This month the whole family traveled to New Zealand for a week.This was baby Moomin's first international trip. He also started daycare two days a week. Moomintroll started going to free pre-school at the local public school 2.5 days a week and 2 days a week he is going to a private school where we can still get a childcare subsidy from the government.

It's been more than 3 months since we started trying to transfer our mortgage from Commonwealth Bank to HSBC. I went to the HSBC branch again, midmonth. The manager claimed that she had an incorrect email address for me and so I didn't get her message querying various things. They want to reduce the cash out component and the loan term length, both of which I was happy with.

I also tried to raise our Commonwealth Bank credit card credit limit from AUD 15k to AUD 20k. I was unsuccessful :( I always think it's strange that they don't consider assets or net worth in these applications.

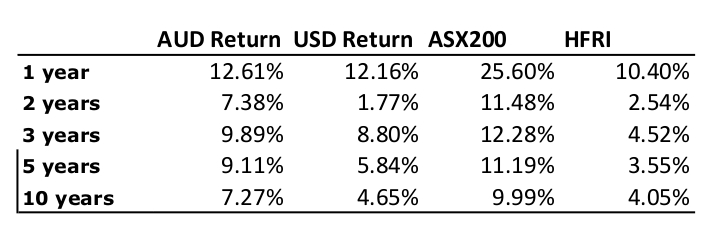

All stock markets fell sharply in response to the Coronavirus pandemic. The Australian Dollar fell from USD 0.6695 to USD 0.6499. The MSCI World Index fell 8.04%, the S&P 500 8.23%, and the ASX 200 7.46%. All these are total returns including dividends. We lost 3.8% in Australian Dollar terms and 6.61% in US Dollar terms. This was the worst monthly investment return ever in terms of absolute Australian Dollars lost (AUD 141k). The target portfolio lost 2.55% in Australian Dollar terms and the HFRI hedge fund index lost 1.67% in US Dollar terms. So, we under-performed these benchmarks though did better than equity indices. Updating the monthly AUD returns chart:

Here is a report on the performance of investments by asset class:

The returns reported here are in currency neutral terms.

The returns reported here are in currency neutral terms.

Things that worked well this month:

We moved a a bit away from our new long-run asset allocation. The shares of bonds, gold, and real estate rose and all others fell:

On a regular basis, we invest AUD 2k monthly in a set of managed funds, and there are also

retirement contributions. Other moves this month:

It's been more than 3 months since we started trying to transfer our mortgage from Commonwealth Bank to HSBC. I went to the HSBC branch again, midmonth. The manager claimed that she had an incorrect email address for me and so I didn't get her message querying various things. They want to reduce the cash out component and the loan term length, both of which I was happy with.

I also tried to raise our Commonwealth Bank credit card credit limit from AUD 15k to AUD 20k. I was unsuccessful :( I always think it's strange that they don't consider assets or net worth in these applications.

All stock markets fell sharply in response to the Coronavirus pandemic. The Australian Dollar fell from USD 0.6695 to USD 0.6499. The MSCI World Index fell 8.04%, the S&P 500 8.23%, and the ASX 200 7.46%. All these are total returns including dividends. We lost 3.8% in Australian Dollar terms and 6.61% in US Dollar terms. This was the worst monthly investment return ever in terms of absolute Australian Dollars lost (AUD 141k). The target portfolio lost 2.55% in Australian Dollar terms and the HFRI hedge fund index lost 1.67% in US Dollar terms. So, we under-performed these benchmarks though did better than equity indices. Updating the monthly AUD returns chart:

Things that worked well this month:

- Strangely, the China Fund was the best performer, gaining USD 4k. I sold it at the right time.

- The TIAA Real Estate Fund rose a tiny bit for the month. Apart from those other gainers were all bonds.

- Though it did lose money, the PSS(AP) superannuation fund was very resilient, only losing 2.1%.

- Junkier bonds like Virgin Australia and Tupperware and even Commonwealth Bank hybrids lost big time. Baby bonds generally did OK, though.

- Winton Global Alpha fund fell by 2.86%, providing little diversification benefit.

- Listed hedge funds were crushed, including Pershing Square (down 8.6% for the month), Platinum Capital (-23.3%), Regal (-11.4%), Tribeca Global Resources (-33%), and Cadence Capital (-20.5%). In most cases the stock price has fallen much more than the net asset value. This chart compares the actively managed ETF, PIXX.AX and the closed end fund PMC.AX, which are invested in similar portfolios:

We moved a a bit away from our new long-run asset allocation. The shares of bonds, gold, and real estate rose and all others fell:

- We sold USD20k of Tupperware bonds and USD50k of Energy Transfer bonds and bought USD25k of Medallion Financial (MFINL) and USD25k of General Finance (GFNSL) baby bonds (i.e. 1,000 shares of each) and USD50k of Ford and USD25k of Virgin Australia bonds. USD40k of Kinder Morgan bonds matured. So, our corporate bond holdings rose by USD15k. Selling Tupperware was a good move. Buying Virgin Australia was not.

- We also bought 500 more CBAPI.AX Commonwealth Bank hybrid securities (convertible bonds). It wasn't a good idea.

- We bought AUD 50k by selling US Dollars.

- We exercised our rights to buy 50,000 Pengana Private Equity (PE1.AX) shares in the rights issue. The actual transaction will come in March.

- I Sold 2,000 China Fund (CHN) shares after they recovered from the initial coronavirus scare. I expect there to be further implications of coronavirus, though of course I could be wrong.

- I bought another 2,000 IAU shares (a bit less than 20 ounces of gold).

- I bought a net 10,000 shares in Tribeca Global Resources Fund (TGF.AX) when the price seemed particularly depressed after one of the companies they lent money to entered US Chapter 11 bankruptcy. Also, one of the two main portfolio managers quit recently. This is now our worst investment ever in terms of dollars lost. We did a tax loss harvesting sale as part of this transaction, buying back shares in our other account. Different people, so not a "wash sale". I was too early.

- I bought 20,000 more shares of Cadence Capital (CDM.AX) another depressed LIC (listed hedge fund). Too early here too.

- I bought 20,000 shares of US Masters Residential Property Fund (URF.AX) - an even more beaten down closed end fund. We previously held this and sold at a small loss before the price really dived.

- I bought 4,957 shares of Platinum Capital (PMC.AX).