Monday, December 23, 2013

Predicting Stock Market Returns

This correlation is pretty amazing. It is also pretty clear that there is causation here too or both variables are driven by the same other causal variables.

Monday, December 02, 2013

Moominvalley November 2013 Report

Turns out that I miscalculated and we didn't quite reach USD 1 million last month. This month due to the fall in the Australian Dollar we are further below it to $975k. In Australian Dollars we reached $1.069 million, up $A14k on last month. The monthly accounts (in USD) follow:

Spending was high this month. First, I had a bunch of business expenses for a trip early next year. Then I had to pay my employer a refund of half the price of an airline ticket for our trip to the Northern Hemisphere this past Northern summer. Otherwise, they decided retrospectively that they would have to pay fringe benefits tax and they don't want to do that... We still spent about $A6k after deducting these which seems to be the new normal. As a result we only saved $2.8k from regular income.

Spending was high this month. First, I had a bunch of business expenses for a trip early next year. Then I had to pay my employer a refund of half the price of an airline ticket for our trip to the Northern Hemisphere this past Northern summer. Otherwise, they decided retrospectively that they would have to pay fringe benefits tax and they don't want to do that... We still spent about $A6k after deducting these which seems to be the new normal. As a result we only saved $2.8k from regular income.

We lost money on investments - $28k - mainly due to the fall in the Australian Dollar of about 3 US cents. Rate of return for the month was -2.87% in USD terms or +0.83% in Australian Dollar terms. The MSCI gained 1.04%, the S&P500 3.05% (the unstoppable Energizer Bunny), and the ASX 200 lost 1.31% - the first two indices are in USD terms and the latter in AUD.

I made a major investment in managed futures as already mentioned in the blog. This month I will subscribe to the Platinum Capital rights issue for about $A7.5k. At the end of November our allocation of gross assets looked like this:

Of course, this isn't the same as the allocation of net worth due to leverage. Total leverage is about 34% i.e. 34 cents borrowed for each dollar of net worth. We retain that much cash while borrowing due to looking still to buy a house...

Of course, this isn't the same as the allocation of net worth due to leverage. Total leverage is about 34% i.e. 34 cents borrowed for each dollar of net worth. We retain that much cash while borrowing due to looking still to buy a house...

We lost money on investments - $28k - mainly due to the fall in the Australian Dollar of about 3 US cents. Rate of return for the month was -2.87% in USD terms or +0.83% in Australian Dollar terms. The MSCI gained 1.04%, the S&P500 3.05% (the unstoppable Energizer Bunny), and the ASX 200 lost 1.31% - the first two indices are in USD terms and the latter in AUD.

I made a major investment in managed futures as already mentioned in the blog. This month I will subscribe to the Platinum Capital rights issue for about $A7.5k. At the end of November our allocation of gross assets looked like this:

Sunday, December 01, 2013

Investments Update

Stock markets remained very strong globally, and particularly in the United States, this month, but not so much in Australia. The ASX 200 actually fell 1.31% while the SP 500 rose 3.05% both in local currency terms. The MSCI World Index was in between with a 1.46% increase in USD terms. Australian small caps were particularly weak. Our small cap investments lost 2.58% while our large cap Australian stocks bucked the trend and gained 0.82%.

A lot of our funds and stocks are hitting all time max profits for us

Colonial First State Geared Share Fund (Aus managed fund)

Unisuper (industry superannuation fund)

PSS(AP) (industry superannuation fund)

Colonial First State Diversified Fund (Aus managed fund)

CREF Global Equities (US retirement fund)

Colonial First State Geared Global Share Fund (Aus managed fund)

Generation Global Fund (Aus marketed managed fund from Generation)

Boulder Total Return Fund (BTF)

Colonial First State Diversified Fixed Interest Fund(Aus managed fund)

Macquarie Winton Global Alpha Fund

So diversifed and international funds and large cap Australian stocks are providing us with good long term returns. Australian small caps have been good but not in the past month.

Looking at my Mom's investments, finally we seem to have exceeded the pre-global financial crisis peak. Some funds though are worth less than what we paid for them and some more (we don't track the dividends from funds that pay out dividends so this isn't very accurate). What has done really badly are India and Brazil funds and commodities funds somewhat less badly. Hedge funds, large cap developed country stocks, diversified funds have done well in the long run.

A lot of our funds and stocks are hitting all time max profits for us

Colonial First State Geared Share Fund (Aus managed fund)

Unisuper (industry superannuation fund)

PSS(AP) (industry superannuation fund)

Colonial First State Diversified Fund (Aus managed fund)

CREF Global Equities (US retirement fund)

Colonial First State Geared Global Share Fund (Aus managed fund)

Generation Global Fund (Aus marketed managed fund from Generation)

Boulder Total Return Fund (BTF)

Colonial First State Diversified Fixed Interest Fund(Aus managed fund)

Macquarie Winton Global Alpha Fund

So diversifed and international funds and large cap Australian stocks are providing us with good long term returns. Australian small caps have been good but not in the past month.

Looking at my Mom's investments, finally we seem to have exceeded the pre-global financial crisis peak. Some funds though are worth less than what we paid for them and some more (we don't track the dividends from funds that pay out dividends so this isn't very accurate). What has done really badly are India and Brazil funds and commodities funds somewhat less badly. Hedge funds, large cap developed country stocks, diversified funds have done well in the long run.

Tuesday, November 26, 2013

Second Investment in Managed Futures

I have long seen the advantages of managed futures funds. The best of managed futures funds companies seems to be Winton. I previously made an investment with Man-AHL. The fund hasn't made much money for us, but did much better in the financial crisis than most of my other investments. We have 0.80% of net worth invested in the fund. We also have some investment in commodities via GTAA. Another fund that hasn't done much of anything so far. Now I have made an initial investment in a Winton fund offering. The investment is 4.6% of net worth. This takes exposure to commodities out of net worth to 6.0% and out of gross assets 4.5%. The main downside to this fund is that in Australia it doesn't have any tax advantages compared to stocks, which have strong advantages. This means that this will likely remain a small diversifying investment until maybe one day I set up a self-managed super fund, which is a tax advantaged structure itself.

How does this fit into our overall investment strategy? Basically we have a 60/40 portfolio with 60% in stocks and 40% in other investments. Within the stocks 2/3 are planned to be Australian stocks and 1/3 foreign. Within those categories we also allocate to large and small cap Australian and to US and non-US stocks in proportion to their market capitalizations. In the 40% other we have allocations to: bonds, real estate, hedge funds, commodities, private equity, cash, and other. The whole portfolio is then levered to provide about a beta of 1 to the stock market and rebalanced on an ongoing basis. The leverage of a diversified portfolio is an idea from the risk parity approach. 60/40 is simply the traditional stock-bond ratio used for diversified portfolios, and we weight heavily to Australian stocks for tax reasons. Several of the supposedly non-stock investments are in fact Australian listed stocks that are listed investment companies pursuing alternative investment strategies. A lot of the leverage is obtained by investing in leveraged (geared) managed stock funds rather than using margin loans ourselves. We keep the actual margin loan quite small most of the time. This is because the interest rate we can get is much worse than what the funds can get. Interactive Brokers has much better interest rates, but they aren't giving loans to Australian investors at the moment. All this seems to me a reasonable strategy for a non-high net worth investor based in Australia.

How does this fit into our overall investment strategy? Basically we have a 60/40 portfolio with 60% in stocks and 40% in other investments. Within the stocks 2/3 are planned to be Australian stocks and 1/3 foreign. Within those categories we also allocate to large and small cap Australian and to US and non-US stocks in proportion to their market capitalizations. In the 40% other we have allocations to: bonds, real estate, hedge funds, commodities, private equity, cash, and other. The whole portfolio is then levered to provide about a beta of 1 to the stock market and rebalanced on an ongoing basis. The leverage of a diversified portfolio is an idea from the risk parity approach. 60/40 is simply the traditional stock-bond ratio used for diversified portfolios, and we weight heavily to Australian stocks for tax reasons. Several of the supposedly non-stock investments are in fact Australian listed stocks that are listed investment companies pursuing alternative investment strategies. A lot of the leverage is obtained by investing in leveraged (geared) managed stock funds rather than using margin loans ourselves. We keep the actual margin loan quite small most of the time. This is because the interest rate we can get is much worse than what the funds can get. Interactive Brokers has much better interest rates, but they aren't giving loans to Australian investors at the moment. All this seems to me a reasonable strategy for a non-high net worth investor based in Australia.

Friday, November 01, 2013

Moominvalley October 2013 Report

Following hitting one million Australian dollars net worth last month, this month we reached a million US Dollars. $US1.008 million to be precise, up $US49k on last month. In Australian Dollars we reached $1.064 million, up $A38k on last month. The monthly accounts (in USD) follow:

Income was boosted a bit this month due to a gift of RMB 10k that Snork Maiden got when she visited China. She also spent a lot of that there and so we spent $5,846 for the month. We still saved almost $9k from regular income but our spending is gradually inching up and saving down as you would expect when our spending is still so low relative to income. Our annual spending level is around $80k per year. The following chart shows a moving average over the previous 12 months of spending for the year very roughly adjusted for inflation:

Income was boosted a bit this month due to a gift of RMB 10k that Snork Maiden got when she visited China. She also spent a lot of that there and so we spent $5,846 for the month. We still saved almost $9k from regular income but our spending is gradually inching up and saving down as you would expect when our spending is still so low relative to income. Our annual spending level is around $80k per year. The following chart shows a moving average over the previous 12 months of spending for the year very roughly adjusted for inflation:

The big peaks are mostly international moves (like in 2007), or in recent years big international trips, like our trip to 3 continents this year... Of course, after mid 2007 the data are for us as a couple and before that they are for just me, Moom, alone.

The big peaks are mostly international moves (like in 2007), or in recent years big international trips, like our trip to 3 continents this year... Of course, after mid 2007 the data are for us as a couple and before that they are for just me, Moom, alone.

Rate of return for the month was 3.92% in USD terms or 2.51% in Australian Dollar terms. The MSCI gained 4.04%, the S&P500 4.60%, and the ASX 200 3.97% - the first two indices are in USD terms and the latter in AUD.

I moved $US10k during the month from Australia to the US to pay off my margin loan with Interactive Brokers. I also did some switching out of large cap Australian stocks to diversified funds and global shares to rebalance as the Australian stock market was very strong and the Australian Dollar rose during the month too. I'm looking in the coming month to make a big (well less than 5% of net worth, but that is fifty thousand dollars) investment in managed futures. Having trouble with the application process, in the meantime.

Rate of return for the month was 3.92% in USD terms or 2.51% in Australian Dollar terms. The MSCI gained 4.04%, the S&P500 4.60%, and the ASX 200 3.97% - the first two indices are in USD terms and the latter in AUD.

I moved $US10k during the month from Australia to the US to pay off my margin loan with Interactive Brokers. I also did some switching out of large cap Australian stocks to diversified funds and global shares to rebalance as the Australian stock market was very strong and the Australian Dollar rose during the month too. I'm looking in the coming month to make a big (well less than 5% of net worth, but that is fifty thousand dollars) investment in managed futures. Having trouble with the application process, in the meantime.

Friday, October 18, 2013

And in US Dollars Too

As the Australian Dollar has risen strongly in the last few days, it has pushed us over the 1 million US Dollar mark, at least intra-month, too.

Saturday, October 12, 2013

Moom's Taxes 2012-13 Edition

My taxes are not so much changed from last year as things have settled down a lot now, compared to our first few years in Australia:

Salary (no employee super contributions so that is the actual salary) was up 12.3%. Interest up dramatically due to our house buying fund. Dividends and managed fund distributions up more modestly. Deductions were down on the whole. Tax payable up 19.4% due to lower deductions and the increase in Medicare surcharge etc. as a result after tax income didn't rise as much.

Salary (no employee super contributions so that is the actual salary) was up 12.3%. Interest up dramatically due to our house buying fund. Dividends and managed fund distributions up more modestly. Deductions were down on the whole. Tax payable up 19.4% due to lower deductions and the increase in Medicare surcharge etc. as a result after tax income didn't rise as much.

I expect to pay $1440 extra tax. I actually increased my CGT loss carry-forward this year, taking it from from $82k to $83k! That's a tax asset worth about $31k, which we don't include in our regular net worth spreadsheets.

I expect to pay $1440 extra tax. I actually increased my CGT loss carry-forward this year, taking it from from $82k to $83k! That's a tax asset worth about $31k, which we don't include in our regular net worth spreadsheets.

Snork Maiden's Taxes 2012-13 Edition

I've finally done our tax returns for this year. First, is Snork Maiden's taxes.

Blogpost on last year's taxes in order to compare with this year. In Australia there is no such thing as a joint tax return but increasingly married couples have to enter data in their tax return on their spouses finances as more things are being assessed on a household basis such as the Medicare Surcharge Tax. So, actually I need to do them at the same time. Anyway, here is a summary for Snork Maiden:

Her salary is actually higher than this. Employee superannuation (retirement) contributions are not counted in the taxable income - so-called "salary sacrifice". They amounted to about $A10k. Salary was up 11.5% on last year and taxable income including investments was up 12.5%. Distributions from managed funds and capital gains were up dramatically. I also compute a real income number before and after tax (up 15.2%) that puts back in some of the deductions which are purely imaginary. For example, long-term capital gains are taxed at half the rate of ordinary income but instead of using half the tax rate, half the capital gain is deducted from taxable income.

It looks like she owes about $500 extra tax this year.

Her salary is actually higher than this. Employee superannuation (retirement) contributions are not counted in the taxable income - so-called "salary sacrifice". They amounted to about $A10k. Salary was up 11.5% on last year and taxable income including investments was up 12.5%. Distributions from managed funds and capital gains were up dramatically. I also compute a real income number before and after tax (up 15.2%) that puts back in some of the deductions which are purely imaginary. For example, long-term capital gains are taxed at half the rate of ordinary income but instead of using half the tax rate, half the capital gain is deducted from taxable income.

It looks like she owes about $500 extra tax this year.

Update on Interactive Brokers

E-mail from IB this morning telling us Australian investors who have margin loans with them that we have to close out our margin loans by 11th November. This follows the previous e-mail saying that we couldn't open any new positions until we paid off the loan. So, I will be transferring money to the US to pay off the loan. I plan to use Ozforex for this. They do say that they hope to be able to offer margin loans to Australian customers again with 6 months.

Lots of Nice Head and Shoulders Patterns in the Markets

It looks like the US markets are expecting a US default or something despite the rise in stock prices over the last two days. Of course, if the crisis is really solved the market will likely go higher but if not, it will play out as a classic textbook technical analysis pattern. My favorite indicators are also pointing down:

Sunday, October 06, 2013

Investment Returns Since the Financial Crisis

Following up on yesterday's post comparing global, US, and Australian index rates of return and my own investment performance, today's post looks at the period after the low in the stockmarkets in March 2009. I also compare everything properly in both USD and AUD terms. First, in US Dollar terms:

Initially I tracked the ASX200 very closely coming out of the low but then gradually got pulled down by the lower performance of foreign shares. In the last year the ASX has underperformed foreign shares and that too seems to drag on our performance. Seem to be getting the worst of both worlds rather than the best! In AUD terms things look a bit different (just use the AUD/USD exchange rate to convert everything to AUD values):

Initially I tracked the ASX200 very closely coming out of the low but then gradually got pulled down by the lower performance of foreign shares. In the last year the ASX has underperformed foreign shares and that too seems to drag on our performance. Seem to be getting the worst of both worlds rather than the best! In AUD terms things look a bit different (just use the AUD/USD exchange rate to convert everything to AUD values):

Foreign shares performed poorly coming out of the financial crisis. Since mid 2011 they have outperformed Australian shares and as a result I've underperformed the foreign indices in that period.

Foreign shares performed poorly coming out of the financial crisis. Since mid 2011 they have outperformed Australian shares and as a result I've underperformed the foreign indices in that period.

Saturday, October 05, 2013

10 Year Rates of Return: ASX200 vs MSCI, SPX, and Moom

Another way of showing just how extraordinary the performance of the Australian stockmarket has been in the last couple of decades. I've posted this graph before, but now I've added the rate of return of the ASX200 index, which is the 200 largest stocks by capitalization on the Australian share market:

Returns are the average annual rate of return over the 10 years previous to the date marked. The ASX almost hit 15% per annum over ten years at one point! This maybe isn't a fair comparison as Moom, MSCI, and S&P500 are returns in US Dollars and the ASX200 is the return in Australian Dollars. ">Again you can see that I track the MSCI pretty closely.

Returns are the average annual rate of return over the 10 years previous to the date marked. The ASX almost hit 15% per annum over ten years at one point! This maybe isn't a fair comparison as Moom, MSCI, and S&P500 are returns in US Dollars and the ASX200 is the return in Australian Dollars. ">Again you can see that I track the MSCI pretty closely.

Thursday, October 03, 2013

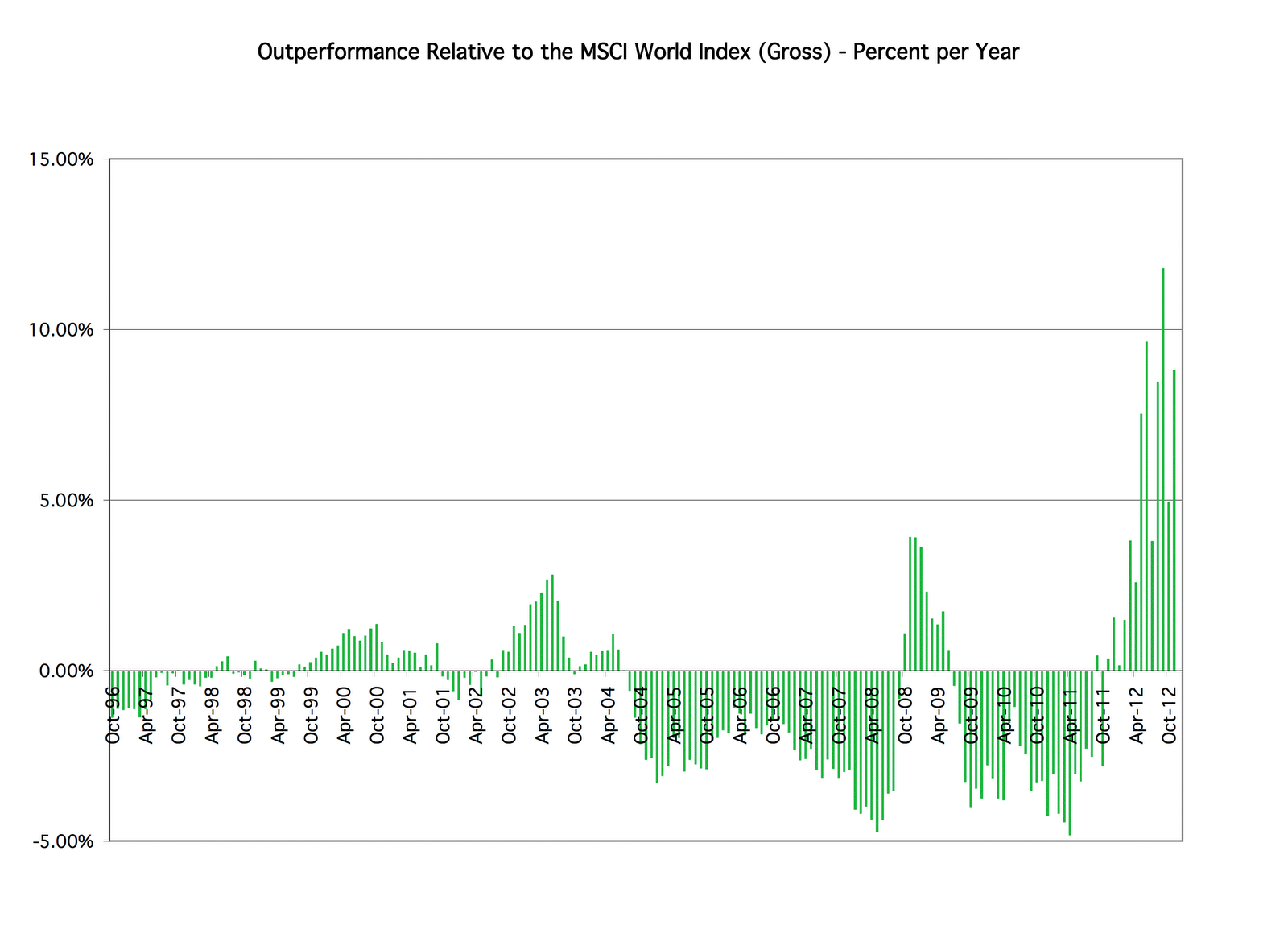

Investment Performance Against 4 Different Indices

BigChrisB sent me the ASX200 Accumulation Index data

he had collected and I have now measured my investment performance since 1996 (monthly data) against it and compared that to the other indices I've been tracking performance against:

The table shows that you get very different performance figures depending on which index you benchmark against. First the MSCI World Index in USD terms and using the US risk free rate to do the standard CAPM regression analysis. In other words, I measure my investment returns in US Dollars too. Estimated beta is 1.23 - a 1% change in the index is associated with a 1.23% change in my portfolio. Alpha is 0.44% which means I am beating the index on a risk adjusted basis. My monthly percentage rate of return is most correlated with the returns of this index. R-Squared is 0.74 which means that 74% of the variation in my rate of return is explained by the changes in the index. Results are quite different when I measure my rate of return and that of the index in Australian Dollars. The R-Squared is only 0.39, beta is much lower, and alpha is a little negative. Switching back to US Dollars my correlation with the S&P 500 is worse than with the MSCI but I underperformed the index by 1.6% per year, risk adjusted. Finally, in comparison to the Australian ASX 200 index and measuring things in Australian Dollars I underperformed by 3.89% a year, beta is 0.89 and R-Squared is 0.51. The ASX has been a fantastic performer over this period of time:

This explains why I benchmark against the MSCI in USD terms even though I live in Australia.

The table shows that you get very different performance figures depending on which index you benchmark against. First the MSCI World Index in USD terms and using the US risk free rate to do the standard CAPM regression analysis. In other words, I measure my investment returns in US Dollars too. Estimated beta is 1.23 - a 1% change in the index is associated with a 1.23% change in my portfolio. Alpha is 0.44% which means I am beating the index on a risk adjusted basis. My monthly percentage rate of return is most correlated with the returns of this index. R-Squared is 0.74 which means that 74% of the variation in my rate of return is explained by the changes in the index. Results are quite different when I measure my rate of return and that of the index in Australian Dollars. The R-Squared is only 0.39, beta is much lower, and alpha is a little negative. Switching back to US Dollars my correlation with the S&P 500 is worse than with the MSCI but I underperformed the index by 1.6% per year, risk adjusted. Finally, in comparison to the Australian ASX 200 index and measuring things in Australian Dollars I underperformed by 3.89% a year, beta is 0.89 and R-Squared is 0.51. The ASX has been a fantastic performer over this period of time:

This explains why I benchmark against the MSCI in USD terms even though I live in Australia.

Tuesday, October 01, 2013

Moomin Valley September 2013 Report

The main news this month was passing the one million Australian Dollar net worth mark. In other news, I spent two weeks this month in Northern Europe, but that hasn't had any impact on the figures after I deducted the refundable component to get "core expenditure", which was only $3,900. This month's accounts in US Dollars, as usual:

Current other income was a little higher than usual due to the refund I got for the European trip. I have the answer to last month's question as to why Snork Maiden's pay was a bit higher than expected. She got promoted one notch on the pay-scale but this happened after the regular union negotiated pay rise kicked in on 1 July though it was retroactive to 1 July.

The Australian Dollar rose this month to 93.41 US cents, which boosted investment returns in USD terms. As you can see from the table about 2/3 of USD investment returns were exchange rate gains.

I still have to file tax returns for both of us. I actually got a letter from the ATO telling me I was running out of time. I thought that was cheeky given the deadline is the end of this month.

Current other income was a little higher than usual due to the refund I got for the European trip. I have the answer to last month's question as to why Snork Maiden's pay was a bit higher than expected. She got promoted one notch on the pay-scale but this happened after the regular union negotiated pay rise kicked in on 1 July though it was retroactive to 1 July.

The Australian Dollar rose this month to 93.41 US cents, which boosted investment returns in USD terms. As you can see from the table about 2/3 of USD investment returns were exchange rate gains.

I still have to file tax returns for both of us. I actually got a letter from the ATO telling me I was running out of time. I thought that was cheeky given the deadline is the end of this month.

One Million Australian Dollars

We reached the long-awaited million Australian dollar net worth level. We aren't quite at a million US Dollars yet. It was back in 2007 when we first crossed a half million Australian Dollars mark for the first time and in 2008 we briefly touched half a million US Dollars. In between there was a global financial crisis, a marriage, and a move to Australia... well in reverse order... attempts to make a living as a trader, being unemployed, and then getting back onto the career track at a higher salary than before:

I actually thought yesterday when the Australian market was falling 85 points (1.6%) that we wouldn't remain above the line at the end of the month. Actually, the Geared Share Fund fell 3.3% on the day but was still up 5.5% on the month.

I actually thought yesterday when the Australian market was falling 85 points (1.6%) that we wouldn't remain above the line at the end of the month. Actually, the Geared Share Fund fell 3.3% on the day but was still up 5.5% on the month.

So the numbers come in at $A1.026 million or $US 958k. Rate of return for the month was 8.63% in USD terms or 3.5% in Australian Dollar terms. The MSCI gained 5.2% and the S&P500 3.14%. More accounting details to come.

So the numbers come in at $A1.026 million or $US 958k. Rate of return for the month was 8.63% in USD terms or 3.5% in Australian Dollar terms. The MSCI gained 5.2% and the S&P500 3.14%. More accounting details to come.

Sunday, September 29, 2013

Sources of Data on Stock Market Accumulation Indices

It's easy to get real time information on a wide range of stock market indices and historical data on a daily basis from sites like Yahoo Finance. But getting data on accumulation indices is much harder. Accumulation indices or in US terminology "total return indexes" include dividends in the index return. So they track how much your money would be worth if you could invest in the index and then reinvest all dividends without paying taxes or management fees. I have collected data on the MSCI All Country World Index and S&P500 total return index going back to 1996. My current sources for these indices are here and here.

The MSCI site allows you to select different pages of index returns using menus. I use the ACWI for the Developed and Developing Country, Gross returns, and Standard (midcap and large cap) options. Gross returns also include tax credits. I would include small caps, but that data wasn't available when I started following the series. You can select the data for any date you like.

At the S&P website you need to get the daily fact sheet on each index which includes price only and total return indices. The only way to get exact end of calendar month data is to collect it on the last day of each month. It seems that you now need to subscribe to get historical data. They used to provide a few months for free. You can get Australian indices here as well as the US ones I usually collect from here.

Bigchrisb recently linked to another source for the Australian ASX200 accumulation index - statistics provided by the Reserve Bank of Australia. You can get monthly data for a few recent years there.

The MSCI site allows you to select different pages of index returns using menus. I use the ACWI for the Developed and Developing Country, Gross returns, and Standard (midcap and large cap) options. Gross returns also include tax credits. I would include small caps, but that data wasn't available when I started following the series. You can select the data for any date you like.

At the S&P website you need to get the daily fact sheet on each index which includes price only and total return indices. The only way to get exact end of calendar month data is to collect it on the last day of each month. It seems that you now need to subscribe to get historical data. They used to provide a few months for free. You can get Australian indices here as well as the US ones I usually collect from here.

Bigchrisb recently linked to another source for the Australian ASX200 accumulation index - statistics provided by the Reserve Bank of Australia. You can get monthly data for a few recent years there.

Monday, September 02, 2013

Moominvalley August 2013 Report

We have been back home all this month and spending modestly by recent standards. This month's accounts in US Dollars, as usual:

Retirement contributions were higher than normal at $3,630 (AUD 4079) because Snork Maiden got an extra retirement contributions in after last month's three paychecks. Hmmm... I must be missing a contribution somewhere. But there is in fact little line between three paycheck months and three retirement contribution months as retirement contributions don't seem to be sent to the fund on as precise a timing as employees get their cash payment. Snork Maiden's pay was also a bit higher than expected. I haven't checked why.

The Australian Dollar fell a little more this month to exactly 89 US cents. Investment returns in US Dollar terms were 0.68% but in Australian Dollar terms they were 1.34%. For a change, we did much better than global markets due to our focus on Australia. The MSCI lost 2.04% (USD terms) and the S&P 500 2.90%.

Net worth rose in US Dollars by $17k to $873k. In Australian Dollar terms it rose by $A25k to $A981k. Unless there is a sharp fall in the markets we would clear 1 million Australian Dollars this month or next. But this time of year is often volatile :) September has been the second worst month since I started investing (May is worst), while October has been the best. That's surprising given its reputation for stock market crashes. In this timeframe (since 1996) the worst month for both the international indices I track has actually been August and the best April.

Retirement contributions were higher than normal at $3,630 (AUD 4079) because Snork Maiden got an extra retirement contributions in after last month's three paychecks. Hmmm... I must be missing a contribution somewhere. But there is in fact little line between three paycheck months and three retirement contribution months as retirement contributions don't seem to be sent to the fund on as precise a timing as employees get their cash payment. Snork Maiden's pay was also a bit higher than expected. I haven't checked why.

The Australian Dollar fell a little more this month to exactly 89 US cents. Investment returns in US Dollar terms were 0.68% but in Australian Dollar terms they were 1.34%. For a change, we did much better than global markets due to our focus on Australia. The MSCI lost 2.04% (USD terms) and the S&P 500 2.90%.

Net worth rose in US Dollars by $17k to $873k. In Australian Dollar terms it rose by $A25k to $A981k. Unless there is a sharp fall in the markets we would clear 1 million Australian Dollars this month or next. But this time of year is often volatile :) September has been the second worst month since I started investing (May is worst), while October has been the best. That's surprising given its reputation for stock market crashes. In this timeframe (since 1996) the worst month for both the international indices I track has actually been August and the best April.

Saturday, August 17, 2013

More International Investing Red Tape

It used to be that one advantage of being an Australia based investor was that you could invest in any investment product anywhere in the world and as long as you paid your taxes the government didn't mind. Of course, the taxes are relatively high compared to living in Hong Kong or Singapore but low compared to Western Europe. By contrast, US investors are heavily restricted unless they have a high net worth and become "accredited investors". But it seems the red tape is increasing (not surprising under a Labor government). I have had an account with Interactive Brokers since I lived in the US. This includes margin lending and I currently am borrowing money from them. Their interest rates are much lower than those you can get with retail brokers here in Australia. But, I just got a message from them that Australia modified the Corporations Act in 2010 so that margin lenders to Australian clients all need some licence. IB was told at the time that they didn't need to get the licence modification but now they do. Therefore, until they get the licence approved I won't be able to make any new investments on margin. Of course, I can close positions and I could add enough money to the account to pay off the loan and then continue to make new investments. No problem with trading futures as IB isn't lending money on futures trades. I haven't done any futures trades for several years. They gave us the option of closing our account at this point. Of course, I affirmed to keep my account open.

Thursday, August 15, 2013

Ten Years of Tax Credits

The chart shows our annual total of investment tax credits over the last ten years. These consist of credits attached to dividends for corporation tax paid by Australian companies known as "franking credits" and tax withheld on dividends in some countries. The US withholds tax on foreign investors, the UK does not. This doesn't include the atx credits in our superannuation (retirement) funds.

Because of investment expenses we end up with excess credits beyond the tax due on the dividends. We can use these to reduce our tax bill on a one to one basis. But with a $A60k joint annual tax bill we would need 20 times our current liquid assets to wipe out our tax bill. That's something like 10 million dollars. So this strategy is only making a somewhat marginal impact at the moment. Tax credits have not yet exceeded the pre-GFC high, despite liquid assets being 45% higher now. Liquid assets are all non-retirement investments before deducting debt.

Sunday, August 11, 2013

Vote Compass

The ABC have a website called Vote Compass that is meant to help in deciding who to vote for in our upcoming federal election here in Australia. I came out as a little socially liberal and right of centre economically and closest to the Liberal National Party. This wasn't a surprise at all. But it was still fun to do the survey. Snork Maiden was about as socially liberal as me but left of centre. Both of us are in the space between the Labor and Liberal parties.

I just saw that Enoughwealth has also done the survey. He came out as more socially conservative and right wing than the Liberal National Party.

Friday, August 02, 2013

Health Insurance, Part 2

So the consultant I met last week didn't send me any quotes... When I phoned the company she hadn't entered any of my details into their system either. So, I talked to a couple of consultants who were willing to give me actual quotes. The hospital cover plan we are looking at would cost $253.39 per month for the two of us including the lifetime health care cover and the 10% tax rebate and a $500 excess on hospital admission (only paid once per year per person if you need to go to hospital more than once). That's $3040 per year. My estimate of the Medicare surcharge is $3,100. So, it is about a breakeven in terms of upfront fees, as I expected. It turns out that my understanding of the lifetime health cover fee was wrong. If you don't join a private health scheme within a certain time of returning to Australia or immigrating and becoming eligible for Medicare then you pay the full loading. Your time out of Australia doesn't count. So our average loading would be about 20%.

I'm now thinking about the "extras" package, which covers stuff like dental and optical. The cheapest package adds $508 a year in costs, but none of their preferred optical providers are in our state and the benefits you can get on dental are also low outside of Victoria and South Australia which seems to be their major base. So, I don't think that extra package makes sense. Snork Maiden tends to use these services when she visits China.

This is our corporate health insurance deal. Probably, I should look at another quote before deciding on it.

P.S. 12:24pm

I just discovered this great government website that lets you compare alternative policies.

Thursday, August 01, 2013

Moominvalley July 2013 Report

Half of this month we spent travelling. Given that, spending is fairly modest. The Australian Dollar continued to fall, boosting returns in Australian Dollar terms and reducing them in US Dollar terms. This month's accounts in US Dollars, as usual:

Income was very high as this was a three pay month and we also got some refunds for the travel expenditure. The difference between "Expenditure" and "Core Expenditure" is due to business-related travel spending. Core expenditure gives a better idea of how much we are really spending while the total expenditure is needed to actually make the numbers add up. As a refresh, there are quite a few anomalies in the way I report our accounts. Other income, which is salary and other non-investment income (current income), as well as retirement contributions, is reported after tax and also include the proceeds to net tax refunds. Investment income (both current and retirement) is reported pre-tax including tax credits (Australian "franking credits" and foreign tax paid). We don't actually receive these credits - they reduce our tax bill at the end of the year - so I need to deduct them from the reported investment return to get the actual change in net worth each month. This is because net worth only reflects the actual money in our accounts at the end of each month. If we went to an accrual based system I could also add the value of my capital gains loss tax asset - worth $35k or so - but that would be a big complication for little or no gain. So, I stick with this system which works well for me. I only really care about what we get after tax and what we have now, but I want to see investment returns on a pre-tax basis to compare them with the market indices.

The Australian Dollar fell sharply this month resulting in investment returns in US Dollar terms of 2.33% but in Australian Dollar terms of 4.73%. This again lagged the market. The MSCI gained 4.82% (USD terms) and the S&P 500 5.09%.

Net worth rose in US Dollars by $34k to $861k. In Australian Dollar terms it rose by $A59k to $A961k. This has really been a stratospheric rise since mid 2011:

Income was very high as this was a three pay month and we also got some refunds for the travel expenditure. The difference between "Expenditure" and "Core Expenditure" is due to business-related travel spending. Core expenditure gives a better idea of how much we are really spending while the total expenditure is needed to actually make the numbers add up. As a refresh, there are quite a few anomalies in the way I report our accounts. Other income, which is salary and other non-investment income (current income), as well as retirement contributions, is reported after tax and also include the proceeds to net tax refunds. Investment income (both current and retirement) is reported pre-tax including tax credits (Australian "franking credits" and foreign tax paid). We don't actually receive these credits - they reduce our tax bill at the end of the year - so I need to deduct them from the reported investment return to get the actual change in net worth each month. This is because net worth only reflects the actual money in our accounts at the end of each month. If we went to an accrual based system I could also add the value of my capital gains loss tax asset - worth $35k or so - but that would be a big complication for little or no gain. So, I stick with this system which works well for me. I only really care about what we get after tax and what we have now, but I want to see investment returns on a pre-tax basis to compare them with the market indices.

The Australian Dollar fell sharply this month resulting in investment returns in US Dollar terms of 2.33% but in Australian Dollar terms of 4.73%. This again lagged the market. The MSCI gained 4.82% (USD terms) and the S&P 500 5.09%.

Net worth rose in US Dollars by $34k to $861k. In Australian Dollar terms it rose by $A59k to $A961k. This has really been a stratospheric rise since mid 2011:

Non-retirement profits in AUD terms also finally got above zero again. Profits on retirement accounts are well above the pre-GFC high:

Saturday, July 27, 2013

Health Insurance

So I met with the health insurance representative on Friday and she will send me quotes next week for various plans. With a basic plan we will save money compared to the Medicare surcharge. At our income level the Medicare surcharge is 1.25% of income which would be about $3,125 per year. The basic insurance package for our couple would be about $2,200 per year. But there are lots of "extras" you can add on. A complicated topic is the Lifetime Health Cover policy. This was introduced in 2000 by the Australian government and is meant to encourage people to take out private health insurance at a young age to avoid the adverse selection problem. It means that the cost of your insurance premium rises by 2 percentage points for each year you are over 30 years old after 2000.... For me this means that as I had my 30th birthday in 1994, the penalty only started accruing after 2000 (I think). But then I was in the US for many years. Those years don't count towards the penalty. So, I figure the penalty for me is 12%. For immigrants the penalty only starts to be incurred from after they become eligible for Medicare (and are older than 30). So for Snork Maiden I reckon her penalty is 6%. Therefore, our combined penalty is 9%. The government also offers a tax rebate for having private health insurance. At our income level this is 10%. So the penalty and the rebate should roughly cancel out and can be ignored when looking at the costs of the different policies.

Explanation for non-Australians - Australia has somewhat free public health care but their are tax incentives to get private health insurance. There is a surcharge which is 1-1.5% of your total income when your household income exceeds a certain level and you don't have insurance and there is a tax credit of 0-30% of the cost of health insurance, which is higher at lower income levels. There are also penalties for delaying getting health insurance after age 30 which are applied for the first ten years after you first buy private health insurance.

Explanation for non-Australians - Australia has somewhat free public health care but their are tax incentives to get private health insurance. There is a surcharge which is 1-1.5% of your total income when your household income exceeds a certain level and you don't have insurance and there is a tax credit of 0-30% of the cost of health insurance, which is higher at lower income levels. There are also penalties for delaying getting health insurance after age 30 which are applied for the first ten years after you first buy private health insurance.

Thursday, July 25, 2013

Excess Superannuation Contributions

I just saw this on the Colonial First State website:

"More generous rules for excess contributions:

In the past, if you went over your concessional contribution cap accidentally or otherwise, you’d be penalised effectively by having to pay the highest tax rate on the excess amount. But from

1 July 2013, you pay tax at your normal marginal tax rate on any excess concessional contributions, plus an interest charge. You'll also have the ability to withdraw up to 85% of any excess concessional contribution made. Note that this does not apply to contributions you have made in excess of the concessional cap before 1 July 2013."

I had heard there would be some change to the excess contributions regime but didn't know the details. But this is pretty unclear. Looking at the ATO website they don't have any clear information available yet on exactly how it would work. It looks like you can pay the extra tax at your own marginal rate and leave the money in the fund. The longer you wait to pay the excess tax, the more interest you will pay. But the ATO also says that "you will be liable for the excess concessional contributions charge." It doesn't say how much that will be - or perhaps that is the interest that the other articles I found mention.

I am stuck making excess contributions (more than $25k currently) because the universities' superannuation scheme has employers contributing 17% of your salary to the fund. And, no, you can't get them to reduce it or pay part of it as a "non-concessional contribution". At least the excess for me is less than $1000. In Snork Maiden's case I just realised that after the latest round of pay increases she will now be over the cap. We have been contributing $400 every two weeks as a "salary sacrifice" contribution on top of the employer contribution of 15.4%. We'll reduce this to $350.

"More generous rules for excess contributions:

In the past, if you went over your concessional contribution cap accidentally or otherwise, you’d be penalised effectively by having to pay the highest tax rate on the excess amount. But from

1 July 2013, you pay tax at your normal marginal tax rate on any excess concessional contributions, plus an interest charge. You'll also have the ability to withdraw up to 85% of any excess concessional contribution made. Note that this does not apply to contributions you have made in excess of the concessional cap before 1 July 2013."

I had heard there would be some change to the excess contributions regime but didn't know the details. But this is pretty unclear. Looking at the ATO website they don't have any clear information available yet on exactly how it would work. It looks like you can pay the extra tax at your own marginal rate and leave the money in the fund. The longer you wait to pay the excess tax, the more interest you will pay. But the ATO also says that "you will be liable for the excess concessional contributions charge." It doesn't say how much that will be - or perhaps that is the interest that the other articles I found mention.

I am stuck making excess contributions (more than $25k currently) because the universities' superannuation scheme has employers contributing 17% of your salary to the fund. And, no, you can't get them to reduce it or pay part of it as a "non-concessional contribution". At least the excess for me is less than $1000. In Snork Maiden's case I just realised that after the latest round of pay increases she will now be over the cap. We have been contributing $400 every two weeks as a "salary sacrifice" contribution on top of the employer contribution of 15.4%. We'll reduce this to $350.

Blog List

I finally upgrade Moomin Valley to a new Blogger template but in the process lost my previous blog list. A lot of the links were dead anyway. I've added a few back. If you would like your personal finance or investment blog added, let me know and if I like it, I'll add it. I'm more interested in the investing/business direction and less in frugality/getting out of debt.

Also, what's up with the NetWorthIQ badges? I re-added the code to the blog but nothing shows up :( If you know a hack, please let me know too.

Also, what's up with the NetWorthIQ badges? I re-added the code to the blog but nothing shows up :( If you know a hack, please let me know too.

Wednesday, July 24, 2013

Houses, Shares, Taxes Again

OK, so now we are not renting a house. We looked at four. Two were acceptable. But now Snork Maiden's mom says that she won't visit Australia till we buy a house and so we'll stay put for the moment. There aren't a lot of interesting houses on the market at the moment at this time of year.

I completed the four share purchases with shares in CAM.AX and IPE.AX.

Enoughwealth sent me a useable copy of the Australian tax form. It combines all three regular tax forms (the main form, the supplementary form, and the business items form) into one and unlike other Australian tax forms it isn't very colorful and instead of having separate boxes for each letter or number it has freeform entry boxes - compare to the sample individual tax return. But all the items and labels are exactly the same. It's weird, but I don't see why not to use it.

Monday, July 22, 2013

Houses, Shares, Taxes...

After looking at another couple of houses at the weekend and not agreeing on which we preferred we have changed direction and are now looking to rent a house or townhouse as a midway step to buying a house. Snork Maiden's mom is probably coming to visit for a while (months) and though we previously reorganized this apartment to accommodate her and her now deceased husband we aren't prepared to do that this time. We are much better off now and so have other alternatives. One option would be to rent her a furnished apartment nearby, but she's not keen on that... So we have four houses lined up to look at in the next three days. Rents range from $A570 to $A650 per week compared to $A490 in our current apartment. One ($A650) is actually nearer to the city centre, the others a little further out. One house is almost identical to another we looked at to buy a few doors down. Snork Maiden didn't like the small garden or lack of trees in the (new) neighborhood. But if we're not buying permanently...

I also just put in four orders to buy shares in listed funds here in Australia. Two have already executed (OCP.AX and AOD.AX). My margin loan was down to only $A15k. But if we are not likely to buy a house very soon then I don't need the extra borrowing capacity. We are still keeping a huge amount of cash on hand. You never know when the ideal property would show up. If we rent a house though it would be a 12 month lease. You can get out of that but it could be costly. With high occupancy rates still, it shouldn't be too hard to find someone else to rent in these locations.

The financial year here in Australia ends 30th of June so we are again in the run-up to filing tax returns (deadline 31 October). I've done a preliminary assessment and both of us probably owe more tax. For me it is over $1,000. This is going to mean that I will need to pay quarterly taxes in future :( The reason it is so high is that as we still don't have private health insurance I need to pay 1% of my income as the Medicare surcharge. On top of that my interest earnings are more than $3k due to our house-buying cash stockpile. On Friday I'm meeting a health insurance salesperson (sorry, consultant) who is offering a lower corporate health insurance rate. So, hopefully in future I can avoid the quarterly tax payments. It's also an incentive to increasing the margin loan again. I tried to do Snork Maiden's taxes using the ATO's E-Tax software now that they have a Mac version. It was a frustrating experience and I gave up. Crazily, you can't download a pdf of the main tax form! Only a sample copy. You have to get a hardcopy from the ATO in the mail or from their "shopfront". What I would really like is a web-based tax form that I can just fill numbers into without dealing with all the silly questions in E-Tax, or a typable pdf. I am going to get a hardcopy and again submit paper tax returns until they get the system more user friendly.

I also just put in four orders to buy shares in listed funds here in Australia. Two have already executed (OCP.AX and AOD.AX). My margin loan was down to only $A15k. But if we are not likely to buy a house very soon then I don't need the extra borrowing capacity. We are still keeping a huge amount of cash on hand. You never know when the ideal property would show up. If we rent a house though it would be a 12 month lease. You can get out of that but it could be costly. With high occupancy rates still, it shouldn't be too hard to find someone else to rent in these locations.

The financial year here in Australia ends 30th of June so we are again in the run-up to filing tax returns (deadline 31 October). I've done a preliminary assessment and both of us probably owe more tax. For me it is over $1,000. This is going to mean that I will need to pay quarterly taxes in future :( The reason it is so high is that as we still don't have private health insurance I need to pay 1% of my income as the Medicare surcharge. On top of that my interest earnings are more than $3k due to our house-buying cash stockpile. On Friday I'm meeting a health insurance salesperson (sorry, consultant) who is offering a lower corporate health insurance rate. So, hopefully in future I can avoid the quarterly tax payments. It's also an incentive to increasing the margin loan again. I tried to do Snork Maiden's taxes using the ATO's E-Tax software now that they have a Mac version. It was a frustrating experience and I gave up. Crazily, you can't download a pdf of the main tax form! Only a sample copy. You have to get a hardcopy from the ATO in the mail or from their "shopfront". What I would really like is a web-based tax form that I can just fill numbers into without dealing with all the silly questions in E-Tax, or a typable pdf. I am going to get a hardcopy and again submit paper tax returns until they get the system more user friendly.

Sunday, July 14, 2013

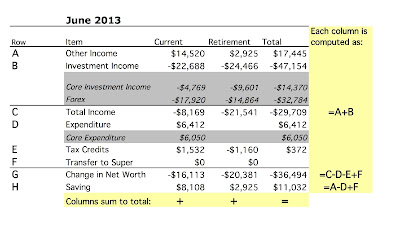

Moominvalley June 2013 Report

Finally back in Australia after another long trip to Europe, Asia, and Africa. This month's accounts in US Dollars, as usual:

Unlike last month we managed to save some money this month ($8,108 from current non-investment income) but still spent $6,412, which isn't too bad given all the travelling. There will probably be a similar level of spending in July too.

The Australian Dollar fell sharply this month resulting in investment returns in US Dollar terms of -5.46% but in Australian Dollar terms of -0.94%. As a result net worth fell $US36k but rose $3k in Australian Dollar terms to $A901k.

Unlike last month we managed to save some money this month ($8,108 from current non-investment income) but still spent $6,412, which isn't too bad given all the travelling. There will probably be a similar level of spending in July too.

The Australian Dollar fell sharply this month resulting in investment returns in US Dollar terms of -5.46% but in Australian Dollar terms of -0.94%. As a result net worth fell $US36k but rose $3k in Australian Dollar terms to $A901k.

Monday, June 03, 2013

Moominvalley May 2013 Report

Short report this month. I am travelling, currently in Charlottesville VA and about to go out to do some shopping.... Long trip from Australia via Canada yesterday... Here are the monthly accounts:

The Australian Dollar fell sharply resulting in steep losses in USD terms. US Dollar net worth is down $70k. This way underperformed the MSCI World Index. Australian Dollar net worth was flat as investment returns were -1.42% in currency neutral terms. The Australian Dollar is still overvalued of course (will report back from my shopping trip maybe on that)... We spent a record amount, actually dissaving a little bit this month. Most of the expenditure is on planned travel. $3,500 at least was reimbursed but still is recorded as expenditure. A big chunk though is associated private travel.

The Australian Dollar fell sharply resulting in steep losses in USD terms. US Dollar net worth is down $70k. This way underperformed the MSCI World Index. Australian Dollar net worth was flat as investment returns were -1.42% in currency neutral terms. The Australian Dollar is still overvalued of course (will report back from my shopping trip maybe on that)... We spent a record amount, actually dissaving a little bit this month. Most of the expenditure is on planned travel. $3,500 at least was reimbursed but still is recorded as expenditure. A big chunk though is associated private travel.

Wednesday, May 01, 2013

April 2013 Moominvalley Report

Yes, I haven't posted anything since last month's report, but I didn't post much on my professional blog either. It's been a busy time - teaching and everything else... Now starting to plan trips for June and July. I've booked a trip to Canada and the US. Will be in Ontario and Virginia in the first week of June. I'll be back in Australia for 10 days and then heading for Spain and Middle East/Africa. It will be my first trip to sub-Saharan Africa - I have been to Tunisia before - with two new countries to add to the visited list. I have a guidebook with a picture of giraffes on the cover right next to me as I am typing this.

Another up month... In USD terms it is the 11th up month. In AUD and currency neural terms we were down a little last month though. We yet again hit new net worth highs in both Australian and US Dollar terms of $A8889k (+$A31k) and $US923k (+$US28k).

Our rate of return was 1.97% in USD terms versus 2.92% for the MSCI and 1.93% for the S&P500. US stock markets were very strong and the Australian stock market relatively weak. In Australian Dollar terms we gained 2.52%. All asset classes gained apart from small cap Australian stocks (-2.62%). The best performing asset class was large cap Australian stocks (+3.32%). The monthly accounts (in US Dollars) look like this:

Non-investment income was a bit above normal and spending was the high side. Snork Maiden was traveling in North America. Total investment returns were $17k with USD returns suffering from the rising US Dollar. Saving in the table is saving from non-investment income.We saved almost $8k from our salaries not counting the retirement contributions of $4k. The latter were inflated, by a third payment this month from Snork Maiden's employer - all salary and other payments are paid every two weeks in Australia.

Another up month... In USD terms it is the 11th up month. In AUD and currency neural terms we were down a little last month though. We yet again hit new net worth highs in both Australian and US Dollar terms of $A8889k (+$A31k) and $US923k (+$US28k).

Our rate of return was 1.97% in USD terms versus 2.92% for the MSCI and 1.93% for the S&P500. US stock markets were very strong and the Australian stock market relatively weak. In Australian Dollar terms we gained 2.52%. All asset classes gained apart from small cap Australian stocks (-2.62%). The best performing asset class was large cap Australian stocks (+3.32%). The monthly accounts (in US Dollars) look like this:

Non-investment income was a bit above normal and spending was the high side. Snork Maiden was traveling in North America. Total investment returns were $17k with USD returns suffering from the rising US Dollar. Saving in the table is saving from non-investment income.We saved almost $8k from our salaries not counting the retirement contributions of $4k. The latter were inflated, by a third payment this month from Snork Maiden's employer - all salary and other payments are paid every two weeks in Australia.

Tuesday, April 02, 2013

Moominvalley March 2013 Report

Finally, we had a slightly down month in investment returns in Australian Dollar terms though the streak of gains extended to the 10th month in USD terms. We yet again hit new net worth highs in both Australian and US Dollar terms of $A858k (+$A9k) and $US895k (+$US25k). The Australian Dollar rose to $US 1.0426.

Our rate of return was 1.38% in USD terms versus 1.88% for the MSCI and 3.75% for the S&P500. US stock markets were very strong and the Australian stock market relatively weak. In Australian Dollar terms we lost 0.43%. Real estate was the best performing asset class and Australian small cap stocks the worst. The monthly accounts (in US Dollars) look like this:

Non-investment income was normal as was spending. We spent $A220 on a lawyer looking over the contract for the house that we didn't buy. Total investment returns were $12k with USD returns suffering from the rising US Dollar. Saving in the table is saving from non-investment income.We saved almost $10k from our salaries not counting the retirement contributions of $3k.

Our rate of return was 1.38% in USD terms versus 1.88% for the MSCI and 3.75% for the S&P500. US stock markets were very strong and the Australian stock market relatively weak. In Australian Dollar terms we lost 0.43%. Real estate was the best performing asset class and Australian small cap stocks the worst. The monthly accounts (in US Dollars) look like this:

Non-investment income was normal as was spending. We spent $A220 on a lawyer looking over the contract for the house that we didn't buy. Total investment returns were $12k with USD returns suffering from the rising US Dollar. Saving in the table is saving from non-investment income.We saved almost $10k from our salaries not counting the retirement contributions of $3k.

Monday, March 11, 2013

Money Burning a Hole in Your Pocket

Snork Maiden's stepfather died. He was 80 years old. Her mother is much younger. Snork Maiden has gone to China to be with her mother for a while. Her mother wants to visit Australia later this year, maybe starting in late October for a while and think about spending more time here in the future. She wants to transfer some money to our account here to help pay her expenses in Australia so that she can be more independent than when she and her husband visited last time. If we still are living in this apartment we could try to rent her a furnished unit somewhere nearby. We saw a couple of these last year when were looking for accommodation for a colleague (in the end they stayed on campus), but they weren't that near here.

But she wants to transfer the money today. One reason is so that Snork Maiden can help her with the transaction, which involves moving a "pile of cash" between two banks. Snork Maiden said as well that:

"She is in a hurry because she doesn't want to sit on a pile of money for long. She got a fixed-term pile of money that is ready to be harvested today, and she wants to decrease the number of transactions as much as possible. I suggested we could put the money in her saving account for the time being, but she said that was too complex and she has never had that much money sitting in her account. It was my stepfather who dealt with their money, so she has never touched so many cash before, and even the thought of having that much of money in her bank account somehow worries her. "

In the past I heard she would give money away to relatives rather than hold onto too much. It made me think of this story. A lot of people asked how it could be that a 68 year old full professor in a low cost of living location didn't have any savings. One answer is that some people just don't seem to be able to hold onto money for psychological reasons. Obviously, I don't have that problem. So, I'm going to look after her money for her.

But she wants to transfer the money today. One reason is so that Snork Maiden can help her with the transaction, which involves moving a "pile of cash" between two banks. Snork Maiden said as well that:

"She is in a hurry because she doesn't want to sit on a pile of money for long. She got a fixed-term pile of money that is ready to be harvested today, and she wants to decrease the number of transactions as much as possible. I suggested we could put the money in her saving account for the time being, but she said that was too complex and she has never had that much money sitting in her account. It was my stepfather who dealt with their money, so she has never touched so many cash before, and even the thought of having that much of money in her bank account somehow worries her. "

In the past I heard she would give money away to relatives rather than hold onto too much. It made me think of this story. A lot of people asked how it could be that a 68 year old full professor in a low cost of living location didn't have any savings. One answer is that some people just don't seem to be able to hold onto money for psychological reasons. Obviously, I don't have that problem. So, I'm going to look after her money for her.

Saturday, March 02, 2013

Auction

Our first auction where we were actually bidding. Some guy started the bidding at $700k and then it went up in increments of $25k. It stalled around $825k. Then I bid $830k. The next bid was $835k. But even $830k was above our predetermined limit. I only bid it because I knew the price was still below the reserve and if bidding really had dried up I wanted to be the top bidder to negotiate. But that seemed to unstick things and eventually the house sold for $877,500. Looks like the reserve was $875k. I was surprised that it actually sold at auction as the two previous houses that sold for $870k in that neighborhood would have standard valuations that would be higher. I guess the atmosphere on that block feels more like you are out in the bush and maybe that is what people wanted to pay for. It's what attracted us.

One of the agents would go around talking to bidders during the auction trying to get them to up their bids. When he asked me at around $875k I said: "That's the most we could possibly afford and it's way over the valuation we got, so no". He said: "They were wrong". I think it is highly likely that official land values for tax purposes will go up steeply in this neighborhood after these recent sales. But at the end of the auction, the agent shook my hand and said: "Congratulations". That was weird. Did he really think it wasn't worth $877.5k or did he know something else? A neighbor standing behind us then made some cryptic comments about the other neighbors. Snork Maiden thinks he was saying they were bad. I just couldn't understand what he was talking about.

Our attention now turns to a house in a neighborhood nearer us. It's land is valued $200k more than this one. It has a great view of the city and hills. The house is smaller and not in as good condition. Maybe a better chance to get a deal. There are lots of blocks in this value range that I really think are not worth paying for. This one maybe is.

A couple of colleagues came along to the auction. They hadn't been to a house auction before. One said: "These are like Santa Barbara prices". That's almost right.

One of the agents would go around talking to bidders during the auction trying to get them to up their bids. When he asked me at around $875k I said: "That's the most we could possibly afford and it's way over the valuation we got, so no". He said: "They were wrong". I think it is highly likely that official land values for tax purposes will go up steeply in this neighborhood after these recent sales. But at the end of the auction, the agent shook my hand and said: "Congratulations". That was weird. Did he really think it wasn't worth $877.5k or did he know something else? A neighbor standing behind us then made some cryptic comments about the other neighbors. Snork Maiden thinks he was saying they were bad. I just couldn't understand what he was talking about.

Our attention now turns to a house in a neighborhood nearer us. It's land is valued $200k more than this one. It has a great view of the city and hills. The house is smaller and not in as good condition. Maybe a better chance to get a deal. There are lots of blocks in this value range that I really think are not worth paying for. This one maybe is.

A couple of colleagues came along to the auction. They hadn't been to a house auction before. One said: "These are like Santa Barbara prices". That's almost right.

Friday, March 01, 2013

Moominvalley February 2013 Report

Yet another in 8 months of positive investment returns in Australian Dollar terms (9th in USD terms). We yet again hit new net worth highs in both Australian and US Dollar terms of $A848k (+$A40k) and $US869k (+26k). The US Dollar rose strongly, particularly against the Pound but also against the Euro and Australian Dollar. Many of our investments are at all time high profit levels. In US Dollar terms, total profits hit a new high of $US254k vs. $US250k in October 2007. So in nominal terms we have recovered from the financial crisis. In Australian Dollars though profits are at $A143k vs. $A209k at the peak in August 2007. So there is still some way to go.

Our rate of return was 2.43% in USD terms versus 0.03% for the MSCI and 1.36% for the S&P500. In Australian Dollar terms we made 4.31%. Almost all asset classes had positive returns with 5% plus gains in AUD terms in large cap Australian stocks and private equity. The monthly accounts (in US Dollars) look like this:

Non-investment income was normal while spending was high. We spent $A550 on getting the house valued. Car rego and a plane ticket to China added another $A2.5k or so. Total investment returns were $20k with USD returns suffering from the rising US Dollar. Saving in the table is saving from non-investment income.We still saved almost $5k from our current salaries in a high spending month like this.

Our rate of return was 2.43% in USD terms versus 0.03% for the MSCI and 1.36% for the S&P500. In Australian Dollar terms we made 4.31%. Almost all asset classes had positive returns with 5% plus gains in AUD terms in large cap Australian stocks and private equity. The monthly accounts (in US Dollars) look like this:

Non-investment income was normal while spending was high. We spent $A550 on getting the house valued. Car rego and a plane ticket to China added another $A2.5k or so. Total investment returns were $20k with USD returns suffering from the rising US Dollar. Saving in the table is saving from non-investment income.We still saved almost $5k from our current salaries in a high spending month like this.

Insurance

This afternoon I had the surreal experience of getting insurance on a house I don't own. We saw the lawyer this afternoon and she recommended that we get insurance already this afternoon rather than wait till Monday as we will still be liable to buy the house once we have a deposit down, even if it burns down or something between Saturday and Monday. This is called a "cover note". If we don't buy, we phone the insurer on Monday and cancel the policy. So we are all ready. The lawyer charged $220 for looking at the contract and going over things with us. No charge for looking at future contracts if we don't buy the house this time. Insurance for the house will be $966 per year.

Wednesday, February 27, 2013

Getting Ready

We are getting ready for the auction this weekend. If we end up buying we need to give the owner a cheque for 5% on the day. So I'm moving that money out of our savings account and into our checking account. There is a $20k a day limit on transfers which is kind of annoying. But I've now done two in a row and so am more or less at the 5%. Snork Maiden's job for today is phoning a lawyer and seeing if they need to see a copy of the contract before the auction. I'd much prefer to just be able to make an offer rather than this auction mechanism, but the best houses tend to go to auction here.

Wednesday, February 13, 2013

Things are Getting Serious

We went to see this house for the second time today. We took along a couple of friends/colleagues. One has some architecture background. They liked the house too. So, I just ordered an independent valuation. The standard way I value in houses here is to use the taxable value of the land and for a house in excellent condition $A2,000 per square metre. Using that this how comes in at $A775k. But houses seem to sell for more than that in this area. So, going into an auction I need a better sense of the fair price. Oh, yes, it's going to be auctioned in a few weeks time. I contacted the bank and they said I don't need to do anything else at the moment. The bank might accept the auction price or get their own valuation, it depends.

We went to see this house for the second time today. We took along a couple of friends/colleagues. One has some architecture background. They liked the house too. So, I just ordered an independent valuation. The standard way I value in houses here is to use the taxable value of the land and for a house in excellent condition $A2,000 per square metre. Using that this how comes in at $A775k. But houses seem to sell for more than that in this area. So, going into an auction I need a better sense of the fair price. Oh, yes, it's going to be auctioned in a few weeks time. I contacted the bank and they said I don't need to do anything else at the moment. The bank might accept the auction price or get their own valuation, it depends.

Friday, February 08, 2013

All Time Highs

The profits on a lot of our investments are currently at the maximum since we started investing in them. This is only remarkable because of the financial crisis and bear market we've been through in the last few years. Many of our investments have now fully recovered or more. They include:

CFS Developing Companies

CFS Future Leaders

Unisuper Superannuation Fund

CFS Diversified Fund

Clime Capital (CAM.AX)

PSSAP Superannuation Fund

TFS Market Neutral Fund (TFSMX)

CREF Global Equities Fund

IPE.AX (Aus private equity) BT Property Securities Fund

Aurora Sandringham Fund (AOD.AX)

Boulder Total Return (BTF)

CFS Geared Global Share Fund

Generation Global Shares

Celeste Small Australian Companies Fund

What isn't:

CFS Geared Share Fund

CFS Conservative Fund

CFS Global Resources Fund

Platinum Capital (PMC.AX)

TIAA Real Estate

Oceania Capital Partners (OCP.AX)

Cambria Global Tactical (GTAA)

Qantas (QAN.AX)

Man Eclipse 3 (Managed futures)

Bekaert

China Fund

3i (iii.l)

Legend International (lgdi)

Leucadia (LUK)

EAIT and EDIF (Funds of hedge funds)

Any pattern here? Australian and more generally small cap stocks and diversified portfolios are doing well. Larger cap stocks and non-Australian private equity resources/China themed stuff are not doing well.

CFS Developing Companies

CFS Future Leaders

Unisuper Superannuation Fund

CFS Diversified Fund

Clime Capital (CAM.AX)

PSSAP Superannuation Fund

TFS Market Neutral Fund (TFSMX)

CREF Global Equities Fund

IPE.AX (Aus private equity) BT Property Securities Fund

Aurora Sandringham Fund (AOD.AX)

Boulder Total Return (BTF)

CFS Geared Global Share Fund

Generation Global Shares

Celeste Small Australian Companies Fund

What isn't:

CFS Geared Share Fund

CFS Conservative Fund

CFS Global Resources Fund

Platinum Capital (PMC.AX)

TIAA Real Estate

Oceania Capital Partners (OCP.AX)

Cambria Global Tactical (GTAA)

Qantas (QAN.AX)

Man Eclipse 3 (Managed futures)

Bekaert

China Fund

3i (iii.l)

Legend International (lgdi)

Leucadia (LUK)

EAIT and EDIF (Funds of hedge funds)

Any pattern here? Australian and more generally small cap stocks and diversified portfolios are doing well. Larger cap stocks and non-Australian private equity resources/China themed stuff are not doing well.

Thursday, February 07, 2013

And Yet More Proposed Changes to Superannuation

Turns out the government has decided to abandon the idea of taxing distributions from larger superannuation accounts. The latest idea they are floating is taxing earnings of larger accounts. But the threshold would be much higher than $800k. This after destroying further the confidence of investors that superannuation payouts won't be taxed. And of course, this further complicates the system. Probably this won't happen because there is no chance I think that this government will be re-elected in September. Of course, none of these changes applies to the huge superannuation benefits that members of parliament receive. Those should definitely be abolished.

Wednesday, February 06, 2013

More Changes to Superannuation?