to me at all. How can it make sense for them to give away more stuff for less money? I can understand where he'd reduce the price if we asked or throw in the warranty for free, but why do both? Anyway, of course I agreed to that deal.

Wednesday, January 04, 2012

Annual Review: Part I

It was a big year careerwise. I got a permanent job in Australia after working temporarily for the same department between January and August. I was promoted to the top rank. Snork Maiden is still trying to turn her position into a permanent one. She has an interview later this month for that purpose. Still this meant that our income (not counting investments) reached a record high this year and will likely be even higher next year:

This table is based on my monthly reports. The numbers are in US Dollars. The USD/AUD exchange rate didn't move much over the year as can be seen from the line labelled "Forex". Salary etc. came in at $165k for the year. This is after tax. Retirement contributions were $35k for a total of nearly $200k. Investment generated a loss of $92k (pre-tax). 9 out of 12 months saw losses. A pretty dispiriting year. On the other hand we saw the highest percentage gain ever in October. More on investment performance in an upcoming post. Expenditure was $75k or more than $6k per month. This does include some travel that was later reimbursed. In AUD terms total expenditure went up from $A62k in 2010 to $A71k. So there may be some lifestyle inflation there... But non-investment income doubled so it was a lot less than the income gain.

In the end net worth rose by $36k to $535k for the year or $A33k to $A522k.

This table is based on my monthly reports. The numbers are in US Dollars. The USD/AUD exchange rate didn't move much over the year as can be seen from the line labelled "Forex". Salary etc. came in at $165k for the year. This is after tax. Retirement contributions were $35k for a total of nearly $200k. Investment generated a loss of $92k (pre-tax). 9 out of 12 months saw losses. A pretty dispiriting year. On the other hand we saw the highest percentage gain ever in October. More on investment performance in an upcoming post. Expenditure was $75k or more than $6k per month. This does include some travel that was later reimbursed. In AUD terms total expenditure went up from $A62k in 2010 to $A71k. So there may be some lifestyle inflation there... But non-investment income doubled so it was a lot less than the income gain.

In the end net worth rose by $36k to $535k for the year or $A33k to $A522k.

Tuesday, January 03, 2012

Moominvalley December 2011 Report

I'll do an annual review soon, so this will be pretty brief. As usual the numbers are in US Dollars. Non-investment income was on the high side as I finally got a reimbursement for my trip to India. These business expenses get included in our regular spending and income figures and exaggerate them a bit. I do try to compute "core expenditure" that excludes this sort of spending. Retirement contributions were lower than normal because some payments seem to have been held up by the holidays. Another losing month on the investment front. We lost 1.31% in USD terms (and about the same in terms of other currencies) though the MSCI only lost 0.17% for the month and the S&P 500 gained 1.02%. Still we managed to increase net worth by $6k and it's close to a new all time record in Australian Dollar terms at $A522k ($US535k).

Expenditure was very low compared to recent levels at just $3,864 ($A3,769). Snork Maiden thinks I must have made a mistake in my computations as she remembers spending a lot of money at Costco, that opened here recently...

Sunday, January 01, 2012

Moominmama Portfolio Performance Dec 2011

Happy new year! Hopefully, this year will be better than the last. For US investors things weren't so bad but the Australian stock market has suffered two losing years in a row, which hasn't happened since the early 1980s. As you can see it was a losing month for Moominmama too. The MSCI index was down 0.17% for the month and the S&P 500 up 1.02%. For the year the MSCI lost 5.96% but Moominmama lost 6.31% with a 1.31% loss in this final month. The only bright spots were Brazilian stocks and Sterling.

Friday, December 23, 2011

Street Scenes from the Other Side of the World

Third post in this series:

1996-2002:

2007-Present:

The most noticeable thing about these pictures I think is the sunshine :) It's not been like that much recently.

1996-2002:

2007-Present:

The most noticeable thing about these pictures I think is the sunshine :) It's not been like that much recently.

Thursday, December 22, 2011

Another Continent

Street scenes from the other side of the ocean:

1990-1991:

1991-1992:

1992-1993:

1995-1996:

2002-2007:

Yes, when I was in grad school I ended up moving every year. Since then, I've been much slower to move.

1990-1991:

1991-1992:

1992-1993:

1995-1996:

2002-2007:

Yes, when I was in grad school I ended up moving every year. Since then, I've been much slower to move.

Wednesday, December 21, 2011

Revisiting the Old Neighborhood

I was inspired by these posts to put up some pictures of places I used to live. The difference in my case is that they all look much the same as when I lived there and I'm twice the age of Ken! For three countries I've lived in I could just go to Google Earth and capture pictures. No need to actually travel :) So to kick off here is Britain below. I've tried to capture a feeling of the streets and I've just labeled them by when I lived there. It's pretty easy to guess where they are though :)

1964-1966:

1966-1983:

1989-1990:

1993-1994:

The only changes are really the models of the cars and in the 1966-1983 place the size of the plants in the gardens and the recycling bins.

1964-1966:

1966-1983:

1989-1990:

1993-1994:

The only changes are really the models of the cars and in the 1966-1983 place the size of the plants in the gardens and the recycling bins.

Wednesday, December 07, 2011

Qantas Technical Analysis

I haven't done this kind of thing for a while :) Looking at the Qantas chart there is a clear resistance line at $1.80. TA theory would say that if we get above that we probably won't go below it again in a hurry. It's interesting a friend said he thinks there will be a new buyout offer at $1.80 - Seems very low though to me... Don't know if it based on anything solid or just rumors he heard (my friends are in places where you can hear interesting rumors). Anyway, there is also an inverse head and shoulders formation in Qan that would take it to about $2.10 if it works. The most recent low in QAN is higher than the previous one and there is some sign that volume is declining through the formation, though hardly a classic pattern.

Thursday, December 01, 2011

Moominmama Portfolio Performance November 2011

And back down again this month. The portfolio was heavily affected by the rise in the US Dollar reducing the value of non-USD assets in USD terms.

It was Moominmama's 80th birthday today, by the way, and my 47th birthday. Yes, we have the same birthday. We did a Skype video hook up across the time zones. Snork Maiden, my brother (doing the tech stuff at their end), and the live in helper that looks after my Mom (though she only lives in the next building to my brother) were all in on the call. My brother is moving to a bigger apartment, but it is just a block away. Hopefully, I'll visit some time next year.

Moominvalley November 2011 Report

Things reversed again this month but the losses were actually less than I expected. IN USD terms we lost 6.35%. In AUD terms we lost 3.05% and in currency neutral terms 3.65%. But the MSCI World Index only lost 2.94% for the month. The reason for our underperformance is that the Australian market largely missed out on the global 30th of November rally induced by globally coordinated easing by central banks. The World Index rose by 3.71% on 30th November. So the day before the index was down 6.54% on the month, which is roughly what we lost.

Anyway, here are this month's accounts in USD:

USD net worth fell by $20k but in AUD terms we were only down $A1k. . Net worth is at $531k or AUD 519k. Total non-investment income was $20k. Just over $3k of that came from a refund I got for our trip to the US in September-October. I'm still awaiting a couple of other travel refunds. Retirement contributions are now running at $4k a month as we are both contributing near the maximal concessional amount ($A25k per annum) including employer contributions. Investments lost a total of $35k with $15k of that due to foreign exchange movements as the US Dollar rose against other currencies. Total spending was $6,065 but almost $1,000 of that was a trip I took to Queensland which should be refunded. So spending was around our "new normal" of $5,000 per month.

Yeah, these numbers in terms of non-investment income are feeling pretty crazy to me. You can see how quickly things have changed when you look back over the last several months of reports.

Anyway, here are this month's accounts in USD:

USD net worth fell by $20k but in AUD terms we were only down $A1k. . Net worth is at $531k or AUD 519k. Total non-investment income was $20k. Just over $3k of that came from a refund I got for our trip to the US in September-October. I'm still awaiting a couple of other travel refunds. Retirement contributions are now running at $4k a month as we are both contributing near the maximal concessional amount ($A25k per annum) including employer contributions. Investments lost a total of $35k with $15k of that due to foreign exchange movements as the US Dollar rose against other currencies. Total spending was $6,065 but almost $1,000 of that was a trip I took to Queensland which should be refunded. So spending was around our "new normal" of $5,000 per month.

Yeah, these numbers in terms of non-investment income are feeling pretty crazy to me. You can see how quickly things have changed when you look back over the last several months of reports.

Monday, November 14, 2011

More Liquidity

With potentially large expenditures in the next year or two we need to have more liquidity. So going forward I'm going to focus discretionary saving more on short-term investments and paying down debt. Our automatic investments will continue as before at $5000 plus a month. Just over $A3,000 per month going into superannuation (after the 15% contribution tax) and $A2,000 a month into managed funds.

Show of Confidence in Qantas?

It looks like the chairman and a bunch of other directors of Qantas went out and bought shares on the market. It's nice to see a vote of confidence in the company from the board. But really 100,000 shares at $1.60 each is not going to be much of an investment for Leigh Clifford given that he was previously CEO of Rio Tinto. Anyway, the stock price is up a little this morning on this news (as I can't see any other reason apart from the positive performance on Wall Street on Friday).

Saturday, November 12, 2011

Invest in Multifamily Houses in Jersey City?

I saw an ad in the Australian Financial Review today to invest in the US Masters Residential Property Fund. I already invest in US property through the TIAA Real Estate Fund, which does include apartment complexes but not small multi-family or single family houses like this fund does. The supposed advantages are a high yield relative to investing in single family homes in Australia, the low price of housing currently in the US, and the high value of the Australian Dollar. The fund is not hedged, so if the Australian Dollar falls the value in AUD terms will go up. Also it is cheap to borrow in the US, though currently the fund is not borrowing. The management fee is about 1.6% per year. There are a few possible downsides:

1. The fund is currently trading at $1.64 on the National Stock Exchange (formerly the Newcastle Stock Exchange), but it's NAV is $1.54.

2. The application fee amounts to 4%. Combined, this means that you lose more than 10% of your money right away.

3. Selling units would mean trading on the NSX. Neither CommSec nor Interactive Brokers trades on this exchange.

4. All the houses bought so far are in Jersey City, which isn't very diversified. At least it isn't Michigan I guess...

Point 3, rules out buying units in the market unless I was to set up an account with Macquarie say... So I think I'll pass on this. What US REITs invest in this investment class that I could buy through my Interactive Brokers account?

Of Course Compulsory Super is a Cost to Employees...

A reader asks the Sydney Morning Herald:

"Q The money that an employer ''compulsorily contributes'' to my super * comes from where? Is it my money contributed on my behalf by the employer, or is it the employer's money, begrudgingly contributed to my super because the government orders it?"

and the answer:

"A The contribution is a cost to employers and, although contributed on behalf of the employee, is not a cost to them unless they are employed under a salary-packaging arrangement."

While this might be legally correct it is absolutely not correct from an economic point of view. It reminds me of the claims back in 2000 from the government that the GST (=value added tax) wasn't a tax on business but just a tax collected by businesses from consumers for the government. If employers didn't have to make 9% contributions to super they would pay workers higher nominal wages by the same amount (presuming that workers value super and extra salary the same and so labor supply was unaffected which wouldn't be quite true). It is very much forced saving by workers. That doesn't mean there is anything wrong with it. It is a kind of behavioral economics policy - forcing people to save in their own interest because they wouldn't do enough of it otherwise.

* Super(annuation) is the retirement account system in Australia. Employers must by law contribute a minimum 9% of the stated salary on top of the salary actually paid to a superannuation account. This will be rising to 12% if current legislation is passed.

"Q The money that an employer ''compulsorily contributes'' to my super * comes from where? Is it my money contributed on my behalf by the employer, or is it the employer's money, begrudgingly contributed to my super because the government orders it?"

and the answer:

"A The contribution is a cost to employers and, although contributed on behalf of the employee, is not a cost to them unless they are employed under a salary-packaging arrangement."

While this might be legally correct it is absolutely not correct from an economic point of view. It reminds me of the claims back in 2000 from the government that the GST (=value added tax) wasn't a tax on business but just a tax collected by businesses from consumers for the government. If employers didn't have to make 9% contributions to super they would pay workers higher nominal wages by the same amount (presuming that workers value super and extra salary the same and so labor supply was unaffected which wouldn't be quite true). It is very much forced saving by workers. That doesn't mean there is anything wrong with it. It is a kind of behavioral economics policy - forcing people to save in their own interest because they wouldn't do enough of it otherwise.

* Super(annuation) is the retirement account system in Australia. Employers must by law contribute a minimum 9% of the stated salary on top of the salary actually paid to a superannuation account. This will be rising to 12% if current legislation is passed.

Tuesday, November 08, 2011

Security Clearance

If you ever have to do a security clearance - at least in this country - these are some of the things you'll need:

1. Everywhere you ever travelled overseas down to the months for the last 10 years and by year for previous years. And for your spouse too.

2. Addresses with proof in the form of utility bills for last ten years.

3. Everywhere you worked with months and times you weren't working for the last ten years.

4. Birth certificate etc. of course

5. You can get away with minimal info on your parents and your spouse's parents.

They'll also want to know all the accounts you have and their value and your credit card numbers etc.

Luckily I can provide all the info more or less. So that's a good reason not to throw things away...

This is the lowest level clearance so I can be granted free access to a federal government department. Working for a university is not working for the government. It's a public sector non-profit or something...

1. Everywhere you ever travelled overseas down to the months for the last 10 years and by year for previous years. And for your spouse too.

2. Addresses with proof in the form of utility bills for last ten years.

3. Everywhere you worked with months and times you weren't working for the last ten years.

4. Birth certificate etc. of course

5. You can get away with minimal info on your parents and your spouse's parents.

They'll also want to know all the accounts you have and their value and your credit card numbers etc.

Luckily I can provide all the info more or less. So that's a good reason not to throw things away...

This is the lowest level clearance so I can be granted free access to a federal government department. Working for a university is not working for the government. It's a public sector non-profit or something...

Sunday, November 06, 2011

Vice Chancellor of University of Queensland was Paid More than $1 Million

The Vice Chancellor (i.e. President) of the University of Queensland is resigning. But what shocked me in the story was that he was paid over $1 million! And his deputy was paid almost $1 million. Recently there was a controversy that the head of the Reserve Bank had an increase in salary to $1 million and that several other public officials saw increases to around $800k. The Prime Minister gets less than $400k and government department heads were in the $400k or so range. A full professor gets $145k base salary with more senior and star people up to $250k (Laureate Fellows get this much). My impression was that a Dean would get around $200k and so I assumed that the VC would be in the $400k range. But apparently not. Or is it just Queensland? Apparently this is not unique. Ian Young got about $900k at Swinburne and so presumably gets much more now he moved to ANU.

Friday, November 04, 2011

Australia is the Richest Country in the World by Far

When measured in terms of median wealth per individual in US Dollars at $220,000. Switzerland is richest in terms of mean wealth per individual. Both facts are in the Credit Suisse Wealth Report.

(HT: Enoughwealth)

(HT: Enoughwealth)

Wednesday, November 02, 2011

15.01%

Yes our rate of return in USD was 15.01% for October which is a record. But it was largely due to the rebound in the Australian Dollar. In AUD terms we only made 5.61% and in currency neutral terms 8.57%. And after 7 months of losses in AUD terms it doesn't get us back to where we were either. And now Greece seems to have gone crazy and called a referendum on a deal which would have written off a large amount of their debt. I didn't think Greece would end up exiting the Euro. But at this rate it might. I still think the Euro project as a whole won't be reversed. Anyway, here are this month's accounts in USD:

A gain of $87k in net worth. $30k came from foreign currency movement. $40k from core investment returns and $23k from salary, tax refunds, and retirement contributions. Spending was at $5,672. It seems that $5,000 is the new normal for spending. Net worth is at $551k or AUD 519k.

A gain of $87k in net worth. $30k came from foreign currency movement. $40k from core investment returns and $23k from salary, tax refunds, and retirement contributions. Spending was at $5,672. It seems that $5,000 is the new normal for spending. Net worth is at $551k or AUD 519k.

Tuesday, November 01, 2011

Moominmama Portfolio Performance October 2011

Finally a positive month... The MSCI World Index gained 10.74% for the month while the S&P500 total return index gained 10.93%. But the portfolio only gained 4.85%. Beta is estimated at 0.49 so this is roughly what you'd expect to see. Alternative investments lost money while equities actually outperformed the indices.

My preliminary estimate is that we gained more than 15% in USD terms in October.

Friday, October 14, 2011

Average Australian Households

Thanks to high house prices and compulsory superannuation the average Australian household is much wealthier than the average American household.

We are below average with a net worth of about $A510k vs. $A720k for the average household. The average house was worth $A541k for those who owned their home outright and $A521k for those with mortgages. The average superannuation (retirement) balance was $A154k. Here we are above average at $A261k. That includes a couple of US retirement accounts though.

Our income (not discussed in this article) puts us in the top 10% or so probably of households and in the long-run I expect we will end up wealthwise in the top 20% of households who average $A2.2 million.

We are below average with a net worth of about $A510k vs. $A720k for the average household. The average house was worth $A541k for those who owned their home outright and $A521k for those with mortgages. The average superannuation (retirement) balance was $A154k. Here we are above average at $A261k. That includes a couple of US retirement accounts though.

Our income (not discussed in this article) puts us in the top 10% or so probably of households and in the long-run I expect we will end up wealthwise in the top 20% of households who average $A2.2 million.

Sunday, October 09, 2011

Costco

We went to the (relatively) new Costco store at Canberra airport today. You have to buy a membership ($A60 p.a.) before you can look inside the store, though the membership is refundable. Some things are very cheap and others are near prices at other discount stores. For example, wine sells for the same price as 1st Choice Liquor. Levis 501 jeans were on sale for a price lower than in a Levis outlet in Los Angeles we were recently at (i.e. just $A45). Post-it notes etc. were about half the price that they are at OfficeWorks. We mainly bought food. Things do come in large sizes but there are some smaller ones too. You can buy a regular 3 litre bottle of milk, 250 gram Camembert cheese etc. and individual cakes etc. as well as the larger sizes. The price for TVs was the same as Harvey Norman.

If you are already shopping at 1st Choice, Aldi, and fresh food markets you probably won't save a huge amount in Costco and the range is limited.

We ended up spending $A155.93 somehow or other...

If you are already shopping at 1st Choice, Aldi, and fresh food markets you probably won't save a huge amount in Costco and the range is limited.

We ended up spending $A155.93 somehow or other...

Thursday, October 06, 2011

Moominvalley Report September 2011

Another month of negative returns. Seven straight months of losses. Returns in USD terms were heavily affected by the rise in the US Dollar which reduced the value of all our non-USD investments. As a result net worth fell by $US56k:

In Australian Dollar terms the loss was "only" $A11k. The USD rate of return was -13.26% compared with the MSCI World Index's loss of 9.4%. In AUD terms we lost 4.38% and in currency neutral terms 6.07%. Expenditure was high. We went to the US and bought a lot of stuff there - clothes, kitchen stuff, a new camera etc. Our first trip back since we left in 2007. I don't really feel like writing a lot more about this.

P.S.

In response to the comment from Financial Independence, I've introduced a new format for these monthly income/expenditure statements. Hopefully, they give more intuition about how the numbers are calculated.

In Australian Dollar terms the loss was "only" $A11k. The USD rate of return was -13.26% compared with the MSCI World Index's loss of 9.4%. In AUD terms we lost 4.38% and in currency neutral terms 6.07%. Expenditure was high. We went to the US and bought a lot of stuff there - clothes, kitchen stuff, a new camera etc. Our first trip back since we left in 2007. I don't really feel like writing a lot more about this.

P.S.

In response to the comment from Financial Independence, I've introduced a new format for these monthly income/expenditure statements. Hopefully, they give more intuition about how the numbers are calculated.

Get Done What You Want to Do Now

I just heard that Steve Jobs died at age 56. I felt sad but my immediate thoughts were that he got on with doing the big things he wanted to do and it's good he did because he died relatively young. I've often commented (in contrast to some but not all personal finance bloggers) on not worrying too much about saving for retirement over more immediate life goals and not putting off dreams until you "retire". This just reinforces it. Also in the news is the Nobel Prize in Physics awarded to ANU astronomer Brian Schmidt (and two Americans). He is just over two years younger than me and the key paper that won the prize was published in 1998 when he was just 31. Of course, this is the advice that Steve Jobs himself gave in his graduation address at Stanford.

Monday, October 03, 2011

Moominmama Portfolio Performance September 2011

The portfolio got slammed this month by a double whammy - stock markets fell with the MSCI World Index falling 9.4% and the US Dollar rose sharply with the Euro falling more than 9% and other currencies by smaller amounts. The loss was 6.55%. The least badly performing areas were hedge funds and commodities. The Man/AHL managed futures fund actually gained just under 1%.

Wednesday, September 21, 2011

Google Plus

Google finally opened Google Plus to anyone who wants to join rather than by invitation only. So I joined to see what it was about. I get this one even less than Facebook so far. It invites me to add names to circles, but I get no indication of whether people I know are already on Google Plus. I'm mystified. I guess I'm "doing it wrong". Any enlightenment?

Tuesday, September 20, 2011

Rome

I was just invited to come and talk in Rome. But I turned it down. I think I will have done enough traveling for the year and I don't feel particularly expert in the specifics that they are interested in. I don't see it adding a lot professionally in other ways. It's more like a training session for the participants (from developing countries) from what I can understand. It's a pity because I like Rome and I have a friend I could visit there and even in theory visit family from there. But that's a big trip and would take me away from Snork Maiden for a long time and she isn't very keen on that. So, I think I'll stay home this time. I expect only to get more such invites in the future.

Monday, September 19, 2011

Consulting

How much should I charge as a consultant? My employer allows us to spend 20% of our time on consulting. So I figure I should take my salary + employer retirement contributions and divide by 4*52 days to work out a daily rate. And add on any expenses too, of course. Snork Maiden thinks that is too low. And it seems to be lower than what one of my colleagues quoted. I'm not really interested in making money from this project but more about developing a long-term relationship with the client which would be valuable in terms of science and policy impact. I wouldn't really spend time consulting for a purely commercial client as I think we don't need the money. Unless they offered a really large amount of money of course :)

Thursday, September 15, 2011

Four Years in Australia

We arrived in Australia four years ago today. From today Snork Maiden can apply for Australian citizenship, though now she doesn't seem to be in so much of a hurry to do that now. She just got a visa to visit the US (Australian citizens don't need visas) so won't bother with the citizenship until getting back from the US. We're still living in the same apartment as we were when we got here. We're now earning a lot more money but our net worth is about the same due to the financial crisis that intervened. I got a permanent job though Snork Maiden hasn't yet. There is still plenty of demand to hire her on a temporary basis for the next couple of years. But she hasn't looked for a permanent position outside her current employer and they are taking their time. Lots else has happened in the last four years too. We got married. We've travelled to Europe and Asia and around Australia. We've had people come visit here...

Cambria to Offer More Actively Managed ETFs

Cambria manages the GTAA ETF. Manager Mebane Faber also writes an interesting blog. Now they have filed with the SEC to offer more ETFs.

Monday, September 12, 2011

Getting on Track for a Sustainable Retirement: A Reality Check on Savings and Work

A recent paper by Wade Pfau really overturns some standard ideas about retirement planning. The usual story includes picking a "number", planning how much you need to save to get to the number and starting early with saving in order to benefit from compounding interest. This table from the paper:

shows what percentage of final retirement assets could be explained by accumulated wealth a given number of years before retirement for a bond-stock portfolio simulated over the last century or so for the US. Even with an all bond portfolio only 43% of final wealth could be explained by accumulated assets 10 years from retirement. For stock oriented portfolios very little of the variation could be explained. It's all down to the luck of the market returns in the final 10 years. So tracking net worth doesn't really help much in telling you how much you'll have to retire on after all... Early compounding doesn't make much difference because there isn't much wealth to benefit from compounding.

So what does Pfau recommend? Calculating a minimum safe savings rate based on age, accumulated assets, and allocation. For someone of 55 years old who has saved 4 times their salary and wants to replace 50% of their salary and retire in 10 years and has 60% in stocks, the minimum safe savings rate is 52% of income! For a 50% chance of success of achieving a sustainable retirement only an 18.2% savings rate is needed. Having more wealth earlier does help reduce these rates. Not because of compounding but just in terms of piling up more savings. There are more analyses in the paper of the effect of retiring later etc.

shows what percentage of final retirement assets could be explained by accumulated wealth a given number of years before retirement for a bond-stock portfolio simulated over the last century or so for the US. Even with an all bond portfolio only 43% of final wealth could be explained by accumulated assets 10 years from retirement. For stock oriented portfolios very little of the variation could be explained. It's all down to the luck of the market returns in the final 10 years. So tracking net worth doesn't really help much in telling you how much you'll have to retire on after all... Early compounding doesn't make much difference because there isn't much wealth to benefit from compounding.

So what does Pfau recommend? Calculating a minimum safe savings rate based on age, accumulated assets, and allocation. For someone of 55 years old who has saved 4 times their salary and wants to replace 50% of their salary and retire in 10 years and has 60% in stocks, the minimum safe savings rate is 52% of income! For a 50% chance of success of achieving a sustainable retirement only an 18.2% savings rate is needed. Having more wealth earlier does help reduce these rates. Not because of compounding but just in terms of piling up more savings. There are more analyses in the paper of the effect of retiring later etc.

Thursday, September 08, 2011

Superannuation Trends

This is a graph of our three Australian superannuation (retirement accounts). The green is Snork Maiden who has now been working for four years and accumulated $A50k. The blue is my current account where I worked one part-time job in 2009-2010 and then a full time job from the beginning of 2011 and accumulated about half as much. The red is the account from when I worked in Australia previously that is heavily invested in Australian stocks. So it fluctuated dramatically through the GFC and the recent market correction. The accounts that are currently accumulating were little affected by market fluctuations. They are also much more diversified.

How Much Money Should You Give as a Present if You are Invited to a Wedding?

If you ever wondered how much money to give as a gift at a wedding, there is an "app" for that if the wedding happens to be in Israel. Unfortunately the link is in Hebrew (I can read it...). I wonder if there are similar sites for other countries?

Snork Maiden said that in China RMB 1000-2000 would be expected, which sounds like a lot of money to me as RMB 2000 could be a month's wages for a factory worker or even a new graduate.

Snork Maiden said that in China RMB 1000-2000 would be expected, which sounds like a lot of money to me as RMB 2000 could be a month's wages for a factory worker or even a new graduate.

Thursday, September 01, 2011

Moominvalley August 2011 Report

Six losing months in a row now... The accounts for the month look like this in USD terms:

Non-investment income was very high as was spending. This was a triple pay month - we get paid every two weeks as is the norm in Australia and every few months there is a month with three payments. Also my pay rose as I took on my new position.

But in USD terms we lost 7.25% this month against an MSCI World Index loss of 7.26%. We're now down 9.31% for the year in USD terms while the MSCI has lost 4.19% for the year so far. The Australian Dollar fell back a little to USD 1.07 and so Australian Dollar returns were "only" -4.67%.

Expenditure was very high at $9,743. But a third of this was another long haul plane ticket I bought which I should be reimbursed for (I still need to be reimbursed for my trip to India). Core expenditure was still high. There was about $1000 of medical and dental expenses. We'll get reimbursed about $200 for those.

As a result net worth fell USD 27k to USD 520k and fell AUD 11k to AUD 487k. Due to buying shares asset allocation was pretty much unchanged for the month as stocks fell.

Non-investment income was very high as was spending. This was a triple pay month - we get paid every two weeks as is the norm in Australia and every few months there is a month with three payments. Also my pay rose as I took on my new position.