This month the financial crisis following the COVID-19 pandemic intensified. Up to around the 20th of the month there was chaos in financial markets. Many bonds fell as much or more than stocks and gold fell too as everything was liquidated. Then there began to be some stability with gold and many corporate bonds rallying again. I am now thinking that Australia might come out of this better than countries like the US and so betting a bit on Australian recovery makes sense. I am only doing that though in terms of moving towards our long-run allocation. Not over-allocating to Australian assets yet.

I expect HSBC are now happy they didn't give us a mortgage. It's not worth chasing them any more I think. We are keeping our children out of daycare and school, though technically they are still open. There was some miscommunication about applying for the subsidy and only this weekend I completed the application. Now the government announced today that childcare will be free to parents during the pandemic. I was thinking about cancelling the service, but if it is free, of course I won't. It's not 100% clear yet whether it will be free.

I think I will keep paying for my 4 year old's private preschool as we are considering the school as a long term schooling option (it goes through to year 10). Also, we are receiving a government subsidy. It's unclear yet whether this pre-school qualifies for the free childcare deal. We want to have a school for him when this crisis hopefully ends later this year. He goes to that school 2 days a week and 2.5 days to the public preschool.

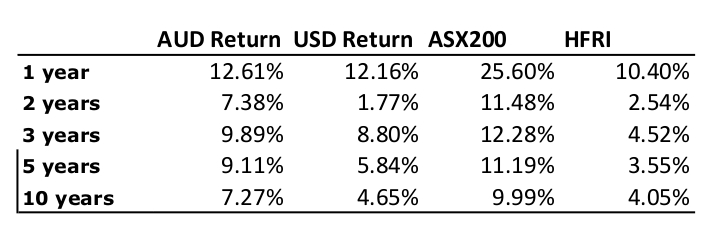

All stock markets fell sharply in response to the Coronavirus pandemic. The Australian Dollar fell from USD 0.6499 to USD 0.6115 and at one point reached USD 0.55. The MSCI World Index fell 13.44%, the S&P 500 12.35%, and the ASX 200 20.42%. All these are total returns including dividends. We lost 8.95% in Australian Dollar terms and 14.33% in US Dollar terms. This was the worst monthly investment return ever in terms of absolute Australian Dollars lost (AUD 319k). The target portfolio lost 5.05% in Australian Dollar terms and the HFRI hedge fund index is expected to lose 5.88% in US Dollar terms. So, we under-performed these benchmarks though did better than the ASX 200. The value of our house, which is not included in this investment return, increased. Well, the price of houses in our city went up. Updating the monthly AUD returns chart:

Here is a report on the performance of investments by asset class:

The returns reported here are in currency neutral terms. All asset classes lost money. Australian small cap stocks was the worst performer and gold the least bad. The biggest detractors from my overall return were bonds and hedge funds. These supposed diversifiers didn't work to mitigate losses in stocks. Hedge funds in general both lost from fund performance and from the fall in the price of listed closed end funds relative to their net asset value.

Things that worked well this month:

On a regular basis, we invest AUD 2k monthly in a set of managed funds, and there are also

retirement contributions. Other moves this month:

I expect HSBC are now happy they didn't give us a mortgage. It's not worth chasing them any more I think. We are keeping our children out of daycare and school, though technically they are still open. There was some miscommunication about applying for the subsidy and only this weekend I completed the application. Now the government announced today that childcare will be free to parents during the pandemic. I was thinking about cancelling the service, but if it is free, of course I won't. It's not 100% clear yet whether it will be free.

I think I will keep paying for my 4 year old's private preschool as we are considering the school as a long term schooling option (it goes through to year 10). Also, we are receiving a government subsidy. It's unclear yet whether this pre-school qualifies for the free childcare deal. We want to have a school for him when this crisis hopefully ends later this year. He goes to that school 2 days a week and 2.5 days to the public preschool.

All stock markets fell sharply in response to the Coronavirus pandemic. The Australian Dollar fell from USD 0.6499 to USD 0.6115 and at one point reached USD 0.55. The MSCI World Index fell 13.44%, the S&P 500 12.35%, and the ASX 200 20.42%. All these are total returns including dividends. We lost 8.95% in Australian Dollar terms and 14.33% in US Dollar terms. This was the worst monthly investment return ever in terms of absolute Australian Dollars lost (AUD 319k). The target portfolio lost 5.05% in Australian Dollar terms and the HFRI hedge fund index is expected to lose 5.88% in US Dollar terms. So, we under-performed these benchmarks though did better than the ASX 200. The value of our house, which is not included in this investment return, increased. Well, the price of houses in our city went up. Updating the monthly AUD returns chart:

Things that worked well this month:

- Pershing Square Holdings - this hedge fund did perform as intended, with the share price rising. The manager Bill Ackman made a big bet on credit default swaps that hedged the losses in the stock portfolio. Subsequently, he has closed those positions and bought more stocks. I bought more shares in PSH, which are trading around 65% of NAV.

- Treasury futures - my bet on a steepening yield curve worked and I closed half the position. The remaining position has backtracked since then.

- China Fund - I bought back our position, which has since performed well.

- Regal Funds - this was our worst performing investment this month in dollar terms. It lost 45% for the month.

- The Unisuper and PSS(AP) superannuation funds were the next biggest losers in dollar terms. They lost 13% and 9%, respectively, which is about what would be expected given a 20% fall in the Australian stock market.

- Junkier bonds like Virgin Australia. The value of Virgin Australia bonds halved. It's not our only distressed bond at this point, but just the worst. I don't know what I was thinking, buying this in the first place.

- Domacom (DCL.AX) shares fell by 2/3.

- Washington Gaslight and Lexmark bonds matured, releasing USD 60k plus interest. We didn't buy any new corporate bonds, so our exposure fell.

- We bought AUD 104k by selling US Dollars.

- I bought 25k Pengana Private Equity (PE1.AX) shares after the rights issue was cancelled. My timing could have been better as the shares then dipped before rebounding.

- I bought back our position in the China Fund (CHN). I figured that China is now rebounding. So far, that was good timing.

- I bought 25k Cadence Capital shares (CDM.AX). This fund has been a disaster, but the shares were trading at the value of cash that the fund has per share. So far, a good move.

- I bought 10k Tribeca Global Resources (TGF.AX) shares. Another disastrous investment in the long run, but the new shares have risen since buying them.

- I bought 25k Bluesky Alternatives shares (BAF.AX). They were trading at about 50% of NAV. I expect some of the fund's investments will be written down, but not that much overall.

- I shifted USD 4k from the TIAA Real Estate Fund to the CREF Social Choice Fund.

- I shifted about AUD 36k from the CFS Conservative Fund to the CFS Diversified Fund that has a higher risk allocation.