I am wondering whether to continue this blog as the only thing I have posted recently are these monthly reports and now we are above US$1 million dollars in net worth and things seem to be mostly smooth sailing it is not so interesting. I originally started the blog partly to help me be more responsible with trading as I had to report monthly on what was happening. I haven't done much trading since the GFC. Also, it was a way for Snork Maiden to read about our financial situation, which she pretty much totally leaves up to me to take care of. It doesn't seem that Snork Maiden reads the blog much any more either. And I am guessing that at these levels of net worth and income it is not something that a lot of the people reading PF blogs will be able to relate to. Many of the bloggers who used to report detailed numbers dropped them after they became a success in PF terms and relatively wealthy. Anyway, I haven't quite given up yet and I see that the posts do get a few views still, so here is another monthly report.

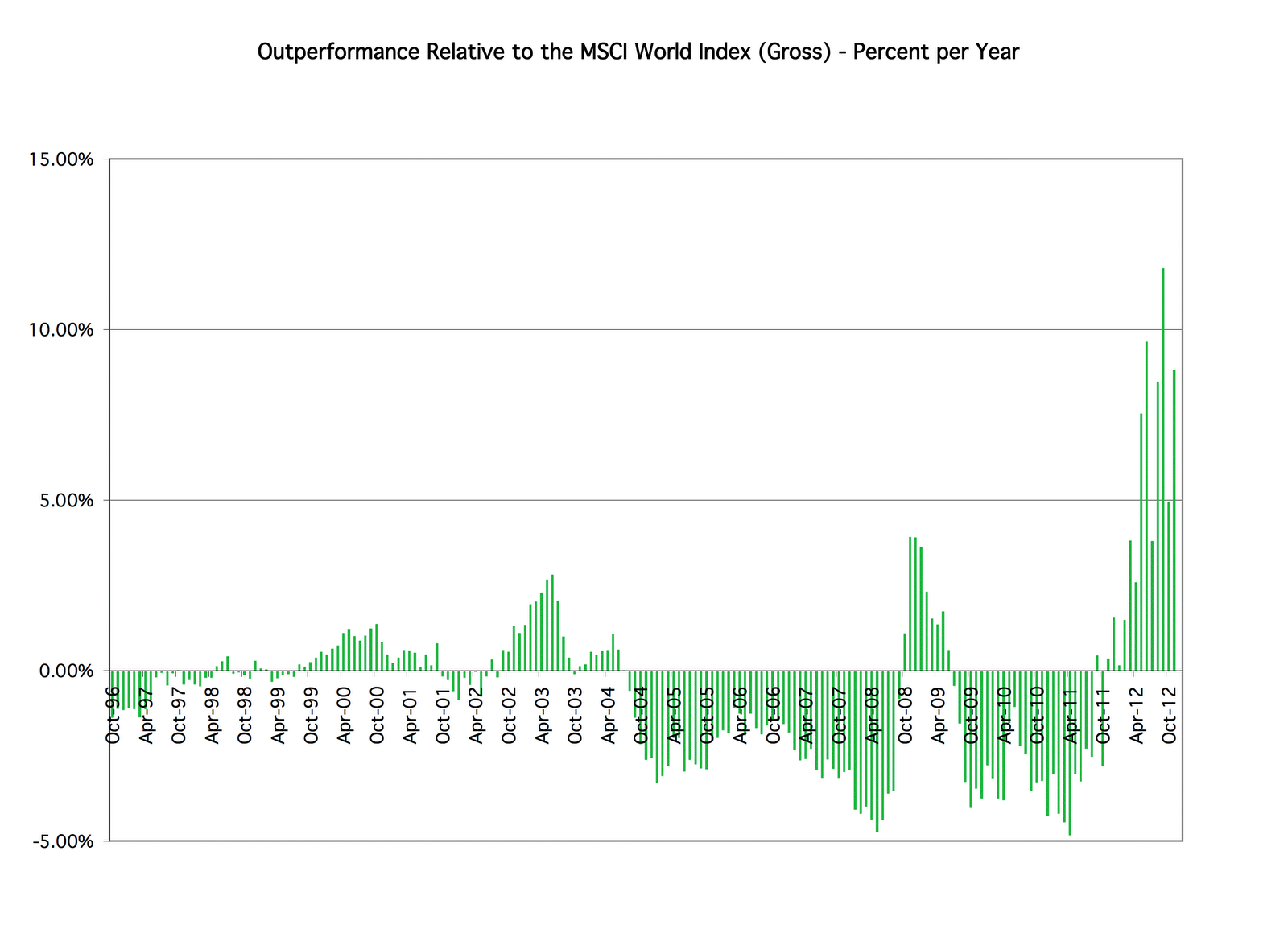

The Australian Dollar increased further this month from $US0.8933 to $US0.9274. This depressed gains in net worth in Australian Dollar terms. Stock markets rose a little. The MSCI World Index rose 0.50%, the S&P 500, 0.84%, and the ASX200 0.29%. We gained 3.02% in US Dollar terms and lost 0.77% in Australian Dollar terms. So we beat the world markets but not the Australian stock market. Net worth rose $5k to $1.148 million in Australian Dollars and rose $US43k to $US1.065 million. The monthly accounts (in AUD now) follow:

Other income is income not from investments or retirement contributions. It was normal this month at $14.6k. Spending was low this month at $4.3k but after adjustments it was an average $5.5k. As a result, we saved $10.3k from regular income

We lost $8.8k on investments. $5.1k of the loss was due to the rise in the Australian Dollar. The asset class that did best this month was hedge funds, but that is because I did some trading in shares of Platinum Capital. Private equity was the only other asset class with a positive return.

The Australian Dollar increased further this month from $US0.8933 to $US0.9274. This depressed gains in net worth in Australian Dollar terms. Stock markets rose a little. The MSCI World Index rose 0.50%, the S&P 500, 0.84%, and the ASX200 0.29%. We gained 3.02% in US Dollar terms and lost 0.77% in Australian Dollar terms. So we beat the world markets but not the Australian stock market. Net worth rose $5k to $1.148 million in Australian Dollars and rose $US43k to $US1.065 million. The monthly accounts (in AUD now) follow:

Other income is income not from investments or retirement contributions. It was normal this month at $14.6k. Spending was low this month at $4.3k but after adjustments it was an average $5.5k. As a result, we saved $10.3k from regular income

We lost $8.8k on investments. $5.1k of the loss was due to the rise in the Australian Dollar. The asset class that did best this month was hedge funds, but that is because I did some trading in shares of Platinum Capital. Private equity was the only other asset class with a positive return.