This blog hasn't really been about saving money in terms of spending less. But facing a year with negative returns and maybe even a fall in net worth in the end, I have focused on cutting expenditure and costs. By switching our car insurance from a comprehensive policy to a third party property damage policy I saved about AUD 400 a year. A reduction from about AUD 675 to AUD 175. The insurance company only values our car at AUD 2,300 and the excess is AUD 695. So, it just didn't make sense to me to insure the car itself. On the new policy we can still get a payout if our car is damaged in an accident by an uninsured driver.

Recently we also called a plumber to look at all the faulty taps in the house. They can't repair taps with ceramic disks and so I decided to just replace all the 7 sets of taps in the house. The plumber told me that I can save money by going buying the taps myself and then getting them to install them. Saving is about $500. So, today we went to a bathroom/plumbing store and selected and ordered taps.

I wonder what Ramit would think about all this?

I got a message from Interactive Brokers that I needed to renew my wholesale investor status as two years had passed since I submitted an accountant's certificate. They currently only allow retail investors to borrow a maximum of AUD 50k in margin loans. The accountant agreed to do it again and I sent her all the relevant material to prove my net worth was more than AUD 2.5 million that took me 2-3 hours to put together. I came up with a number of AUD 3.7 million – the test is done on an individual not family basis – and so thought it would be easy. But now she has come back and said she can't include any superannuation in the number! So she estimates my net worth for the purpose of the test is AUD 2.4 million. She suggested I get a professional valuation of my house to prove the higher number I suggested for it (AUD 1.25 million).

It doesn't make any sense to me that an SMSF would be excluded but home equity included.

Anyway, I looked carefully at my Interactive Brokers account. Currently, I could borrow a maximum of AUD 96k. The saving in interest per year for the amount above 50k compared to CommSec is about AUD 5k. But I am unlikely to borrow that much, as I don't want to get a margin call if things go pear-shaped. So, I've decided not to do the property valuation, because it might come in lower and I still wouldn't qualify. I will wait till when I actually want to borrow more or make a new venture capital investment in Australia and I am closer to qualifying.

Of course, it is much easier to qualify as an accredited investor under US rules. Moominmama qualified in order to participate in AngelList even though her net worth including super is definitely under AUD 2.5 million.

Spending on childcare and education is by far our largest spending category now and has gone up steeply. We are now at AUD 47k for the last 12 months, which is 30% of spending. So, I was wondering where all that money was going:

Turns out that we are spending twice as much on daycare for the 3 year old as on private school for the 6 year old. We get little childcare subsidy. We also spent $4k on deposits for the two children to start at a new private school in 2024. We shouldn't have that expenditure again and the government wants to increase childcare subsidies. So, perhaps this is peak expenditure on this category in real terms until they are both in high school? School fees first fall and then increase again with age.

I read in the Australian Financial Review that having an offset facility usually means that the mortgage interest rate that you are paying is higher and that this gap is biggest at the Commonwealth Bank, where we have our mortgage and offset account. The article said that the gap could be as big as 1.91%! I don't remember this being explained to me when we got our mortgage and offset account though I did discuss with the salesperson whether we should get an offset account.

I have wondered why our mortgage rate was so high and tried to move our mortgage to HSBC to get a lower rate. They just continually ran me around and nothing ever happened. So, I gave up on that.

So, I phoned the bank and he told me that I should phone regularly to "review my discounts", which I have never done. Basically, there is a seniority discount - the longer you are with the bank the more the discount. So the standard rate for the offset account is actually 6.3%. I was paying 5.4%. He increased the discount from 0.9% to 2.29%, lowering my mortgage rate to 4.01%. If I switched to the no frills product cited in the AFR he could only give me a 0.2% discount off the 5.53% standard rate.

I estimate the gain in net worth at the end of the mortgage, assuming we don't pay off the mortgage any faster, is AUD 271k at 6% inflation and AUD 188k at 3% future inflation. The saved interest is in the ballpark of AUD 90k. It feels weird to earn that much for about an hour's work.

August was a mixed month. The MSCI World Index (USD gross) lost by 3.64% and the S&P 500 lost 4.08% in USD terms, but the ASX 200 gained 1.43% in AUD terms. All these are total returns including dividends. The Australian Dollar fell from USD 0.6968 to USD 0.6855 but it rose against the Pound from one Pound buying AUD 1.7430 to AUD 1.6958. We gained 0.25% in Australian Dollar terms but lost 1.38% in US Dollar terms. The target portfolio lost 0.71% in Australian Dollar terms and the HFRI hedge fund index rose 0.50% in US Dollar terms. So, we out-performed three benchmarks and under-performed two.

Here is a report on the performance of investments by asset class:

The asset class returns are in currency neutral returns as the rate of return on gross assets. I have added in the contributions of leverage and other costs and the Australian Dollar to the AUD net worth return.

Hedge funds were the biggest contributor to performance followed by futures, which had the strongest return. US stocks were the worst performer followed by gold and rest of the world stocks.

Things that worked well this month:

What really didn't work:

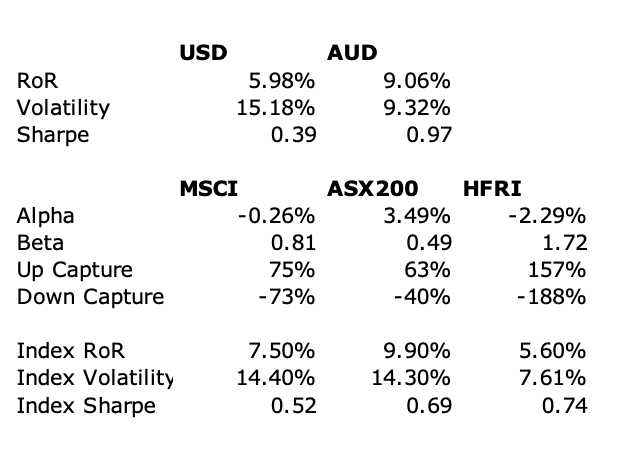

The investment performance statistics for the last five years are:

The first three rows are our unadjusted performance numbers in US and Australian dollar terms. The following four lines compare performance against each of the three indices over the last 60 months. The final three rows report the performance of the three indices themselves. We show the desired asymmetric capture and positive alpha against the ASX200 but not against the hedge fund index nor the MSCI. Compared to the ASX200, our rate of return has only been 0.6% lower, but our volatility has been 5% lower. We are performing 2% per annum worse than the average hedge fund levered 1.7 times.

We moved a bit away from our target allocation. Our actual allocation currently looks like this:

About 70% of our portfolio is in what are often considered to be alternative assets: real estate, art, hedge funds, private equity, gold, and futures. A lot of these are listed investments or investments with daily, monthly, or quarterly liquidity, so our portfolio is not as illiquid as you might think.

We receive employer contributions to superannuation every two weeks. We are now contributing USD 10k each quarter to Unpopular Ventures Rolling Fund and less frequently there will be capital calls from Aura Venture Fund II. In addition we made the following investment moves this month: