August was a mixed month. The MSCI World Index (USD gross) lost by 3.64% and the S&P 500 lost 4.08% in USD terms, but the ASX 200 gained 1.43% in AUD terms. All these are total returns including dividends. The Australian Dollar fell from USD 0.6968 to USD 0.6855 but it rose against the Pound from one Pound buying AUD 1.7430 to AUD 1.6958. We gained 0.25% in Australian Dollar terms but lost 1.38% in US Dollar terms. The target portfolio lost 0.71% in Australian Dollar terms and the HFRI hedge fund index rose 0.50% in US Dollar terms. So, we out-performed three benchmarks and under-performed two.

Here is a report on the performance of investments by asset class:

The asset class returns are in currency neutral returns as the rate of return on gross assets. I have added in the contributions of leverage and other costs and the Australian Dollar to the AUD net worth return.

Hedge funds were the biggest contributor to performance followed by futures, which had the strongest return. US stocks were the worst performer followed by gold and rest of the world stocks.

Things that worked well this month:

- Pershing Square Holdings was the best performer (AUD 11k) followed by Aspect Diversified Futures (10k) and Winton Global Alpha (8k).

What really didn't work:

- Australian Dollar Futures lost AUD 7k.

The investment performance statistics for the last five years are:

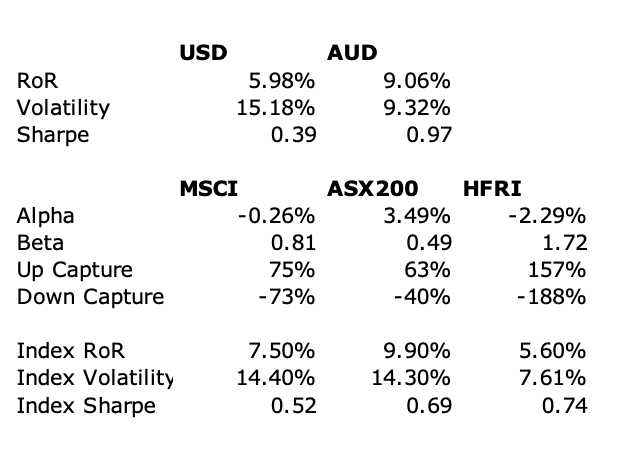

The first three rows are our unadjusted performance numbers in US and Australian dollar terms. The following four lines compare performance against each of the three indices over the last 60 months. The final three rows report the performance of the three indices themselves. We show the desired asymmetric capture and positive alpha against the ASX200 but not against the hedge fund index nor the MSCI. Compared to the ASX200, our rate of return has only been 0.6% lower, but our volatility has been 5% lower. We are performing 2% per annum worse than the average hedge fund levered 1.7 times.

We moved a bit away from our target allocation. Our actual allocation currently looks like this:

About 70% of our portfolio is in what are often considered to be alternative assets: real estate, art, hedge funds, private equity, gold, and futures. A lot of these are listed investments or investments with daily, monthly, or quarterly liquidity, so our portfolio is not as illiquid as you might think.

We receive employer contributions to superannuation every two weeks. We are now contributing USD 10k each quarter to Unpopular Ventures Rolling Fund and less frequently there will be capital calls from Aura Venture Fund II. In addition we made the following investment moves this month:

- I bought AUD 75k of units in the Aspect Diversified Futures Fund (Class A). This cash came from the redemption of Pershing Square Tontine Holdings.

- I sold AUD 25k of the First Choice Wholesale version of this fund and bought units of First Sentier Developing Companies instead.

- I switched about USD 17k from the TIAA Real Estate Fund to the TIAA Social Choice Fund (a balanced fund).

- I traded 10k shares of Regal Funds (RF1.AX) a couple of times.

- I invested USD 2.5k in a start-up offered by the Unpopular Ventures syndicate.

- I sold 12.5k shares of WAM Leaders (WLE.AX) to fund venture capital investments.

- I sold 3k shares of Ruffer Investment Company (RICA.L) for the same purpose.

- We received the payout from the sale of Lured.

No comments:

Post a Comment