This blog hasn't really been about saving money in terms of spending less. But facing a year with negative returns and maybe even a fall in net worth in the end, I have focused on cutting expenditure and costs. By switching our car insurance from a comprehensive policy to a third party property damage policy I saved about AUD 400 a year. A reduction from about AUD 675 to AUD 175. The insurance company only values our car at AUD 2,300 and the excess is AUD 695. So, it just didn't make sense to me to insure the car itself. On the new policy we can still get a payout if our car is damaged in an accident by an uninsured driver.

Recently we also called a plumber to look at all the faulty taps in the house. They can't repair taps with ceramic disks and so I decided to just replace all the 7 sets of taps in the house. The plumber told me that I can save money by going buying the taps myself and then getting them to install them. Saving is about $500. So, today we went to a bathroom/plumbing store and selected and ordered taps.

I wonder what Ramit would think about all this?

I got a message from Interactive Brokers that I needed to renew my wholesale investor status as two years had passed since I submitted an accountant's certificate. They currently only allow retail investors to borrow a maximum of AUD 50k in margin loans. The accountant agreed to do it again and I sent her all the relevant material to prove my net worth was more than AUD 2.5 million that took me 2-3 hours to put together. I came up with a number of AUD 3.7 million – the test is done on an individual not family basis – and so thought it would be easy. But now she has come back and said she can't include any superannuation in the number! So she estimates my net worth for the purpose of the test is AUD 2.4 million. She suggested I get a professional valuation of my house to prove the higher number I suggested for it (AUD 1.25 million).

It doesn't make any sense to me that an SMSF would be excluded but home equity included.

Anyway, I looked carefully at my Interactive Brokers account. Currently, I could borrow a maximum of AUD 96k. The saving in interest per year for the amount above 50k compared to CommSec is about AUD 5k. But I am unlikely to borrow that much, as I don't want to get a margin call if things go pear-shaped. So, I've decided not to do the property valuation, because it might come in lower and I still wouldn't qualify. I will wait till when I actually want to borrow more or make a new venture capital investment in Australia and I am closer to qualifying.

Of course, it is much easier to qualify as an accredited investor under US rules. Moominmama qualified in order to participate in AngelList even though her net worth including super is definitely under AUD 2.5 million.

Spending on childcare and education is by far our largest spending category now and has gone up steeply. We are now at AUD 47k for the last 12 months, which is 30% of spending. So, I was wondering where all that money was going:

Turns out that we are spending twice as much on daycare for the 3 year old as on private school for the 6 year old. We get little childcare subsidy. We also spent $4k on deposits for the two children to start at a new private school in 2024. We shouldn't have that expenditure again and the government wants to increase childcare subsidies. So, perhaps this is peak expenditure on this category in real terms until they are both in high school? School fees first fall and then increase again with age.

I read in the Australian Financial Review that having an offset facility usually means that the mortgage interest rate that you are paying is higher and that this gap is biggest at the Commonwealth Bank, where we have our mortgage and offset account. The article said that the gap could be as big as 1.91%! I don't remember this being explained to me when we got our mortgage and offset account though I did discuss with the salesperson whether we should get an offset account.

I have wondered why our mortgage rate was so high and tried to move our mortgage to HSBC to get a lower rate. They just continually ran me around and nothing ever happened. So, I gave up on that.

So, I phoned the bank and he told me that I should phone regularly to "review my discounts", which I have never done. Basically, there is a seniority discount - the longer you are with the bank the more the discount. So the standard rate for the offset account is actually 6.3%. I was paying 5.4%. He increased the discount from 0.9% to 2.29%, lowering my mortgage rate to 4.01%. If I switched to the no frills product cited in the AFR he could only give me a 0.2% discount off the 5.53% standard rate.

I estimate the gain in net worth at the end of the mortgage, assuming we don't pay off the mortgage any faster, is AUD 271k at 6% inflation and AUD 188k at 3% future inflation. The saved interest is in the ballpark of AUD 90k. It feels weird to earn that much for about an hour's work.

August was a mixed month. The MSCI World Index (USD gross) lost by 3.64% and the S&P 500 lost 4.08% in USD terms, but the ASX 200 gained 1.43% in AUD terms. All these are total returns including dividends. The Australian Dollar fell from USD 0.6968 to USD 0.6855 but it rose against the Pound from one Pound buying AUD 1.7430 to AUD 1.6958. We gained 0.25% in Australian Dollar terms but lost 1.38% in US Dollar terms. The target portfolio lost 0.71% in Australian Dollar terms and the HFRI hedge fund index rose 0.50% in US Dollar terms. So, we out-performed three benchmarks and under-performed two.

Here is a report on the performance of investments by asset class:

The asset class returns are in currency neutral returns as the rate of return on gross assets. I have added in the contributions of leverage and other costs and the Australian Dollar to the AUD net worth return.

Hedge funds were the biggest contributor to performance followed by futures, which had the strongest return. US stocks were the worst performer followed by gold and rest of the world stocks.

Things that worked well this month:

What really didn't work:

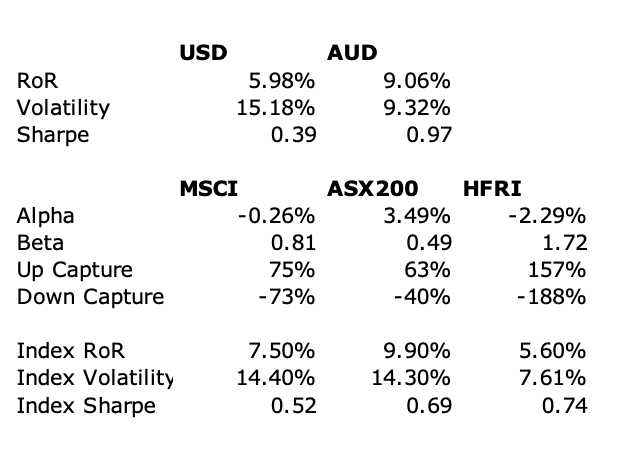

The investment performance statistics for the last five years are:

The first three rows are our unadjusted performance numbers in US and Australian dollar terms. The following four lines compare performance against each of the three indices over the last 60 months. The final three rows report the performance of the three indices themselves. We show the desired asymmetric capture and positive alpha against the ASX200 but not against the hedge fund index nor the MSCI. Compared to the ASX200, our rate of return has only been 0.6% lower, but our volatility has been 5% lower. We are performing 2% per annum worse than the average hedge fund levered 1.7 times.

We moved a bit away from our target allocation. Our actual allocation currently looks like this:

About 70% of our portfolio is in what are often considered to be alternative assets: real estate, art, hedge funds, private equity, gold, and futures. A lot of these are listed investments or investments with daily, monthly, or quarterly liquidity, so our portfolio is not as illiquid as you might think.

We receive employer contributions to superannuation every two weeks. We are now contributing USD 10k each quarter to Unpopular Ventures Rolling Fund and less frequently there will be capital calls from Aura Venture Fund II. In addition we made the following investment moves this month:

I transferred USD 1,000 from Interactive Brokers to the HSBC Everyday Global Account. I was surprised to find that they converted it to Australian Dollars. I am confused about whether I did something wrong or not. I posted a question about it in the mobile chat and the app said it was still learning and didn't understand and a consultant would get back to me.

P.S. 30Aug22

So, the consultant explained that first you have to add the US Dollar "product" to your account before you can transfer US Dollars to your account. I now applied and was approved.

Even if I get this working properly this is a slow method of converting currency. First I need to transfer money to IB, then wait before I am allowed to withdraw it again, then wait while the transfer to HSBC happens, then do another transfer. Of course, we could simply have lots of US Dollars lying around at HSBC just in case, but there is an interest cost to doing that... So all this might be too much hassle.

For September's investment in Unpopular Ventures, I'm planning to sell some shares at IB and then transfer US Dollars to HSBC and see how it goes.

P.P.S. 30Aug22

So now I know when you get the 2% cashback on debit card purchases. You need to deposit at least $2,000 a month into the account. That is a tremendous rate of return compared to passing that spending money through our offset account - about 5 times the rate of return. So, I am going to get Moominmama's salary deposited to this account in future. I'm not sure about opening one myself as I have a lot lower rate of spending on a debit/credit card.

This year's tax returns include large amounts of franking credits connected to Australian dividends. I almost managed to wipe out Moominmama's tax bill with them. The franking credits are added to income and then deducted from the tax bill. As the corporate tax rate for large companies is 30%, if you are in the 34.5% marginal tax bracket (including the Medicare Levy) like she is, it would seem that franked dividends will slightly increase your tax bill. Say you got a $1,000 dividend including the franking credit. Your tax on the dividend as a whole is $345 and you deduct the $300 franking credit from that, paying $45 in tax on the dividend. The magic of franking credits is that if you have investment deductions like margin interest, you will end up with surplus credits. Let's say you have $500 in margin interest in this example. Then your tax on the net $500 in income is $172.50. After deducting the franking credit from this, you have $127.50 in tax credits, which you can apply against the tax on your salary etc.

Foreign source income tax offsets work in a similar way. These are tax paid to foreign governments on dividends etc. Finally, there are also Early Stage Venture Capital Limited Partnership tax offsets. If you invest in an ESVCLP you can get a credit worth up to 10% of your investment. This totally offsets tax on other income even without any deductions!

Over time, the amount of franking credits and foreign source income tax offsets we have received has increased, as you would expect, though this year's credits are off the scale:

This doesn't include any tax credits received by our SMSF or any other superannuation fund for that matter.

I also did Moominmama's taxes for this financial year. The post about last year's taxes is here. Here is a summary of her tax return for this year:

Her salary was up steeply this year, as last year large superannuation contributions were deducted from it. This year, we redirected those to our new SMSF. Australian dividends were up dramatically as I tried to get more investments in her name. Gross income fell by 15% though because of reduced capital gains.

Total deductions rose by 66%, mainly because of the $20k in contributions to the SMSF. As a result, net income fell 32% mainly I think because of the reduced capital gains this year.

Gross tax applies the tax bracket rates to taxable income. Most of this nominal tax was eliminated by the 208% increase in franking credits. As a result, she should be assessed for only $1.4k in tax. As this is much less than the tax withheld from her salary, I expect she will get a refund of around $4k.

This year, I've prepared our tax returns earlier than usual as I have already received all the required information. Here is a summary of my taxes. Last year's taxes are here. To make things clearer, I reclassify a few items compared to the actual tax form. Of course, everything is in Australian Dollars.

On the income side, Australian dividends and franked distributions from managed funds are again up strongly. My salary still dominates my income sources but only increased by 3%.

A big chunk of foreign source income is from the distribution from Aspect Diversified Futures Fund. As a result, I am moving that holding into the SMSF. Net capital gain is zero due mainly to some strategic sales ton generate losses. I am carrying forward $99k in capital losses, which is double what was brought forward from last year.

In total, gross income grew 8%.

Deductions fell 47% because last year they included the loss on Virgin Australia bonds. Most deductions are interest including the $14k in other deductions.

Net income rose as a result by 26%.

Gross tax is computed by applying the rates in the tax table to the net income. In Australia, you don't enter the tax due in your tax return, but I like to compute it so that I know how big or small my refund will be.

Franking credits (from Australian dividends), foreign tax paid, and the

Early Stage Venture Capital (ESVCLP) offset (none this year as there were no capital calls from Aura) are all deducted from gross

tax to arrive at the tax assessment.

Estimated assessed tax rose 47%.

I estimate that I will pay 28% of net income in tax. Tax was withheld on my salary at an average rate of 31%. I already paid $6,546 in tax installments and so estimate that I need to pay an additional $2,829 in tax.

Inspired by Jessica Irvine's article on health insurance in the Sydney Morning Herald (I get her weekly newsletter), I phoned BUPA a couple of times and reduced our monthly health insurance premium from AUD 596 to about AUD 530. I switched the hospital coverage from gold (which we wanted when Moominmama was pregnant) to silver advanced (which is probably still too much coverage) and the extras from Budget Extras to Freedom 50. I think we should probably just drop the extras but Moominmama seems to think we'll use it. I'll monitor after a year or two and see if we are getting our money's worth. I estimate that the extra tax we would have to pay if we didn't have private health insurance is about AUD 370 a month. Moominmama likes private health insurance (and private schools etc.) whereas I don't get the point, really.

.jpg)

Back at the beginning of 2021 I opened an HSBC account for Moominmama because Plus 500 refused to send money to an account in our joint names. Moominmama has just been using it for shopping getting 2% cashback some months. I just realised that it can hold foreign currencies. So, instead of using OFX to convert and transfer money to the US to invest in Unpopular Ventures and Masterworks I could convert the money at Interactive Brokers at the best exchange rate, transfer it to HSBC and then transfer it to the recipient from there for an AUD 30 fee. OFX have about a 1.4% exchange rate cost plus an AUD 15 fee for small orders. And one day when there are distributions from Unpopular Ventures we could transfer the money back to HSBC without converting it.

I just calculated the return on my TIAA-CREF 403b in Australian Dollar terms to compare to our Australian superannuation funds. While the SMSF has done a lot better than Unisuper and PSS(AP) since inception, TIAA has really shone. This is mainly due to our investment in the TIAA Real Estate Fund and partly due to the fall in the Australian Dollar. Now, I am wondering whether to switch out of that fund.

Pre-tax returns for the 2021-22 financial year were: SMSF 2.6%, Unisuper -5.0%, PSS(AP) -2.9%, TIAA-CREF 28.5%. I am very generous in estimating the tax paid by Unisuper and PSS(AP). This boosts estimated pre-tax returns on the way up a little but detracts a bit on the way down.

With the final private asset valuations complete, I am ready to present the June accounts. I needn't have waited, as the share price of Aura VF1 only rose by one cent and Aura VF2's share price was constant.

World markets fell sharply with the MSCI World Index (USD gross) falling by 8.39% and the S&P 500 by 8.25%. The ASX 200 fell 7.72%. All these are total returns including dividends. The Australian Dollar fell from USD 0.7177 to USD 0.6900 increasing Australian Dollar returns and reducing USD returns. We lost 5.82% in Australian Dollar terms or 9.46% in US Dollar terms. The target portfolio lost 2.42% in Australian Dollar terms and the HFRI hedge fund index lost 3.08% in US Dollar terms. So, we under-performed all benchmarks apart from the ASX.

Here is a report on the performance of investments by asset class (currency neutral returns in terms of gross assets):

Things that worked well this month:

What really didn't work:

We moved a bit nearer to our target allocation. Our actual allocation currently looks like this:

70% of our portfolio is in what are often considered to be alternative assets: real estate, art, hedge funds, private equity, gold, and futures. A lot of these are listed investments or investments with daily, monthly, or quarterly liquidity, so our portfolio is not as illiquid as you might think.

We receive employer contributions to superannuation every two weeks. We are now contributing USD 10k each quarter to Unpopular Ventures Rolling Fund and less frequently there will be capital calls from Aura Venture Fund II. In addition we made the following investment moves this month:

July was a reversal of June. The S&P500 gained more than it lost in the previous month and gold fell more than it rose in the previous month. Investors seem to think that the Federal Reserve will raise interest rates by less than originally expected. The MSCI World Index (USD gross) rose by 7.02%, the S&P 500 by 9.22%, and the ASX 200 by 5.77%. All these are total returns including dividends. The Australian Dollar rose from USD 0.6900 to USD 0.6968 increasing Australian Dollar returns and reducing USD returns. We gained 4.11% in Australian Dollar terms or 5.13% in US Dollar terms. The target portfolio gained 3.75% in Australian Dollar terms and the HFRI hedge fund index was up only 1.65% in US Dollar terms. So, we out-performed the latter two benchmarks but under-performed the stock indices. The AUD return for the month is more than what would be expected historically given the ASX 200 performance for the month.

Here is a report on the performance of investments by asset class:

The asset class returns are in currency neutral returns as the rate of return on gross assets. I have for the first time added in the contributions of leverage and the Australian Dollar to the AUD net worth return.

Hedge funds were the biggest contributor to performance while Australian small cap had the best return. Gold was the worst performer and a significant detractor. Rest of the World stocks had a relatively poor performance because of our weighting to the China Fund.

Things that worked well this month:

What really didn't work:

The investment performance statistics for the last five years are:

The first three rows are our unadjusted performance numbers in US and Australian dollar terms. The following four lines compare performance against each of the three indices over the last 60 months. This month, I have added another three rows to report the performance of the three indices themselves. We show the desired asymmetric capture and positive alpha against the ASX200 but not against the hedge fund index and not really against the MSCI. Compared to the ASX200 our rate of return has only been 0.6% lower but our volatility has been 5% lower.

We are performing 2% per annum worse than the average hedge fund levered 1.7 times. I'm not sure why this alpha has deteriorated sharply recently. July 2017, which was dropped from the estimation this month, was a good month for hedge funds but both June and July 2017 were particularly good months for us in USD terms as the Australian Dollar rose sharply.

We moved a bit away from our target allocation. This was mainly because of the redemption of Pershing Square Tontine Holdings that reduced our private equity allocation. Our actual allocation currently looks like this:

70% of our portfolio is in what are often considered to be alternative assets: real estate, art, hedge funds, private equity, gold, and futures. A lot of these are listed investments or investments with daily, monthly, or quarterly liquidity, so our portfolio is not as illiquid as you might think.

We receive employer contributions to superannuation every two weeks. We are now contributing USD 10k each quarter to Unpopular Ventures Rolling Fund and less frequently there will be capital calls from Aura Venture Fund II. In addition we made the following investment moves this month:

A couple of days ago, I went on the Domacom platform just to see if anything was new. I found an offer to sell about 10,000 units in a semi-rural property near Sydney for AUD 1.0156 placed on 30th May. But the property was revalued on 18th July by around 30%!. Almost instantly I bought the units. One downside is that I already own about AUD 10k of units in the neighboring property. Of course, I can't realize this profit, so it is just on paper. The market is very illiquid, which is why I managed to get this bargain in the first place. Both properties have a vote next March on whether to sell the properties and wind up the funds or whether to continue to hold. Recently, my first investment at Domacom held a vote and sold for a big profit.

To get the funds, I had to cancel my pledge to a campaign to buy rural property. My money has been tied up in the campaign for a year while they have made almost no progress on raising money. I think that in future I won't make pledges to campaigns and only engage in the secondary market. The additional advantage of that is that I avoid paying big fees for the purchase of the property and the often huge upfront cut (c. 10%) taken by the promoters of the campaign. It would be much better if they were paid by performance fees instead...

A year on, the career plan needs updating. I agreed with the School Director to take long service leave in 2022 and delay my leadership position to 2023-24. Instead, another person would take that leadership role for one year. Two months into the year, the director became a head of school at another university. The person temporarily filling the leadership position took over as interim director and a third person filled the leadership role. When I raised the issue recently, the person in the leadership role said they knew nothing of the plan to put me into the position in 2023-24 and it would depend on the new permanent school director who will be starting in January 2023. I don't think that the new director would be enthusiastic about me in that role.

Yesterday, I met with my immediate Department Head. He said that he thinks the leadership position is now off the table and doesn't think there will be pressure for me to take that kind of role now... He also wants me to again teach one of the courses I dropped.* The advantage, of course, is that teaching this course won't require any preparation. This new course has taken more preparation that anything I've taught before, I think. I am still working on that as the course began this week, but the end of prep is near... I'm not happy about teaching more again... Anyway, I told him that I would want to teach both courses in the same semester rather than spreading them out over the year. I find switching between teaching and research to be hard and end up wasting a lot of time doing that.

I also told him that I had thought about going to part-time status instead. Yesterday, I sent an email to HR asking about that. But I think that depending partly on investment income is a bit scary given the current economic and market uncertainty. On the other hand, the question is whether I will ever feel like I have enough money to retire....

I'll probably end up teaching the old course again together with the new one this time next year.

* He is teaching it this year (he also taught it before). Next year, he wants to revive another course that we have both taught before....

Sam Dogen of Financial Samurai has first video interview. Finally, you can get to see him, even if you still don't know his real name 😀

Enough Wealth has a new post comparing our two NetWorthShare net worth curves titled a Tale of Two Bloggers. He took out the step changes due to inheritance in both our histories. But the two curves are in different currencies - mine in USD and his in AUD despite us both living in Australia. I wanted my track record to be comparable to the majority of other members who are US based. The volatility of my net worth is much lower in AUD than in USD. This is by design. The Australian Dollar tends to fall during "risk-off" periods reducing losses in AUD terms and increasing them in USD terms.

So, I thought I'd post a comparison of my net worth curve in both AUD and USD terms:

These go back way before the record on NetWorthShare. Back to September 1990, the month I started my PhD in the US... In addition to bigger moves during bear markets, the US series has a number of flat periods compared to the AUD series - around 2015, 2018-19 and in 2021. Overall, the AUD curve ascends more smoothly. We can also reminisce about that time after the GFC when the Australian Dollar was worth more than the US Dollar!

It looks like I will have to pay Division 293 superannuation contributions tax for the first time. This is an extra 15% tax on superannuation contributions that you have to pay if your income including concessional super contributions is above AUD 250k. My preliminary estimate of my taxable income is already above AUD 250k. So, for sure the total including around 30k of super contributions will be even if the final income number is a little lower. This is probably going to mean an extra AUD 4,500 of tax.

I'm also currently estimating I'll owe more than AUD 13k in extra tax after paying AUD 6k in tax installments. Last year I got a tax refund because of the Virgin Australia debacle. Bond losses can be deducted immediately from your income unlike losses on shares. The tax installments were because the previous year's tax return...

I'm reluctant to stuff more money into super as non-concessional contributions to reduce tax in case we'll need it. For example, to buy a bigger or better located house. If I continue to work, we can't withdraw the money from my account till I'm 65 in 8 years time. And much longer in Moominmama's case. That liquidity costs in taxes.

In the last couple of years we made large non-concessional contributions. I also have illiquid investments in venture capital and art. Our liquid investments are 46% of gross assets not including our house. I doubt I can get a bigger mortgage given my age and Moominmama's low wage income.

Masterworks sold Lured by Cecily Brown for USD 1 million. The initial offer price was USD 605k. We are supposed to get the money within a month. I think this is the third painting they have sold, two of which were ones I invested in.

Domacom reported to the ASX that their private placement was over-subscribed! They hope to be reintstated in the ASX soon.

I won't post June accounts for quite a while. There

doesn't seem much point until we have all valuations for private assets

for the end of the financial year and that won't happen till some time

in August probably.

I did a bit of a portfolio planning exercise again with some moves planned. I tweaked the portfolio allocation a little as a result to meet the various constraints. Target allocation to Australian large cap is down from 8% to 7%, hedge fund allocation down from 25% to 24% and bonds and futures both up from 5% to 6%. Other allocations remain unchanged (real assets 15%, private equity 15%, international shares 11%, gold 10%, and cash 1%). Back in 2017, our Australian large cap allocation was 35-36%!

In theory, the new allocation does increase the historical portfolio Sharpe ratio.

So here is the current allocation where I break down by asset class and type of holding:

You are going to need to click on this to see any detail. The names at the bottom are most of the relevant investments in that category. Employer super includes my US retirement account as well. I originally developed this spreadsheet when we were planning the SMSF. Then the future allocation tries to move more towards the long run allocation while taking into account the amount of money in each pot and what the employer super is invested in etc.

It also reflects that we are probably going to get the cash back from our investment in PSTH, which is then reinvested in the SMSF. I want to move my holding of Aspect Diversified Futures into the SMSF I will sell and buy again rather than actually move it as I plan to buy a class with lower fees. With the proceeds from selling Aspect we invest in Australian small cap and international shares. We then use the proceeds from PSTH to buy Aspect in the super fund. Plus a $20k concessional contribution for Moominmama I just made. Otherwise, the allocation says we need to increase holdings of real assets outside of super a lot. I don't know what those investments would be...

For the last five years I've been putting together reports on our spending over the Australian financial year, which runs from 1 July to 30 June. This makes it easy to do a break down of gross income including taxes that's comparable to many you'll see online, though all our numbers are in Australian Dollars. At the top level we can break down total income (as reported in our tax returns plus superannuation contributions):

We break down spending into quite detailed categories. Some of these are then aggregated up into broader categories:

Our biggest spending category, if we don't count tax, is now childcare and education, which has again risen steeply. As mentioned above, the income and tax numbers are all estimates. Commentary on each category follows:

Employer superannuation contributions: These include employer contributions and salary sacrificed contributions but not concessional contributions we paid to the SMSF this year.

Superannuation contributions tax: The 15% tax on concessional superannuation contributions. This year it includes tax on our concessional contributions to the SMSF.

Franking credits: Income reported on our tax returns includes franking credits (tax paid by companies we invest in). We need to deduct this money which we don't receive as cash but is included in gross income. Foreign tax paid is the same story.

Life and disability insurance: I have been trying to bring this under control and the amount paid has fallen as a result.

Health: Includes health insurance and direct spending. Spending peaked with the birth of our second child and continues to decline.

Housing: Includes mortgage interest, maintenance, and body corporate fees (condo association). We haven't spent much on maintenance this year, so spending is down.

Transport: About 2/3 is spending on our car and 1/3 my spending on Uber, e-scooters, buses etc.

Utilities: This includes spending on online subscriptions etc as well as more conventional utilities. I need to cut back on spending on video games as this category continued to climb strongly.

Supermarkets: Includes convenience stores, liquor stores etc as well as supermarkets. Seems crazy that it has almost doubled in five years and become our second biggest spending category.

Restaurants: This was low in 2017-18 because we spent a lot of cash at restaurants. It was low last year because of the pandemic and this year because of a seeming permanent behavior change.

Cash spending: This has collapsed to zero. I mainly use cash to pay Moomin pocket money and he pays me back if we buy stuff online for him. That's how it ended up negative for the year. Moominmama also gets some cash out at supermarkets that is included in that category.

Department stores: All other stores selling goods that aren't supermarkets. No real trend here.

Mail order: This seems to have leveled out in the last three years/

Childcare and education: We are paying for private school for one child, full time daycare for the other, plus music classes, swimming classes...

Travel: This includes flights, hotels etc. It was very high in 2017-18 when we went to Europe and Japan. Last year it was down to zero due to the pandemic and having a small child. This year we went to the nearby coast for a week and this is mostly how much the accommodation, booked at the last minute, cost.

Charity: Not sure why it's down this year.

Other: This is mostly other services. It includes everything from haircuts to professional photography.

This year's increased spending was mainly driven by increased childcare and education costs. I expect these to be about the same next year and then fall for a while in subsequent years - private primary school is cheaper than daycare with the low level of subsidy we get - before beginning to rise again.

Regal Partners just merged with VGI to create a new larger alternative fund manager that will be known by the former name. The company still trades under the VGI.AX ticker but is expected to switch to RPL.AX. It seems undervalued to me at a PE of 6 and so I bought some shares. Especially, as that is based on VGI's inferior track record to date.

World markets stabilized with the MSCI World Index (USD gross) rising by 0.19% and the S&P 500 by 0.18%. On the other hand, the ASX 200 fell 2.43%. All these are total returns including dividends. The Australian Dollar rose from USD 0.7114 to USD 0.7177 increasing Australian Dollar returns and reducing USD returns. Our luck ended this month, and we lost 3.10% in Australian Dollar terms or 2.24% in US Dollar terms. The target portfolio lost 1.05% in Australian Dollar terms and the HFRI hedge fund index is expected to gain 0.21% in US Dollar terms. So, we under-performed all benchmarks.

Here is a report on the performance of investments by asset class (currency neutral returns in terms of gross assets):

Hedge funds were the worst drag on performance followed by gold. Only futures and real assets had positive returns.

Things that worked well this month:

What really didn't work:

The investment performance statistics for the last five years are:

The first two rows are our unadjusted performance numbers in US and Australian dollar terms. The following four lines compare performance against each of the three indices over the last 60 months. We show the desired asymmetric capture and positive alpha against the ASX200 and the MSCI but not against the hedge fund index. We are performing 1% per annum worse than the average hedge fund levered 1.67 times.

We moved a little bit nearer to our target allocation. Our actual allocation currently looks like this:

70% of our portfolio is in what are often considered to be alternative assets: real estate, art, hedge funds, private equity, gold, and futures. A lot of these are listed investments or investments with daily, monthly, or quarterly liquidity, so our portfolio is not as illiquid as you might think. On the other hand, around 47% of net worth (not including our house) are now in retirement accounts. Liquid investments are 57% of net worth and illiquid non-retirement investments are 13% of net worth. Because of leverage, the total is 117%.

We receive employer contributions to superannuation every two weeks. In addition we made the following investment moves this month. It was a busy month.

Unpopular Ventures offered a syndicated investment in the seed round of a start-up based in Europe. I can't give any details of the investment. Based on their projections, which I think look pretty unrealistic, it would be a fantastic investment but they have been growing very rapidly so far, have a lot of experience, and the valuation doesn't seem too crazy.

The investment is basically in a separate fund, where the general partners get 20% carry. They suggested investing USD 2,500 (minimum was USD 1,000) and I did that, following Meb's advice to invest a little in lots of different start-ups. I'm used to investing 1-2% or as little as 1/4% of the portfolio in an investment and this is more like 1/16%. On the one hand, I don't want to make too many different investments because of information overload. On the other hand, I can't do anything about this investment unless there is an exit or opportunity to invest more, so I don't really need to pay much attention to its performance.

After reading the most recent quarterly report I decided to get out of URF. I'm not optimistic that even if the shareholders vote against the sale deal we will eventually realize more for the investment and there is a big risk it is approved and we get less than the current market price. I exited yesterday and today at 27 cents per share for a net loss on the investment of AUD 2,300, which isn't too bad, I guess. Obivously, there are a lot of people thinking differently to me who want to buy in.

The graph tracks the performance of our portfolio (Moom, orange) since the March 2020 low versus various benchmarks. All of these are in Australian Dollar terms. So, for example, we multiply the S&P 500 index by the Australian Dollar - USD exchange rate and track that.

Our portfolio is now a little ahead of the S&P 500 and quite a bit ahead of the MSCI but has had a smoother ride than both. The ASX 200 is ahead of us, but has also been more volatile.The target portfolio (Portfolio, black) also has lower volatility but we have beaten it by fund selection and trading.

No guarantee that this performance continues, but our goal is to achieve market like returns with lower volatility. Also, it isn't as pretty in US Dollar terms. Our strategy is designed to give low volatility in Australian Dollar terms.

World markets fell sharply with the MSCI World Index (USD gross) falling by 7.97%, the S&P 500 falling 8.72%, and the ASX 200 falling 0.85%. All these are total returns including dividends. The Australian Dollar fell from USD 0.7494 to USD 0.7114 increasing Australian Dollar returns and reducing USD returns. We lost only 0.16% in Australian Dollar terms but lost 5.23% in US Dollar terms. The target portfolio lost by 2.34% in Australian Dollar terms and the HFRI hedge fund index is lost 0.93% in US Dollar terms. So, we out-performed all benchmarks apart from the HFRI index. I felt like I was losing a lot of money, but in Australian Dollar terms it wasn't that bad.

Here is a report on the performance of investments by asset class (currency neutral returns in terms of gross assets):

In a reversal of last month real assets, gold, and futures gained money, while other asset classes lost. Real assets were negatively affected by the URF debacle. Rest of the world stocks were negatively affected by the China Fund. Gold rose in Australian Dollar terms, though the USD price fell. US stocks performed worst and detracted from performance most, while gold performed best and contributed most to performance.

Things that worked well this month:

What really didn't work:

Our SMSF continues to perform quite well compared to our employer superannuation funds:

The investment performance statistics for the last five years are:

The first two rows are our unadjusted performance numbers in US and Australian Dollar terms. The following four lines compare performance against each of the three indices over the last 60 months. We show the desired asymmetric capture and positive alpha against the ASX200 and the MSCI but not against the hedge fund index. We are basically performing a bit worse than the average hedge fund levered 1.67 times. Hedge funds have been doing well recently.

I adjusted the leverage on the URF.AX investment to roughly 3:1 in our gross asset allocation as there still seems some possibility that the wind-up deal will be voted down by the shareholders.

We moved a little bit nearer to our target allocation. Our actual allocation currently looks like this:

70% of our portfolio is in what are often considered to be alternative assets: real estate, art, hedge funds, private equity, gold, and futures. We receive employer contributions to superannuation every two weeks. In addition we made the following investment moves this month. It was a busy month.

I invested in another painting at Masterworks, No Hopeless by Yoshitomo Nara:

This takes my investment back up to 12 paintings again, given that Doppelbild by Albert Oehlen was sold and should pay out soon. I was a bit nervous this was overvalued but after a bit of research took the plunge anyway and invested USD 10k.

I also started buying units in a property on Domacom: 60 Devonshire Road, Rossmore, which is a market garden near the planned Badgery's Creek Airport. After the initial investors paid up big fees for the establishment of the investment, it trades below par but at the last valuation saw an uptick in value. I am thinking now it makes more sense to buy in the secondary market on Domacom instead of joining "campaigns" that seem to go nowhere.

So far, I only invested AUD 920, but have a bid open waiting for sellers.

Until now, we only had venture capital investments in Australia through Aura Ventures funds and the listed Wilson Asset Management Alternative Assets Fund (WMA.AX).

I bought a position in Pendal (PDL.AX). Yesterday, they announced that they got a takeover offer from Perpetual (PPT.AX) for the equivalent of AUD 6.23 per share. The price isn't a constant as it is about 2/3 in terms of Perpetual shares. The stock was trading around AUD 5.25 after being higher yesterday, but PPT was trading up on yesterday. Analysts say the stock is undervalued and a strong buy after falling a lot in the last year, prior to the bid. So, I didn't see lot of downside in this.

In other news, URF.AX is now up to AUD 0.24, 10% above the AUD 0.22 that investors are supposed to eventually receive. I can't sell as my shares are in transit from Interactive Brokers to Commonwealth Securities. They have now left Interactive Brokers, but haven't shown up yet at CommSec...

I can see scope for improving the fractional investing product. I find the financial information provided on existing investments to be unclear and non-transparent. The level of explanation really needs to be stepped up to make secondary investors willing to participate and increase market liquidity in my opinion. I have only invested in one secondary investment, which is now exiting. I signed up to several "campaigns" but there is glacial progress on raising funds for them. I just discovered that two of them seem to have given up and released the pledged cash back to investors.

Hopefully, these things will improve going forward. Maybe I should send the new chairman (who is my honorary colleague) a letter with my thoughts :)

World markets rebounded with the MSCI World Index (USD gross) rising by 2.22%, the S&P 500 by 3.71%, and the ASX 200 rising by 7.10%. All these are total returns including dividends. The Australian Dollar rose from USD 0.7248 to USD 0.7494 reducing Australian Dollar returns and increasing USD returns. We gained 1.89% in Australian Dollar terms or 5.35% in US Dollar terms. The target portfolio rose by 0.75% in Australian Dollar terms and the HFRI hedge fund index is expected to rise 1.11% in US Dollar terms. So, we under-performed the ASX200, but outperformed all the other benchmarks.

Here is a report on the performance of investments by asset class (currency neutral returns in terms of gross assets):

Real assets, gold, and rest of the world stocks lost money, while other asset classes gained. Real assets were negatively affected by the URF debacle. Rest of the world stocks were negatively affected by the China Fund. Gold fell in Australian Dollar terms, though the USD price rose. Futures performed best, and hedge funds contributed most to performance.

Things that worked well this month:

What really didn't work:

The investment performance statistics for the last five years are:

I adjusted the leverage on the URF.AX investment down to 1:1 in our gross asset allocation as it is supposedly no longer exposed to movement of the actual real estate portfolio. On the other hand, since the end of the month, the share price has bounced back above the 22 cents which shareholders are supposed to receive as a distribution later this year while the convertible bonds are trading at an 18% discount to face value. This suggests that the market doesn't think that the stated deal is final. After all, URF shareholders need to vote on it.

This changed our asset allocation a lot. Real assets are now the most underweight asset class and hedge funds the most overweight. We moved nearer to the target allocation. Our actual allocation currently looks like this:

70% of our portfolio is in what are often considered to be alternative assets: real estate, art, hedge funds, private equity, gold, and futures. We receive employer contributions to superannuation every two weeks. In addition we made the following investment moves this month: