Wednesday, January 16, 2019

Moomin Needs a Tax File Number

That's what the bank in Falafelland says... So, I will look today at applying for one for him. I think they should just give them out when you apply for a birth certificate. I don't know if the bank wants it because they just want a permanent ID for him or because it will affect the tax he pays as a foreign beneficiary of a local trust account. Up till now we have been using his passport number as an ID number. But passport numbers aren't permanent. You get assigned a new one every time you renew your passport, which is every 5 years for children.

Saturday, January 12, 2019

Portfolio Charts

Portfolio Charts is a really interesting website where you can do simulations of safe and permanent withdrawal rates and many other things for a range of investment portfolios. These include predefined portfolios and you can also build your own portfolio using a range of ETFs. Here for example is Tony Robbins' version of Ray Dalio's All Weather portfolio:

The orange line gives the withdrawal rate which means that you wouldn't have run out of money if you retired in any year since 1970 and retired for the length of time on the x-axis. The green line is the withdrawal rate that means that you will have at least as much money as you started with in real terms. It's interesting how these go in opposite directions as the length of retirement increases. If you retired for 30 years the permanent withdrawal rate is 3.8%. This portfolio had an average real return of 5.5%. The best performing portfolio in terms of withdrawal rates is the site creator's own "Golden Butterfly" which has 40% stocks, 40% bonds, and 20% gold:

This portfolio had a real return of 6.5%.

An interesting point is that safe and permanent withdrawal rates vary a lot by country. The site allows you to choose the US, UK, Canada, and Germany as home countries. The linked article also includes Australia, but unfortunately the site itself doesn't allow you to do analysis for Australia. A big caveat is, of course, that all this depends on historical returns. If bonds, for example, don't do as well going forward as they did from 1980 till recently then, withdrawal rates are going to be lower. Choice of alternative investments is also limited to gold, a commodities ETF, and a REIT ETF.

The orange line gives the withdrawal rate which means that you wouldn't have run out of money if you retired in any year since 1970 and retired for the length of time on the x-axis. The green line is the withdrawal rate that means that you will have at least as much money as you started with in real terms. It's interesting how these go in opposite directions as the length of retirement increases. If you retired for 30 years the permanent withdrawal rate is 3.8%. This portfolio had an average real return of 5.5%. The best performing portfolio in terms of withdrawal rates is the site creator's own "Golden Butterfly" which has 40% stocks, 40% bonds, and 20% gold:

This portfolio had a real return of 6.5%.

An interesting point is that safe and permanent withdrawal rates vary a lot by country. The site allows you to choose the US, UK, Canada, and Germany as home countries. The linked article also includes Australia, but unfortunately the site itself doesn't allow you to do analysis for Australia. A big caveat is, of course, that all this depends on historical returns. If bonds, for example, don't do as well going forward as they did from 1980 till recently then, withdrawal rates are going to be lower. Choice of alternative investments is also limited to gold, a commodities ETF, and a REIT ETF.

Annual Report 2018

Investment Returns

In Australian Dollar terms we gained 2.3% for the year while the MSCI gained 0.9% and the ASX200 lost 1.1% (all pre-tax including dividends). In USD terms we lost 7.7%, while the MSCI lost 8.9% and the S&P500 lost 4.4%. So we beat Australian and international markets but not the US market. In the longer term perspective, our returns and market returns were closely aligned this year:

Here are returns over various standard periods (not annualized):

We have done well compared to the ASX 200 over the last 5 years. Not as great over 10 years. In USD terms we have done well compared to the MSCI over the last three years and underperformed over longer time periods.

Investment Allocation

The main change in allocation over the year is the large increase in cash and real estate when we received the inheritance:

I also reduced my allocation to Australian large cap stocks around the same time, in early October. Earlier in the year, the allocation to cash falls as we increased trading and invested more in the Winton Global Alpha Fund (commodities) and subscribed to some IPOs. Private equity also increased with investment in Aura and IPE and then decreased with the takeover of IPE.

I also reduced my allocation to Australian large cap stocks around the same time, in early October. Earlier in the year, the allocation to cash falls as we increased trading and invested more in the Winton Global Alpha Fund (commodities) and subscribed to some IPOs. Private equity also increased with investment in Aura and IPE and then decreased with the takeover of IPE.

Accounts

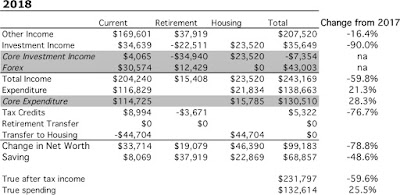

I stopped reporting monthly accounts this year, but I've still been computing them. Here are our annual accounts in Australian Dollars without including the inheritance:

We earned $170k after tax in salary, business related refunds, medical payment refunds, tax refunds etc. We earned (pre-tax including unrealised capital gains) $35k on non-retirement account investments. Both of those numbers were down strongly from last year. I stepped down from an admin role that paid extra salary and earned less in consulting etc. The investment numbers would have been worse without trading and the fall in the Australian Dollar ($31k in "forex" gain). Total current after tax income was $204k. Not including mortgage interest we spent $117k – Total actual spending including mortgage interest was $133k.

$9k of the current pre-tax investment income was tax credits – we don't actually get that money so we need to deduct it. Finally, we transferred $45k in mortgage payments (and virtual saved interest) to the housing account. The change in current net worth, was therefore $34k. Looking at just saving from non-investment income, we saved $8k. Both these numbers are down steeply from last year.

The retirement account is a bit simpler. We made $38k in contributions (after the 15% contribution tax) and the value fell by an estimated $23k in pre tax returns. $4k in "tax credits" is an adjustment needed to get from the number I calculate as a pre-tax return to the after tax number. Taxe on returns are just estimated because all we get to see is the after tax returns. I do this exercise to make retirement and non-retirement returns comparable. Net worth of retirement accounts increased by $19k.

Finally, the housing account. We spent $16k on mortgage interest. We would have paid $24k in mortgage interest if we didn't have an offset account. I estimate our house is worth $24k more than I did last year based on recent sales in our neighbourhood. After counting the transfer of $45k into the housing account housing equity increased $46k of which $23k was due to paying off principal on our mortgage.

Total net worth increased by $99k, $69k of which was saving from non-investment sources. Comparing 2018's accounts with 2017's, we saved 49% less and net worth increased by 79% less. Total after tax income was almost $230k, down 60% on last year. This number feels a lot more "reasonable" than last year.

Though our saving is down sharply on last year, we still saved in total 33% of our after tax non-investment income. Of course, this is less than last year's 50%. Including investment income our savings rate was 43%.

Here are the same accounts expressed in US Dollars:

How Does This Compare to My Projection for This Year?

At the beginning of the year, I projected a gain in net worth of $250k based on an 8% return on investments and a 6% increase in spending. As you can see, spending rose 25% and return on investments was only 2%. As a result net worth increased by only $99k.

Looking to 2019, I think we will be lucky if our investment return is 0%, as I am quite bearish about the world economy and stockmarket. If I pencil in a 6% rise in spending, then we would only increase net worth by $60k.

In Australian Dollar terms we gained 2.3% for the year while the MSCI gained 0.9% and the ASX200 lost 1.1% (all pre-tax including dividends). In USD terms we lost 7.7%, while the MSCI lost 8.9% and the S&P500 lost 4.4%. So we beat Australian and international markets but not the US market. In the longer term perspective, our returns and market returns were closely aligned this year:

Australian Dollar Returns

Here are returns over various standard periods (not annualized):

We have done well compared to the ASX 200 over the last 5 years. Not as great over 10 years. In USD terms we have done well compared to the MSCI over the last three years and underperformed over longer time periods.

Investment Allocation

The main change in allocation over the year is the large increase in cash and real estate when we received the inheritance:

Accounts

I stopped reporting monthly accounts this year, but I've still been computing them. Here are our annual accounts in Australian Dollars without including the inheritance:

Annual Accounts

There are lots of quirks in the way I compute the accounts, which have gradually evolved over time. Here is an explanation:

Current account is all

non-retirement accounts and housing account income and spending. Then

the other two are fairly self-explanatory. But housing spending only

includes mortgage interest. Property taxes etc. are included in the

current account. There is not a lot of logic to this except the

"transfer to housing" is measured using the transfer from our checking

account to our mortgage account. Current other income is reported after

tax, while investment income is reported pre-tax. Net tax on investment

income then gets subtracted from current income as our annual tax refund

or extra payment gets included there. Retirement investment income gets

reported pre-tax too while retirement contributions are after tax. For

retirement accounts, "tax credits" is the imputed tax on investment

earnings which is used to compute pre-tax earnings from the actual

received amounts. For non-retirement accounts, "tax credits" are actual franking credits

received on Australian dividends and the tax withheld on foreign

investment income. Both of these are included in the pre-tax earning but

are not actually received month to month as cash.... Finally, "core

expenditure" for housing is the actual mortgage interest we paid.

"Expenditure" adds back how much interest we saved by keeping money in

our offset account.

We include that saved interest in the current account as the earnings

of that pile of cash. That virtual earning needs to be spent somewhere

to balance the accounts... It is also included in the "transfer to

housing". Our actual mortgage payments were less than the number

reported by the $6k in saved interest. For current accounts "core

expenditure" takes out business expenses that will be refunded by our

employers and some one-off expenditures. This year, I think there are

none of those one-off expenditures. "Saving" is the difference

between "other income" net of transfers to other columns and spending in

that column, while "change in net worth" also includes the investment

income.

We earned $170k after tax in salary, business related refunds, medical payment refunds, tax refunds etc. We earned (pre-tax including unrealised capital gains) $35k on non-retirement account investments. Both of those numbers were down strongly from last year. I stepped down from an admin role that paid extra salary and earned less in consulting etc. The investment numbers would have been worse without trading and the fall in the Australian Dollar ($31k in "forex" gain). Total current after tax income was $204k. Not including mortgage interest we spent $117k – Total actual spending including mortgage interest was $133k.

$9k of the current pre-tax investment income was tax credits – we don't actually get that money so we need to deduct it. Finally, we transferred $45k in mortgage payments (and virtual saved interest) to the housing account. The change in current net worth, was therefore $34k. Looking at just saving from non-investment income, we saved $8k. Both these numbers are down steeply from last year.

The retirement account is a bit simpler. We made $38k in contributions (after the 15% contribution tax) and the value fell by an estimated $23k in pre tax returns. $4k in "tax credits" is an adjustment needed to get from the number I calculate as a pre-tax return to the after tax number. Taxe on returns are just estimated because all we get to see is the after tax returns. I do this exercise to make retirement and non-retirement returns comparable. Net worth of retirement accounts increased by $19k.

Finally, the housing account. We spent $16k on mortgage interest. We would have paid $24k in mortgage interest if we didn't have an offset account. I estimate our house is worth $24k more than I did last year based on recent sales in our neighbourhood. After counting the transfer of $45k into the housing account housing equity increased $46k of which $23k was due to paying off principal on our mortgage.

Total net worth increased by $99k, $69k of which was saving from non-investment sources. Comparing 2018's accounts with 2017's, we saved 49% less and net worth increased by 79% less. Total after tax income was almost $230k, down 60% on last year. This number feels a lot more "reasonable" than last year.

Though our saving is down sharply on last year, we still saved in total 33% of our after tax non-investment income. Of course, this is less than last year's 50%. Including investment income our savings rate was 43%.

Here are the same accounts expressed in US Dollars:

How Does This Compare to My Projection for This Year?

At the beginning of the year, I projected a gain in net worth of $250k based on an 8% return on investments and a 6% increase in spending. As you can see, spending rose 25% and return on investments was only 2%. As a result net worth increased by only $99k.

Looking to 2019, I think we will be lucky if our investment return is 0%, as I am quite bearish about the world economy and stockmarket. If I pencil in a 6% rise in spending, then we would only increase net worth by $60k.

New Investment: U.S. Treasury Bills

Interactive Brokers currently pays 1.7% interest on U.S. Dollars. But U.S. government bonds pay more than that and are supposedly risk free, so I thought I would give it a try. I am concerned that U.S. interest rates could still rise and so I don't want longer term bonds. So, I just bought a U.S. Treasury Bill expiring on 12 February. My idea is when that matures, I'll put part of the proceeds towards buying Australian Dollars. I plan to build a ladder of these and so force myself to buy Australian Dollars slowly.

At IB the commission for buying bonds is $5 and it turns out that the minimum trade size for treasuries is $100k. This isn't stated anywhere, but when I tried buying $50k last week, I got a message that my trade size was too small, whereas this trade went through. I'm gradually moving U.S. Dollars to my IB account - I can move up to $100k every 7 business days using the ACH method.

I've thought about municipal and corporate bonds too, but these can be illiquid. For example, for the nearest term Berkshire Hathaway bond, only $1000 is currently being offered.

At IB the commission for buying bonds is $5 and it turns out that the minimum trade size for treasuries is $100k. This isn't stated anywhere, but when I tried buying $50k last week, I got a message that my trade size was too small, whereas this trade went through. I'm gradually moving U.S. Dollars to my IB account - I can move up to $100k every 7 business days using the ACH method.

I've thought about municipal and corporate bonds too, but these can be illiquid. For example, for the nearest term Berkshire Hathaway bond, only $1000 is currently being offered.

Wednesday, January 09, 2019

Investment Policy for Trust Accounts

My brother is opening the trust accounts. They will be invested in local mutual funds. Unlike Australian or US managed or mutual funds these do not make distributions but like an Australian listed investment company (closed end fund) they pay tax on their earnings. The tax though is the relevant investment rate not the corporation tax. This is 25% of the inflation adjusted gain. Also, if you sell a mutual fund in Falafelland 25% capital gains tax is withheld. Looks like we can't really avoid this tax. Foreign tax paid is not refundable as cash in Australia – it can only be deducted against Australian tax liable.* Because my son's earnings would be way below the tax free threshold (initially each of these accounts will have about AUD 44k in them) he wouldn't need to pay tax if the investment funds were based in Australia.

My brother suggested investing 70% in bonds and 30% in stocks. As a long-term investment policy – we will be investing for the next 20 years for my son – I think this is too conservative.

This is both because in the long run stocks have performed better than bonds in most countries but also because interest rates are now low. This chart shows the real returns on US investments over the last century:

Since 1980, bonds did well as interest rates fell from historic highs. But in the 40 years up to 1980 bonds lost money in real terms as interest rates rose. So, I told him if we are adopting a "set and forget" investment policy then we should go for 60% stocks and 40% bonds. The mix between local and international investments should be 50/50. The local market is one of the cheaper ones globally.

Since 1980, bonds did well as interest rates fell from historic highs. But in the 40 years up to 1980 bonds lost money in real terms as interest rates rose. So, I told him if we are adopting a "set and forget" investment policy then we should go for 60% stocks and 40% bonds. The mix between local and international investments should be 50/50. The local market is one of the cheaper ones globally.

OTOH the local currency is quite strong currently. If we can revisit investment policy periodically then 70% bonds is OK for now. If there is a future larger decline in stock markets we would then switch to a more aggressive stance.

My brother's children are much older and so their trust accounts will exist for less time. If they intend to spend the money when they get it then I guess a more conservative stance might make sense. The youngest though will still need to wait 9 years to get her money so I think she can be more aggressive.

* Labor wants to make franking credits from Australian companies non-refundable as well. This would bring back symmetry in the way these credits are treated. Of course, I think we should go in the other direction and make foreign tax refundable :)

My brother suggested investing 70% in bonds and 30% in stocks. As a long-term investment policy – we will be investing for the next 20 years for my son – I think this is too conservative.

This is both because in the long run stocks have performed better than bonds in most countries but also because interest rates are now low. This chart shows the real returns on US investments over the last century:

OTOH the local currency is quite strong currently. If we can revisit investment policy periodically then 70% bonds is OK for now. If there is a future larger decline in stock markets we would then switch to a more aggressive stance.

My brother's children are much older and so their trust accounts will exist for less time. If they intend to spend the money when they get it then I guess a more conservative stance might make sense. The youngest though will still need to wait 9 years to get her money so I think she can be more aggressive.

* Labor wants to make franking credits from Australian companies non-refundable as well. This would bring back symmetry in the way these credits are treated. Of course, I think we should go in the other direction and make foreign tax refundable :)

Target Portfoilo Performance December 2018

In AUD terms the target portfolio lost 1.85% in December, gaining 0.3% for 2018 as a whole. The MSCI gained 0.9% for the year and I gained 2.3%. The graph shows the returns for the each month in 2018 for the target portfolio, the MSCI World Index in AUD terms, and the target portfolio:

The target has lower volatility but is more correlated to the MSCI than I was. So the target portfolio wouldn't have provided very useful diversification in 2018.

The target has lower volatility but is more correlated to the MSCI than I was. So the target portfolio wouldn't have provided very useful diversification in 2018.

Friday, January 04, 2019

Crowdfunded Real Estate

A relatively new investment concept is crowdfunding real estate investments. The idea is that an individual could directly invest small amounts in a range of properties or development opportunities thus reducing their risk. Rather than a fund manager picking the properties, investors could evaluate deals themselves.

I read about Fundrise on Financial Samurai. It seems to actually be closer to a traditional unlisted real estate managed fund, except there is more of a property development angle. They allow investments in both real estate debt and equity. They claim very high historical rates of return. I find it hard to understand how they could be so high. Equity investments could have leverage but debt investments must return the interest rate on the mortgage minus costs? I didn't feel that there was enough transparency around how returns are generated. In any case, unfortunately, it is not open to non-US investors.

So, I looked for crowdfunded real estate opportunities in Australia. This is what I found:

Crowdfundup – I only found one active project on the site.

Estatebaron – This website has more active deals. It focuses exclusively on property development. There seems to be very little information about each project and the site is much less polished.

Brickraise – The link seems to be dead.

Domacom – This is an ASX listed company. The company looked like they were heading to bankruptcy before a recent fundraising. The new money will only last just over half a year as their burn rate is AUD 5 million a year. They will need more than AUD 0.5 billion assets under management to break even given a 0.8% of NAV management fee. However, they have the largest number of deals on their site and have high quality information. Deals include a wide range of projects including solar farms and bioenergy as well as more conventional real estate. This is something I might consider when we have an SMSF up and running if it looks like the company will survive.

Based on this, real estate crowdfunding is not well developed in Australia. Do you know of other better websites?

Thursday, January 03, 2019

New Investment: PERLS XI

As a place to park Australian Dollars cash until I can move it out of Interactive Brokers, I bought some PERLS XI hybrid bank securities. These are Commonwealth Bank bonds that instead of paying interest pay franked dividends. The "grossed up" rate is 5.7% p.a. roughly. At some point the bonds should convert into Commonwealth Bank shares. However, the conversion rate isn't pre-determined. Instead, $100 of bonds will convert to $100 of shares at whatever the share price is at that time. I thought this was better than earning only 1.4% interest on my money, though there is a risk that the capital value will fall if interest rates rise in Australia. That doesn't look very likely at the moment to me. They are in theory less safe than bank deposits, but the risk of Commonwealth Bank getting into bad enough financial trouble in the next few months to reduce the value seems extremely low to me.

I think this is the first time I have ever bought bonds directly for my own account.

Insane Moves in Australian Dollar and Yen This Morning

Moves this big never happen in currencies. It's like one month's worth of moves in 5 minutes. Yen did the same thing in the other direction, other currencies not so much. No idea what sparked this. I managed to buy AUD24k...

This is being called a "flash crash".

Wednesday, January 02, 2019

December 2018 Report

You'll probably have heard that this was the worst December for US stocks since 1931. December is seasonally a positive month for stocks. Things weren't quite that bad in Australia and because the Australian Dollar fell, our returns for the month in AUD terms ended up being positive.

The Australian Dollar fell from USD 0.7302 to AUD 0.7049 The MSCI World Index fell 7.00% and the S&P 500 9.03%. The ASX 200 fell only 0.01%. All these are total returns including dividends. We gained 0.24% in Australian Dollar terms and lost 3.24% in US Dollar terms. So, we outperformed the Australian and international markets. This is not surprising given the weight of US Dollar cash in our portfolio. Our currency neutral rate of return was -1.74%.

Here again is a detailed report on the performance of all investments:

Things that worked quite well this month:

- US Dollars cash

- Gold

- Property, including:

- My jointly owned apartment with my brother. We got an offer for the apartment near the end of the month and I raised the carrying value in line with that.

- TIAA (direct US investments) and Pendal (REITS) real estate funds.

- On the other hand BlueSky lost a lot...

- Our direct share holdings in Medibank and Yellowbrickroad.

- Again, the PSS(AP) superannuation fund did relatively well (though losing) compared to Unisuper. But on the way up it gained just as much as Unisuper. It has both lower beta and higher alpha... At least based on the investment choices I have made within the fund.

What really didn't work:

- Cadence Capital, again fell sharply. It's performance in the last three months has been very bad. It's not surprising that they have cancelled their IPO of the Cadence Opportunities Fund. They received only AUD 8 million of subscriptions. It will still go ahead as an unlisted public company, whatever that is. Overall, we have lost money investing in Cadence.

- BlueSky fell back too. We still have made some money on this investment.

- 3i, China Fund, Pershing Square, and CFS Geared Global Shares all fell in line with global stock markets. The latter would have benefited from the fall in the Australian Dollar, which for an investment denominated in Australian Dollars is included in the return on that investment, but is separated out for the investments denominated in foreign currency...

We also invest AUD 2k monthly in a set of managed funds, and there are also retirement contributions. Then there are distributions from funds and dividends. Other moves this month:

- I bought 400 shares of the China Fund (CHN) early in the month. Not a good idea.

- I bought 25,000 shares of Bluesky Alternatives in the middle of the month (BAF.AX). Another bad idea.

- I bought 500 shares of Pershing Square Holdings (PSH.L) at the end of the month. So far, not a bad idea.

- I received cash from UBS in my US bank account and started moving it to Interactive Brokers and from there to our Australian bank account. After this first transfer, most of this money will go into buying a US Treasury Bills ladder in the short run. Today, I discovered that I have to keep the cash at IB for 2 months before I can move it to another bank account. So I am looking to buy some Australian bonds (probably bank hybrid securities) in the interim.

Tuesday, December 25, 2018

What's Your Forecast for the Stock Market?

My brother asked me what my forecast for the stock market was. Here is what I wrote to him:

"Well, I’ve been surprised how weak it has been recently, particularly in December, which you may have heard is so far the worst December in US stock markets since 1931. December is a seasonally strong month as is January. The US economy has been strong though house prices have been falling in many places, presumably due to the Fed raising interest rates and this seems to have been the main reason why the market is down. House prices have been falling in Sydney and Melbourne without any increase in interest rates here. Some indicators though show that the global economy could already be in recession, but I don’t know how reliable that is. The reason I was a bit surprised was it has been very predictable that before recessions the yield curve would invert (short term interest rates higher than long term). This hasn’t happened yet in the US. However, the Fed is signalling that they are going to raise interest rates by another 0.5% in 2019 which would reach an inversion probably. Stock markets tend to be leading indicators and so looks like this time it is more leading than usual. The US economic expansion is the 2nd longest in history and so presumably would come to an end some time soon (Australia hasn’t had a recession since the early 90s though…). Now we can say that the bull market ended as stocks have fallen 20%. If we look at the last two recessions and stock market crashes in the US, the stock market bottomed near the end or after the actual recession – in March 2003 and 2009. At that point the Fed will have slashed interest rates dramatically and unemployment will be high. OTOH in the 1990s the US market bottomed in October 1990, which was when the recession was only just getting underway. The Gulf War turned that around.

I did reduce my exposure to the stock market in early October, but not by enough. So, I’d probably use rallies in the market to reduce exposure more at this point. I was planning to use trading as a hedge, but I stopped trading soon after that as backtests weren’t good and I got ill and didn’t have time to work on it.

Of course, I could be completely wrong about all of this. In the last cycle I got out too early and got back in too early. Probably this time I’ll be late :)

I’m not planning on buying Australian Dollars in a hurry either, even though the current price is quite good. I’ll buy them gradually."

"Well, I’ve been surprised how weak it has been recently, particularly in December, which you may have heard is so far the worst December in US stock markets since 1931. December is a seasonally strong month as is January. The US economy has been strong though house prices have been falling in many places, presumably due to the Fed raising interest rates and this seems to have been the main reason why the market is down. House prices have been falling in Sydney and Melbourne without any increase in interest rates here. Some indicators though show that the global economy could already be in recession, but I don’t know how reliable that is. The reason I was a bit surprised was it has been very predictable that before recessions the yield curve would invert (short term interest rates higher than long term). This hasn’t happened yet in the US. However, the Fed is signalling that they are going to raise interest rates by another 0.5% in 2019 which would reach an inversion probably. Stock markets tend to be leading indicators and so looks like this time it is more leading than usual. The US economic expansion is the 2nd longest in history and so presumably would come to an end some time soon (Australia hasn’t had a recession since the early 90s though…). Now we can say that the bull market ended as stocks have fallen 20%. If we look at the last two recessions and stock market crashes in the US, the stock market bottomed near the end or after the actual recession – in March 2003 and 2009. At that point the Fed will have slashed interest rates dramatically and unemployment will be high. OTOH in the 1990s the US market bottomed in October 1990, which was when the recession was only just getting underway. The Gulf War turned that around.

I did reduce my exposure to the stock market in early October, but not by enough. So, I’d probably use rallies in the market to reduce exposure more at this point. I was planning to use trading as a hedge, but I stopped trading soon after that as backtests weren’t good and I got ill and didn’t have time to work on it.

Of course, I could be completely wrong about all of this. In the last cycle I got out too early and got back in too early. Probably this time I’ll be late :)

I’m not planning on buying Australian Dollars in a hurry either, even though the current price is quite good. I’ll buy them gradually."

Friday, December 21, 2018

No Interest on More Than $2 Million Deposit?

My brother and I have between us more than USD 2 million in cash in an account at UBS – most of the money we inherited – that we have been jumping through hoops to get out of there. In the meantime the bank seems to be paying no interest on the money and in the last two weeks it actually the account went down by USD 800 for no clear reason – online I can't find any info on fees the bank has charged. How is that possible?

Looks like we have everything in place now to close the account but have been told it'll take about 2 weeks still given the coming holidays etc. However, the client manager told my brother that she could transfer the majority of the money to us right away, while keeping some for unspecified fees and sending us the remainder not spent on fees later. My brother told her that he was happy to wait to get the money in one lump when they close the account. I was shocked and told him to accept her offer. It's hard for me to imagine that the extra fees for a second transfer could be more than the interest we could potentially earn on the money in two weeks (c. USD 2,000 if investing in US Treasury bills).

Update: We missed the client manager leaving for the Christmas break, so likely won't be till mid-January that we'll get the money out...

Another update: Actually, we now got about 90% of the money transferred to us. Why they need to hang on to a 1/4 million dollars, I don't know...

Looks like we have everything in place now to close the account but have been told it'll take about 2 weeks still given the coming holidays etc. However, the client manager told my brother that she could transfer the majority of the money to us right away, while keeping some for unspecified fees and sending us the remainder not spent on fees later. My brother told her that he was happy to wait to get the money in one lump when they close the account. I was shocked and told him to accept her offer. It's hard for me to imagine that the extra fees for a second transfer could be more than the interest we could potentially earn on the money in two weeks (c. USD 2,000 if investing in US Treasury bills).

Update: We missed the client manager leaving for the Christmas break, so likely won't be till mid-January that we'll get the money out...

Another update: Actually, we now got about 90% of the money transferred to us. Why they need to hang on to a 1/4 million dollars, I don't know...

Subscribe to:

Posts (Atom)