Half of this month we spent travelling. Given that, spending is fairly modest. The Australian Dollar continued to fall, boosting returns in Australian Dollar terms and reducing them in US Dollar terms. This month's accounts in US Dollars, as usual:

Income was very high as this was a three pay month and we also got some refunds for the travel expenditure. The difference between "Expenditure" and "Core Expenditure" is due to business-related travel spending. Core expenditure gives a better idea of how much we are really spending while the total expenditure is needed to actually make the numbers add up. As a refresh, there are quite a few anomalies in the way I report our accounts. Other income, which is salary and other non-investment income (current income), as well as retirement contributions, is reported after tax and also include the proceeds to net tax refunds. Investment income (both current and retirement) is reported pre-tax including tax credits (Australian "franking credits" and foreign tax paid). We don't actually receive these credits - they reduce our tax bill at the end of the year - so I need to deduct them from the reported investment return to get the actual change in net worth each month. This is because net worth only reflects the actual money in our accounts at the end of each month. If we went to an accrual based system I could also add the value of my capital gains loss tax asset - worth $35k or so - but that would be a big complication for little or no gain. So, I stick with this system which works well for me. I only really care about what we get after tax and what we have now, but I want to see investment returns on a pre-tax basis to compare them with the market indices.

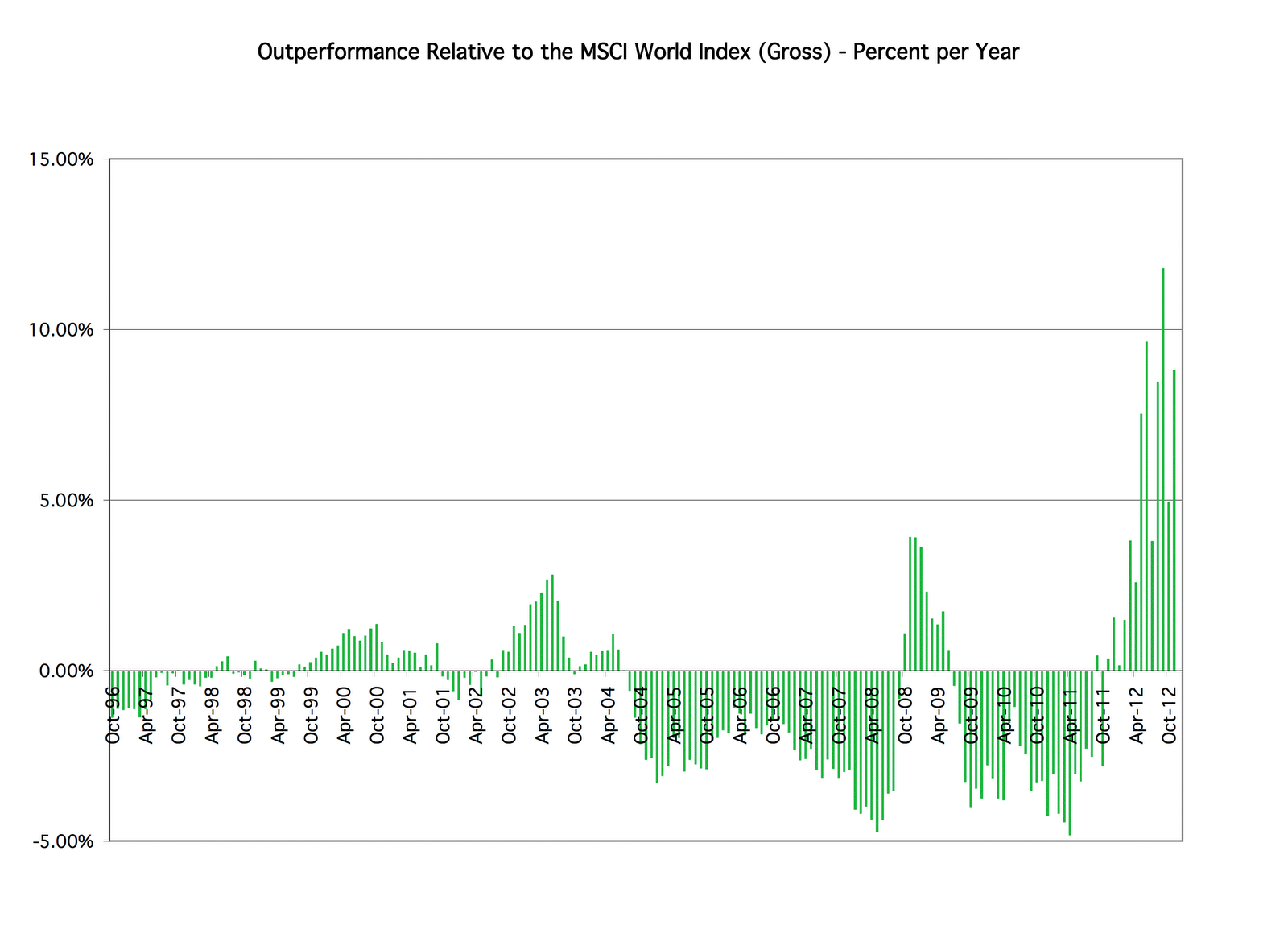

The Australian Dollar fell sharply this month resulting in investment returns in US Dollar terms of 2.33% but in Australian Dollar terms of 4.73%. This again lagged the market. The MSCI gained 4.82% (USD terms) and the S&P 500 5.09%.

Net worth rose in US Dollars by $34k to $861k. In Australian Dollar terms it rose by $A59k to $A961k. This has really been a stratospheric rise since mid 2011:

Income was very high as this was a three pay month and we also got some refunds for the travel expenditure. The difference between "Expenditure" and "Core Expenditure" is due to business-related travel spending. Core expenditure gives a better idea of how much we are really spending while the total expenditure is needed to actually make the numbers add up. As a refresh, there are quite a few anomalies in the way I report our accounts. Other income, which is salary and other non-investment income (current income), as well as retirement contributions, is reported after tax and also include the proceeds to net tax refunds. Investment income (both current and retirement) is reported pre-tax including tax credits (Australian "franking credits" and foreign tax paid). We don't actually receive these credits - they reduce our tax bill at the end of the year - so I need to deduct them from the reported investment return to get the actual change in net worth each month. This is because net worth only reflects the actual money in our accounts at the end of each month. If we went to an accrual based system I could also add the value of my capital gains loss tax asset - worth $35k or so - but that would be a big complication for little or no gain. So, I stick with this system which works well for me. I only really care about what we get after tax and what we have now, but I want to see investment returns on a pre-tax basis to compare them with the market indices.

The Australian Dollar fell sharply this month resulting in investment returns in US Dollar terms of 2.33% but in Australian Dollar terms of 4.73%. This again lagged the market. The MSCI gained 4.82% (USD terms) and the S&P 500 5.09%.

Net worth rose in US Dollars by $34k to $861k. In Australian Dollar terms it rose by $A59k to $A961k. This has really been a stratospheric rise since mid 2011:

Non-retirement profits in AUD terms also finally got above zero again. Profits on retirement accounts are well above the pre-GFC high: