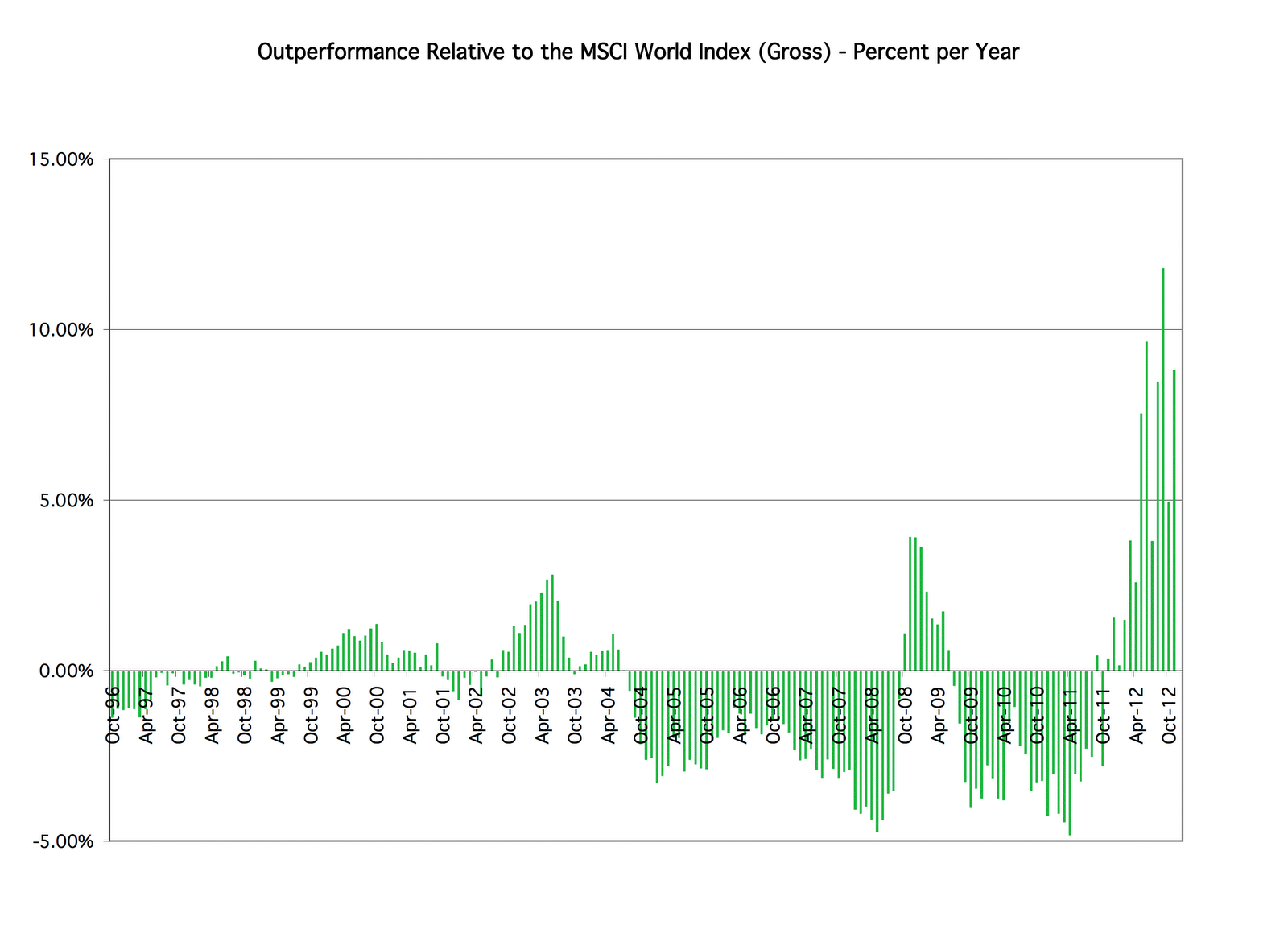

It's easy to get real time information on a wide range of stock market indices and historical data on a daily basis from sites like Yahoo Finance. But getting data on accumulation indices is much harder. Accumulation indices or in US terminology "total return indexes" include dividends in the index return. So they track how much your money would be worth if you could invest in the index and then reinvest all dividends without paying taxes or management fees. I have collected data on the MSCI All Country World Index and S&P500 total return index going back to 1996. My current sources for these indices are here and here.

The MSCI site allows you to select different pages of index returns using menus. I use the ACWI for the Developed and Developing Country, Gross returns, and Standard (midcap and large cap) options. Gross returns also include tax credits. I would include small caps, but that data wasn't available when I started following the series. You can select the data for any date you like.

At the S&P website you need to get the daily fact sheet on each index which includes price only and total return indices. The only way to get exact end of calendar month data is to collect it on the last day of each month. It seems that you now need to subscribe to get historical data. They used to provide a few months for free. You can get Australian indices here as well as the US ones I usually collect from here.

Bigchrisb recently linked to another source for the Australian ASX200 accumulation index - statistics provided by the Reserve Bank of Australia. You can get monthly data for a few recent years there.

The MSCI site allows you to select different pages of index returns using menus. I use the ACWI for the Developed and Developing Country, Gross returns, and Standard (midcap and large cap) options. Gross returns also include tax credits. I would include small caps, but that data wasn't available when I started following the series. You can select the data for any date you like.

At the S&P website you need to get the daily fact sheet on each index which includes price only and total return indices. The only way to get exact end of calendar month data is to collect it on the last day of each month. It seems that you now need to subscribe to get historical data. They used to provide a few months for free. You can get Australian indices here as well as the US ones I usually collect from here.

Bigchrisb recently linked to another source for the Australian ASX200 accumulation index - statistics provided by the Reserve Bank of Australia. You can get monthly data for a few recent years there.