This year was

less eventful than last year, but I was very busy, mainly with my career and a few international and domestic trips. We also put a lot of effort

into looking for a house, but didn't decide on anything. Snork Maiden got her job turned into a

permanent position. She was recently shocked to find out that she is now earning $A93k per year. And that's not counting 15% superannuation contributions from her employer :)

The last couple of years' career events and a reasonable investment market meant that we hit new records in income and net worth. This is the annual accounts that sum each of

my monthly reports for the year:

The numbers are on an after-tax basis but investments are shown pre-tax and any tax refunds or payments are reported under "other income" which otherwise is mainly from salary. Also the investment returns include tax credits, which reduce our tax bill but don't add to net worth directly. Therefore, these have to be deducted to get to net worth changes. It's an odd way of accounting, but it is the easiest one to put together and it works for me :)

The non-investment income after tax totalled $180k with an additional $40k in retirement contributions. Total investment income was $113k with almost all of it being "core income" and not just the result of exchange rate movements. Spending was actually a few hundred less than last year, so no new record there. That's despite giving $5,000 to Snork Maiden's parents which I counted as spending.

I closed my Roth IRA due to a

bungle by Ameritrade. This results in the transfer of $9k from retirement to current accounts. So, we saved $A106k from non-investment income for the year, or $8,800 per month vs. $6,200 in spending per month. That's a record high savings rate, but only 1% higher than in 2006! I only spent $25.7k back then. I was single and lived in the US in a cheap area.

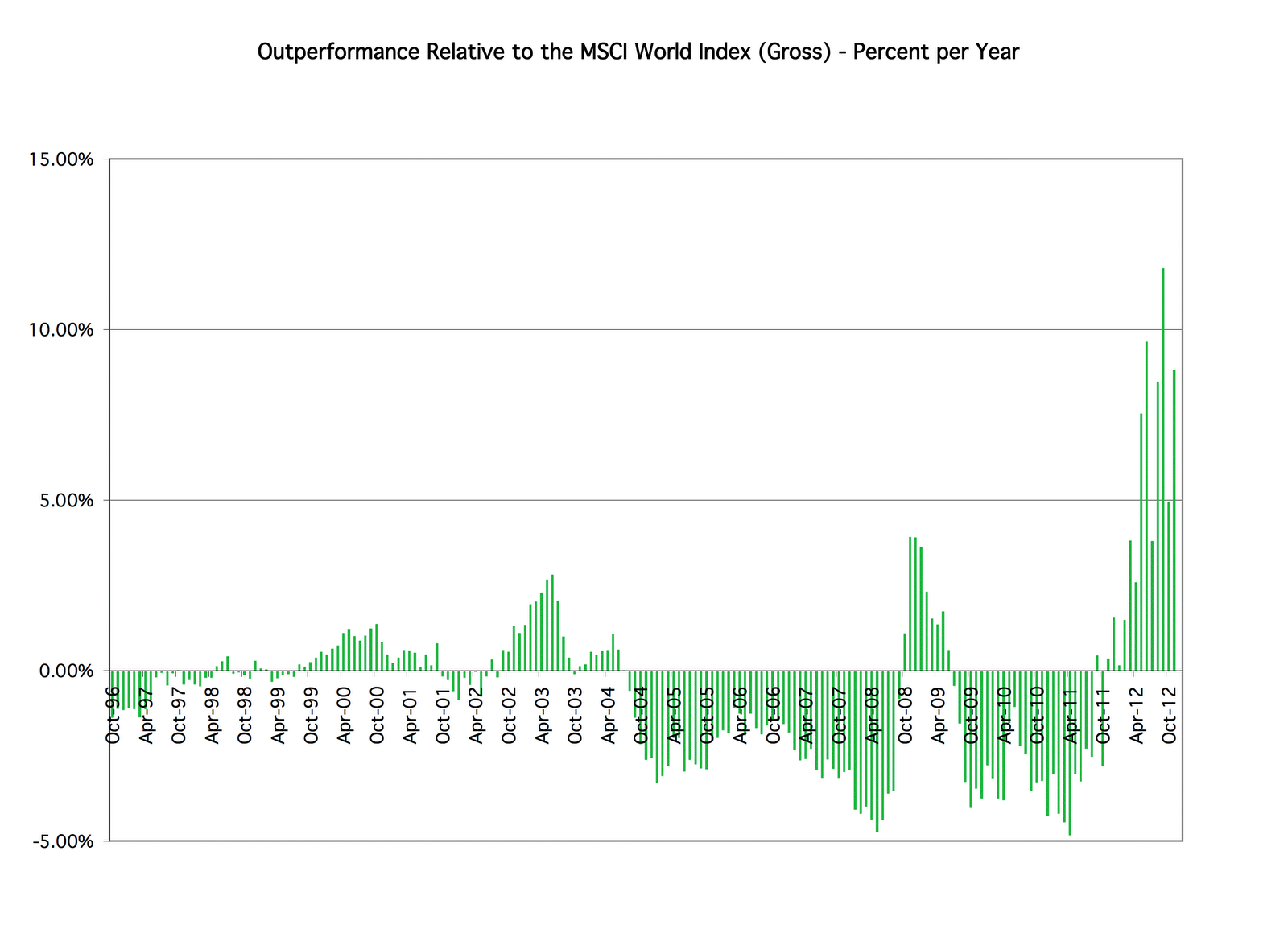

Investment rate of return for the year in USD terms was 18.76% vs. 16.8% for the MSCI. In Australian Dollar terms we made 17.14% (18.11% in currency neutral terms). After the last several years it's good to be making money and doing better than the market.