This month I decided to stop short-term trading again. I think you can make money doing what I was doing, but trading at a size that makes a real difference generates too much anxiety for me. I didn't hear from HSBC on refinancing our mortgage. I sent them one email. Will need to chase them more in January.

The Australian stockmarket fell a bit in December and the Australian Dollar rose, but overseas markets rose. The Australian Dollar rose from USD 0.6764. to USD 0.7023. The MSCI World Index rose 3.56% and the S&P 500 3.02%. On the other hand, the ASX 200 lost 2.08%. All these are total returns including dividends. We gained 0.28% in Australian Dollar terms and 4.11% in US Dollar terms due to the rise in the Australian Dollar. The target portfolio is expected to have lost 0.82% in Australian Dollar terms and the HFRI hedge fund index is expected to have gained 1.07% in US Dollar terms. So, we out-performed all our benchmarks, which is rather unusual. Updating the monthly AUD returns chart:

MSCI is negative here in December because of the rise in the Australian Dollar. We haven't lost money on a monthly basis in Australian Dollar terms since November 2018... The Australian stockmarket fell a bit in December and the Australian Dollar rose, but overseas markets rose. The Australian Dollar rose from USD 0.6764. to USD 0.7023. The MSCI World Index rose 3.56% and the S&P 500 3.02%. On the other hand, the ASX 200 lost 2.08%. All these are total returns including dividends. We gained 0.28% in Australian Dollar terms and 4.11% in US Dollar terms due to the rise in the Australian Dollar. The target portfolio is expected to have lost 0.82% in Australian Dollar terms and the HFRI hedge fund index is expected to have gained 1.07% in US Dollar terms. So, we out-performed all our benchmarks, which is rather unusual. Updating the monthly AUD returns chart:

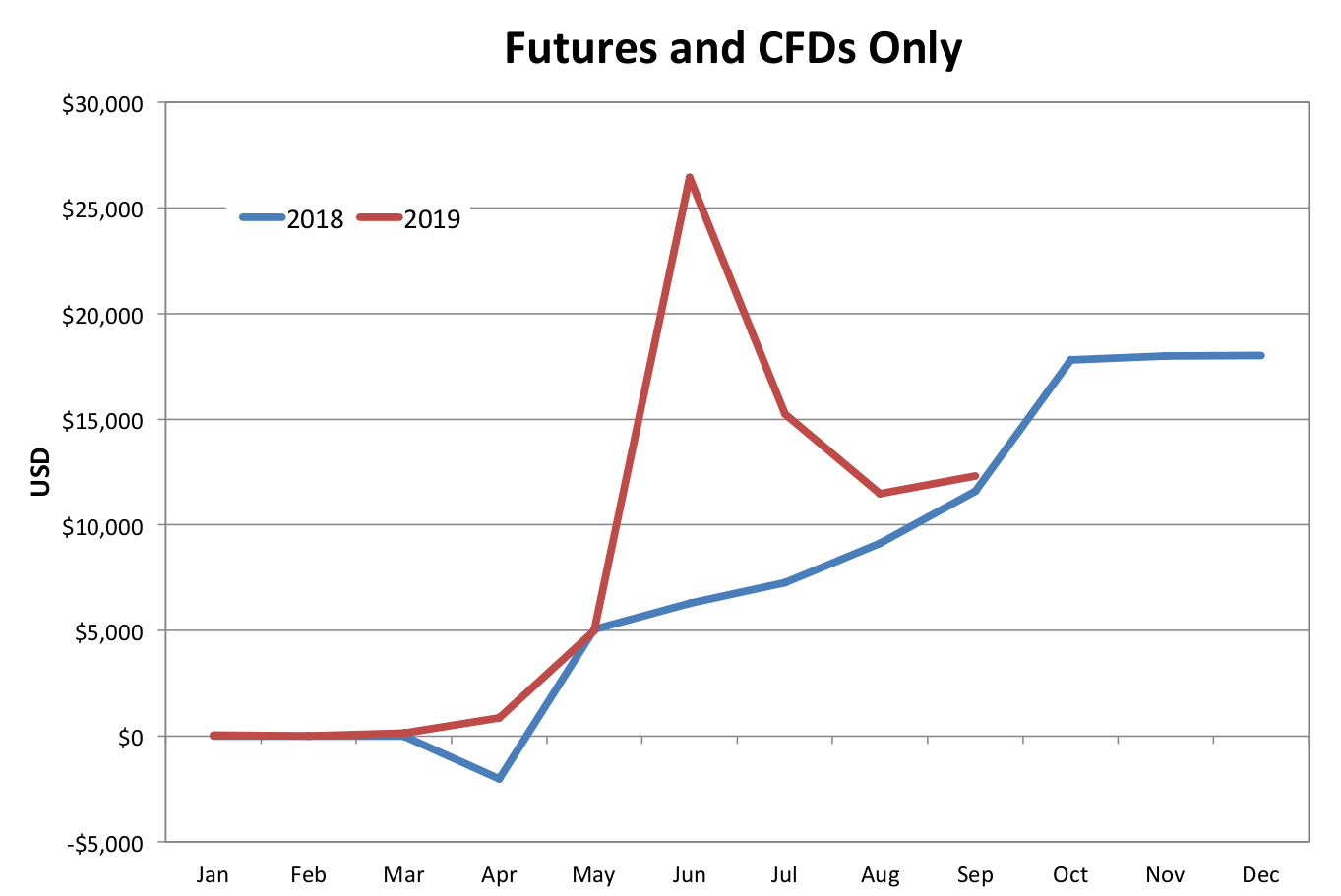

Here is a report on the performance of investments by asset class (futures includes managed futures and futures trading):

Things that worked well this month:

- Hedge funds Platinum Capital/International Fund and Tribeca did very well. Tribeca (TGF.AX) is no longer our worst ever investment in dollar terms, though it is still hugely drawn down.

- Gold did well, almost reaching this year's highs again.

- Bitcoin lost heavily and we stopped trading it.

This is what the target portfolio would look like:

On a regular basis, we invest AUD 2k monthly in a set of managed funds, and there are also retirement contributions. Other moves this month:

- USD15k of Ford bonds were called and we didn't buy any new bonds.

- We bought AUD 40k by selling US Dollars.

- We traded very badly...

- We bought 500 shares of a Commonwealth Bank hybrid (CBAPI).