Our "rates" or property taxes are up 30% from last year! Presumably this is partly because of the shift in this state from stamp duty on buying a house (we paid $A 27,000 when we bought this house) to land taxes over time. Only the value of the land is taxed here in Australia, not the structure on it. For "townhouses" like ours - our house is actually a separate house - that are part of a body corporate (condo association) the land is valued as a share of the overall value of the land in the development. Our land share is only valued at $A168k, when a similar individual block in this suburb would be about $400k. So, this means our property tax is much lower than if we didn't live in a development like this. It's still $1,970 per year.

I just noticed that taxes on commercial property are outrageously high. The value in excess of $A600k is taxed at almost 5%. So you would pay about $A40k a year on land valued at $1 million.

Showing posts with label Tax. Show all posts

Showing posts with label Tax. Show all posts

Sunday, August 20, 2017

Saturday, October 08, 2016

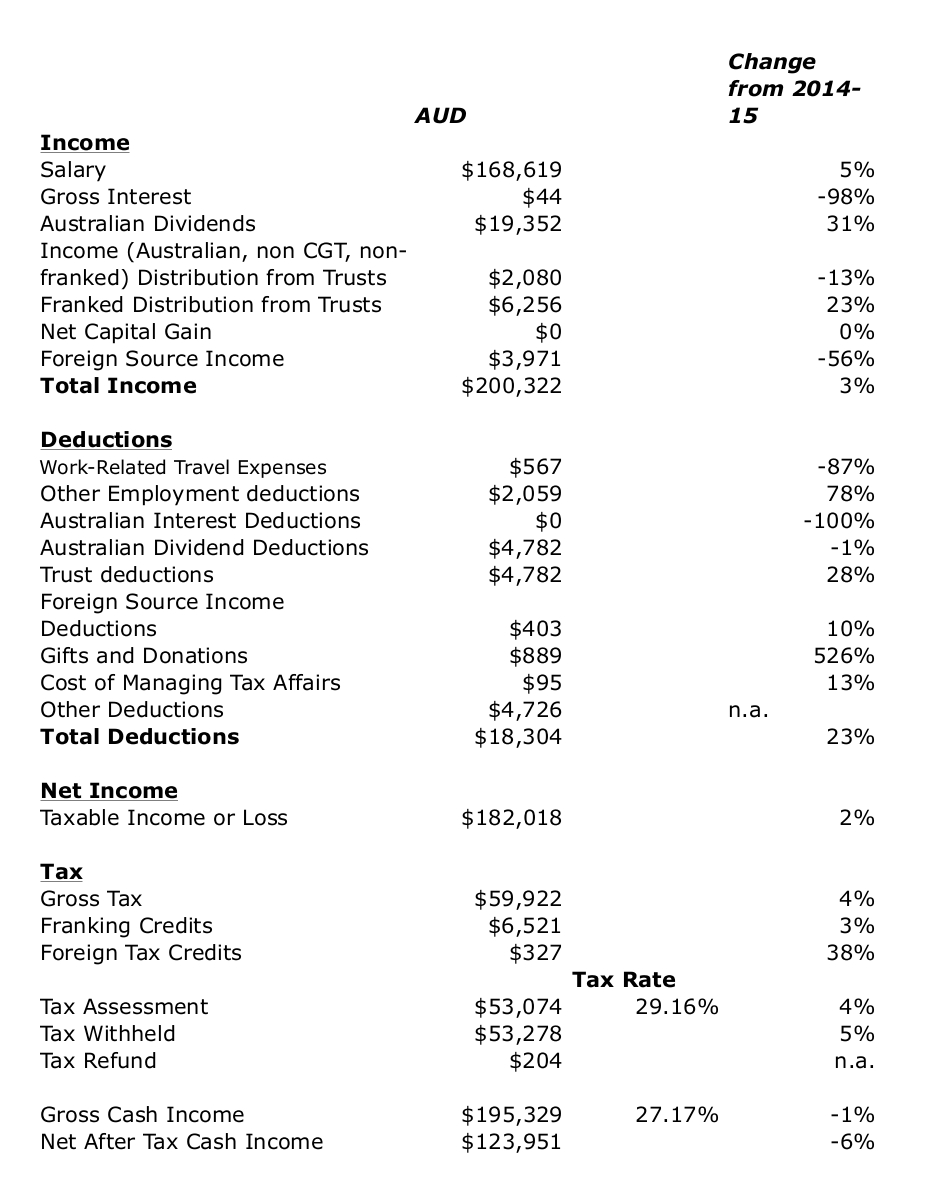

Moominmama's Taxes 2015-16 Edition

I've filed Moominmama's (formerly Snork Maiden) tax return for this tax year. The tax year runs from 1st July to 30th June in Australia. The figures ignore employer and employee contributions to

superannuation (retirement account) which amount to a lot of extra

income. Everything is in Australian Dollars of course.

Her salary is down because she went on maternity leave and the average tax rate also falls as a result. Investment income is up though.

Here are the reports on Snork Maiden's taxes for all previous years:

2014-15

2013-14

2012-13

2012-13

2011-12

2010-11

2009-10

2008-9

2007-8

Her salary is down because she went on maternity leave and the average tax rate also falls as a result. Investment income is up though.

Here are the reports on Snork Maiden's taxes for all previous years:

2014-15

2013-14

2012-13

2012-13

2011-12

2010-11

2009-10

2008-9

2007-8

Moominpapa's Taxes 2015-16 Edition

I have now completed my tax return. Looks like I should get a $204 refund. My taxable income is up by 2%. But my tax is up 4% despite a 23% increase in deductions and increases in tax credits. I'm a bit puzzled by that but I did move into the top tax bracket. Gross cash income is before tax income ignoring franking and other tax credits and adding in net undiscounted capital gains (not deleting losses from previous years).

This was the first year I checked what information the government knows about my tax affairs as revealed by the prefilled information on my tax return. They are missing a lot of information on my Australian accounts and none on my foreign holdings. Strangely they have dividends for some shares I have with a broker and don't have information on dividends from other companies that I hold through the same broker. Also they have one managed fund account but not the other I hold with the same firm. If I filed a return based on the numbers they know but taking the deductions I could document my return would look so radically different to last year that I think it would raise a lot red flags. But I didn't want to give the government any more information than they have, so I again filed a paper return. I filed Moominmama's return online for the first time, using the prefilled numbers plus deductions.

Previous years' reports:

2014-15

2013-14

2012-13

2011-12

2010-11

2009-10

2008-9

2007-8

P.S. 9 November

I got a more than $900 refund. Don't know what I got wrong in my calculations, but I'm not complaining :)

Thursday, August 04, 2016

July 2016 Report

This was a good month all round - both strong investment performance and moderate spending. Here are our monthly accounts (in AUD):

Spending (not counting mortgage) was low at $4.6k. No large and exceptional purchases this month. Salaries etc. added up to $10.4k. Snork Maiden is again earning money - this are payments at the minimum wage she is receiving from the government through her employer while on maternity leave. I think there about 3 months of those. We decided to receive those now in the new financial year to minimize her taxes by spreading her maternity pay over two financial years.

After taking into account the mortgage payment of $3.6k - there were three mortgage payments this month (and which includes implicit interest saving due to our offset account - the actual mortgage payment was about $420 less than this) - which shows up as a transfer to the housing account, we saved $2.2k on the current account. We made $3.1k of retirement contributions , and saved a net $1.6k in added housing equity. Net saving was, therefore, $6.9k across the board.

The Australian Dollar rose from USD 0.7433 to USD 0.7598. The ASX 200 rose 6.29%, the MSCI World Index 4.34%, and the S&P 500 rose 3.69%. We gained 5.27% in Australian Dollar terms and 7.61% in US Dollar terms. So we underperformed the Australian market and outperformed the international markets. The best performing investment (in total dollars not RoR) was, not surprisingly, the Colonial First State Geared Share Fund, which gained $34k. Unisuper and PSSAP gained $9k and $7k, respectively. There were lots of other strong performers. IPE,AX was the worst performer losing $750. All asset classes gained, with Australian Small Caps the best at 6.54%.

As a result of all this, net worth rose AUD 72k to $1.600 million or rose USD 80k to $US 1.216 million.

Colonial First State closed new applications to their retail First Choice Investments platform. This made me realise that the minimum investment for the wholesale version of this platform is now only $5,000. I had thought it would be $100k per fund or something like that. Management fees are lower for the wholesale platform. As a result it absolutely makes sense to move my CFS superannuation account to this platform. Probably, moving our managed (mutual) funds will result in capital gains tax bills. As I mentioned last month, I have a large carried over capital loss, of more than $60k. I estimate that moving all my managed funds will result in a capital gain of $50k. So, I would still have a capital loss carryover. Yes, this has an opportunity cost as it brings nearer the day that I would have to pay capital gains tax. The actual bill would be $12k. The value of funds is $222k. It would, therefore, take around 8 years to pay off in terms of lower management fees. But I figure that if I keep the funds "forever" it is worth it and if I sell at some point in the nearer future I will have to pay CGT anyway. Also, if Labor get into government next time, they are likely to raise the capital gains tax rate.

For Moominmama (formerly Snork Maiden), the number of years to pay off the tax hit is shorter and this year her tax rate (due to maternity leave) will be lower than other years. So, that's a no brainer.

Just need to find time to meet with someone at the bank and discuss all the details. Probably will wait a couple of months as workwise this is a crunch time in the next couple of months.

Monday, July 18, 2016

Investment Tax Credits

Revanche provides info on her progress in increasing dividend flow from stocks. I can't actually give you that exact information unless I ignored the dividend component of pay outs from managed (mutual) funds, because I haven't kept an exact record of that breakdown, as it isn't needed for tax purposes and doesn't help much for investment management purposes. What I do track is the tax credits associated with dividends. This is a particularly Australian phenomenon. Companies can pass on credit to shareholders for the Australian company tax they paid. These are called "imputation credits" or "franking credits". We can also claim a tax credit for foreign tax withheld on dividends etc. I call the total "investment tax credits". And this is what it has done since the 1997-98 tax year:

There was a big fall off during the Global Financial Crisis, but since then we have seen a steep rise. This year we reached just under AUD 9,000. These credits reduce our tax bill dollar for dollar. We are going to need to multiply this by nine though to wipe out our current tax bill :) It's at about AUD 79k before credits. The yield of tax credits is 1% of the liquid non-retirement assets we have. So, they'd have to reach AUD 8 million to eliminate our current tax bill. That's not going to happen, unfortunately.

Tuesday, July 12, 2016

Mid-year Forecast Update

At the beginning of the year I forecast that the best case scenario would see net worth rise to AUD 1.7 million or USD 1.2 million by the end of the year. At this point in the year the best case scenario is tracking at AUD 1.67 million and USD 1.25 million. This is because the Australian Dollar is looking more robust than it did and so I think the best case is that it ends the year at 75 US cents rather than 70. YTD we have only seen a 0.42% investment return (2.59% in USD terms), so we are tracking a bit below the most optimistic forecast from the beginning of the year.

I'm gradually putting together our tax returns as information comes in from fund managers etc. Moominmama should get a $2,700 or so refund at this point. I'm at around a few hundred dollars refund, which is likely to go negative as more info comes in.

I'm gradually putting together our tax returns as information comes in from fund managers etc. Moominmama should get a $2,700 or so refund at this point. I'm at around a few hundred dollars refund, which is likely to go negative as more info comes in.

Sunday, July 03, 2016

June 2016 Report

After hitting a new net worth high in Australian Dollar terms last month, net worth fell back a bit in this month's market turmoil. Here are our monthly accounts (in AUD):

Spending was very high at $12k but one of the two computers I bought was reimbursed by my employer, which is one reason why current other income (salary, refunds etc.) is also higher than in recent months. The other reason is that there were three biweekly salary payments this month. There was also an accident with a computer that required an expensive repair and Snork Maiden bought a treadmill. Minus the reimbursed expense, spending was $8.7k. Minus the other items I just mentioned it would have been $4.8k, which is in line with our typical spending.

After taking into account the mortgage payment of $5,188 - there were three mortgage payments this month (and which includes implicit interest saving due to our offset account - the actual mortgage payment was about $420 less than this) - which shows up as a transfer to the housing account, we dissaved $1.2k on the current account. We made $4.1k of retirement contributions (again three payments this month), and saved a net $3.0k in added housing equity. Net saving was, therefore, $5.8k across the board.

The Australian Dollar rose from USD 0.7241 to USD 0.7433. The ASX 200 fell 2.45%, the MSCI World Index 0.55%, and the S&P 500 rose 0.26%. We lost 3.30% in Australian Dollar terms and -0.74% in US Dollar terms. So we underperformed both Australian and international markets. The best performing investment (in total dollars not RoR) was Winton Global Alpha Fund with a gain of $2.5k. Not surprisingly, the worst performer was the Colonial First State Geared Share Fund, which lost $25k. All asset classes apart from commodities and real estate lost this month.

As a result of all this, net worth fell AUD 36k to $1.529 million but rose USD 3k to $US 1.136 million.

Two investments ended their life in the last couple of months. Legend International declared bankruptcy in May and the Everest Direct Investments Fund made its final distribution in June. The carrying value of each investment was less than $100 and so there isn't much impact on this month's accounts. But this means I can write off the losses on these investments in this year's taxes. The loss on Legend was almost USD 4,000. On EDIF about AUD 1,000. As I have a large carried over capital loss, of more than AUD 60k, the net effect will be to make the accumulated capital loss decline a little less. I think it still will be many years until I pay any capital gains tax.

Wednesday, May 04, 2016

April 2016 Report

Spending was a bit lower this month, financial markets had moderately positive performance, but our salary income has now gone down as Moominmama's maternity leave salary has now ended. In the new financial year she will get another 18 weeks of payments from the government at the minimum wage ($30k something per year). We asked for those to happen next financial year to reduce tax.

Here are our monthly accounts (in AUD):

Spending was $4.7k. The biggest single expenditure was the $639 quarterly body corporate (condo association) fee and after that health insurance of $340.

Moominmama actually got one last partial biweekly salary payment this month, so "current other income" came in at $10.3k and will fall further next month . After taking into account the mortgage payment of $3,567 (which includes implicit interest saving due to our offset account - the actual mortgage payment was about $400 less than this), which shows up as a transfer to the housing account, we saved $2.0k on the current account. We made $3.5k of retirement contributions, and saved a net $1.3k in added housing equity. Net saving was, therefore, $6.8k across the board.

The ASX 200 rose 3.37%, the MSCI World Index 1.54%, and the S&P 500 0.39%. The Australian Dollar fell from $US0.7676 to $US0.7616. We gained 1.96% in Australian Dollar terms and 1.09% in US Dollar terms. So we under-performed both Australian and international markets. The best performing investment (in total dollars not RoR) was again the Colonial First State Geared Share Fund, which gained $6.8k, followed by CFS Global Resources with $3.7k, and Unisuper with $3.5k.The worst performing investment was Cadence Capital, which lost $2.4k. All asset classes apart from hedge funds and commodities gained this month with U.S. stocks and then private equity being the best performers.

As a result of all this, net worth rose $29k including housing equity ($US13k) to $1.499 million ($US1.141 million).

Here are our monthly accounts (in AUD):

Spending was $4.7k. The biggest single expenditure was the $639 quarterly body corporate (condo association) fee and after that health insurance of $340.

Moominmama actually got one last partial biweekly salary payment this month, so "current other income" came in at $10.3k and will fall further next month . After taking into account the mortgage payment of $3,567 (which includes implicit interest saving due to our offset account - the actual mortgage payment was about $400 less than this), which shows up as a transfer to the housing account, we saved $2.0k on the current account. We made $3.5k of retirement contributions, and saved a net $1.3k in added housing equity. Net saving was, therefore, $6.8k across the board.

The ASX 200 rose 3.37%, the MSCI World Index 1.54%, and the S&P 500 0.39%. The Australian Dollar fell from $US0.7676 to $US0.7616. We gained 1.96% in Australian Dollar terms and 1.09% in US Dollar terms. So we under-performed both Australian and international markets. The best performing investment (in total dollars not RoR) was again the Colonial First State Geared Share Fund, which gained $6.8k, followed by CFS Global Resources with $3.7k, and Unisuper with $3.5k.The worst performing investment was Cadence Capital, which lost $2.4k. All asset classes apart from hedge funds and commodities gained this month with U.S. stocks and then private equity being the best performers.

As a result of all this, net worth rose $29k including housing equity ($US13k) to $1.499 million ($US1.141 million).

Thursday, April 21, 2016

Entering the Top Tax Bracket

Only 3% of Australian taxpayers are in the top tax bracket, which starts at $180,000 a year and has a marginal tax rate currently of 49%. And now I'm one of them, I think. IPE just declared a 5.75 cents a share dividend payable next month. I have 100,000 shares and so the dividend is $5,750. And it is a totally unfranked dividend. After this, I'm currently estimating my taxable income for the year at $182k and I'm now expecting to pay $3,000 extra tax at tax time. That also means I'm going to have to pay quarterly tax from now on.

I guess this is a good problem to have, but it feels kind of absurd that I'm now in the top tax bracket. Of course, when I first moved to Australia I wasn't that far from it because it kicked in at $50,000 a year in those days (1996) and my salary was a little higher than that. After "voluntary" super contributions of 7% and some deductions I was out of the zone.

Moominmama's reaction was that I should generate some business expenses to pull my income down. I could buy a nice big computer screen for home use, which I couldn't charge to my employer. It will be half price now I'm in the top tax bracket. I'm already almost maxing out my pre-tax super contributions. But spending money on stuff just to reduce tax is silly.

I guess this is a good problem to have, but it feels kind of absurd that I'm now in the top tax bracket. Of course, when I first moved to Australia I wasn't that far from it because it kicked in at $50,000 a year in those days (1996) and my salary was a little higher than that. After "voluntary" super contributions of 7% and some deductions I was out of the zone.

Moominmama's reaction was that I should generate some business expenses to pull my income down. I could buy a nice big computer screen for home use, which I couldn't charge to my employer. It will be half price now I'm in the top tax bracket. I'm already almost maxing out my pre-tax super contributions. But spending money on stuff just to reduce tax is silly.

Wednesday, April 20, 2016

Superannuation Reform Again?

Changes to superannuation are a perennial topic. If the government does this - lower the threshold for the 30% super contributions tax to $180k income per year and cut the concessional cap to $20k p.a. - I figure I will have to pay almost $7,000 a year more in tax. My taxable income this year looks like being just below $180k but the threshold for the super surcharge adds things like employer super contributions and investment losses to the taxable income amount. It would make most sense to cut the non-concessional cap, which is currently $180k per year, dramatically, as that is the way that wealthy people can get really large amounts of money into the super system, which will be taxed at a zero rate once they retire. But, of course, there is no immediate revenue to be gained by cutting the non-concessional cap. To simplify the system the government could just get rid of the concessional/non-concessional distinction, stop taxing earnings and then have a simple US Roth style system. Much too logical, of course. Actually, the optimal solution, assuming that super will be taxed in some way is to go for the US 401(k)/403(b) approach where there is no tax on contributions or earnings and regular tax on payouts. This gives the the money the best opportunity to increase in value... well under some economic assumptions anyway.

Saturday, December 05, 2015

Pre-Tax (Concessionary) Superannuation Contributions

After thinking about making after-tax retirement contributions, I thought today - Heh, I'm not even making the maximum pre-tax contributions. I've been making about $A28k a year in pre-tax contributions. Actually, that is supposedly my employer's contribution. In the university sector in Australia, employers contribute 17% on top of the nominal salary to superannuation for continuing (=permanent) employees, as opposed to the minimum government requirement of 9.5%. The maximum pre-tax contributions allowed for over 50's currently is $A35k per year ($A30k for under 50s). So, I just submitted the form to add $100 a week to my contributions. I didn't totally max things out to allow for a year or two of growth in salary before having to submit another form.

By the way, the standard agreement in the higher education sector includes another 8.5% pre-tax contribution from the employee's salary. I already opted out of that, because it would have been over the concessionary limit already when I started in 2011, when the concession limit was $A25k a year. Actually, I already had to withdraw an excess contribution to superannuation last year, which was a hassle, before the contribution limit was raised.

I'm still thinking about post-tax contributions. If I do it, I think I will start small at say $A1000 per month. That is small compared to the limit of $A15k per month :)

By the way, the standard agreement in the higher education sector includes another 8.5% pre-tax contribution from the employee's salary. I already opted out of that, because it would have been over the concessionary limit already when I started in 2011, when the concession limit was $A25k a year. Actually, I already had to withdraw an excess contribution to superannuation last year, which was a hassle, before the contribution limit was raised.

I'm still thinking about post-tax contributions. If I do it, I think I will start small at say $A1000 per month. That is small compared to the limit of $A15k per month :)

Tuesday, December 01, 2015

After Tax Super vs. Offset Account

At the moment, Australians can contribute up to $A180k per year to superannuation from after tax money on top of up to $A35k (if over 50) from pre-tax income. This seems like a crazy high limit and has no analogue in the US retirement system, for example. There is now a lot of talk about lifetime caps on super contributions. An easy way to do this would be to cut or eliminate this post-tax contribution limit. I had thought about making post-tax contributions starting in about 5 years time (when I would be about 55) and up to retirement. In the meantime, the plan was to build up our offset account and then pay down and redraw the mortgage. But now I am thinking that government might eliminate the post-tax option, I am wondering whether it would make sense to make these contributions sooner.

The gain from adding post-tax money to super is the tax-free earnings on the money after retiring. However, at least at the moment investment taxes are lower than regular income taxes and so we are talking about avoiding an 10% (after franking dividend tax in 38% bracket) to 23.5% (long-term capital gains tax in 45% bracket) tax starting 10 to 15 years in the future. Let's say the super investments make an 8% return, then the extra yield from avoiding tax by investing in super rather than non-super investments is about 1.3% per year. And this won't start to 10-15 years out and it is uncertain that the opportunity will go away and stop us doing that a few years later.

In the meantime the offset account is earning 4.55% tax free virtual interest with perfect certainty. A superannuation account would probably earn that after tax in the next 10-15 years, but there is a lot of uncertainty about that and the money is locked up for the next 9 years.

Is the answer to diversify and do some of both strategies?

The gain from adding post-tax money to super is the tax-free earnings on the money after retiring. However, at least at the moment investment taxes are lower than regular income taxes and so we are talking about avoiding an 10% (after franking dividend tax in 38% bracket) to 23.5% (long-term capital gains tax in 45% bracket) tax starting 10 to 15 years in the future. Let's say the super investments make an 8% return, then the extra yield from avoiding tax by investing in super rather than non-super investments is about 1.3% per year. And this won't start to 10-15 years out and it is uncertain that the opportunity will go away and stop us doing that a few years later.

In the meantime the offset account is earning 4.55% tax free virtual interest with perfect certainty. A superannuation account would probably earn that after tax in the next 10-15 years, but there is a lot of uncertainty about that and the money is locked up for the next 9 years.

Is the answer to diversify and do some of both strategies?

Tuesday, November 10, 2015

Moom's Taxes: Part 2

I only underestimated the amount of extra taxes that I owe by $5. I don't know why I also wasn't charged an extra amount of tax for private health insurance. That part of the tax return is complicated to understand. Maybe I filled out Snork Maiden's return incorrectly?

Friday, November 06, 2015

Snorkmaiden's taxes: Part 2

Back in July I computed Snork Maiden's taxes for the 2014-15 financial year. I estimated she owed $169 in extra tax. When I actually submitted her tax return more recently I had refined that to $147. But in fact the letter from the ATO today says she owes $292. Why? There is a $145 "Excess private health fund reduction or refund (rebate reduced) item" on the notice of assessment. I guess our family income turned out to be too high and we won't get as large a tax rebate on private health insurance?

Sunday, October 11, 2015

Moom's Taxes 2014-15 Edition

I have now completed my tax return. Looks like I need to pay $590 in extra tax. My salary is flat on last year but my taxable income is up by 5%. Gross cash income is before tax income ignoring franking and other tax credits and adding in net undiscounted capital gains (not deleting losses from previous years). Dividends, franking credits, and foreign source income are all up steeply, but so are most forms of deductions. As a result tax is only up 4%. But because tax withholding is only up 1% this year I owe tax, whereas last year I got a refund.

Previous years:

2013-14

2012-13

2011-12

2010-11

2009-10

2008-9

2007-8

Saturday, July 25, 2015

Snork Maiden's Taxes 2014-15 Edition

I've done the calculations for Snork Maiden's tax return for this tax year. The tax year runs from 1st July to 30th June in Australia. The figures ignore employer and employee contributions to

superannuation (retirement account) which amount to a lot of extra

income. Everything is in Australian Dollars of course.

Looks like she needs to pay extra tax :( Compared to last year the Medicare Levy has increased by 0.5%, which means an extra $450 of tax before anything else So, despite income being up only by 3% taxes are up by 5%. Salary is unchanged because the current Enterprise Agreement has expired and the union hasn't agreed a new deal with the employer. Investment income is up as are tax credits derived from investment income (by more than 50% in the latter case). Deductions are steeply down because there was no unreimbursed work related travel this year. Gifts and donations are up 1100%. Snork Maiden started donating $40 per month to Save the Children a month before the end of the last tax year.

The average tax rate on taxable income is 24.94%. Gross income before deductions and tax credits is not a lot higher than taxable income and so the tax rate on "gross cash income" is only slightly lower. The difference will be much bigger on my own income.

Here are the reports on Snork Maiden's taxes for all previous years:

2013-14

2012-13

2012-13

2011-12

2010-11

2009-10

2008-9

2007-8

Looks like she needs to pay extra tax :( Compared to last year the Medicare Levy has increased by 0.5%, which means an extra $450 of tax before anything else So, despite income being up only by 3% taxes are up by 5%. Salary is unchanged because the current Enterprise Agreement has expired and the union hasn't agreed a new deal with the employer. Investment income is up as are tax credits derived from investment income (by more than 50% in the latter case). Deductions are steeply down because there was no unreimbursed work related travel this year. Gifts and donations are up 1100%. Snork Maiden started donating $40 per month to Save the Children a month before the end of the last tax year.

The average tax rate on taxable income is 24.94%. Gross income before deductions and tax credits is not a lot higher than taxable income and so the tax rate on "gross cash income" is only slightly lower. The difference will be much bigger on my own income.

Here are the reports on Snork Maiden's taxes for all previous years:

2013-14

2012-13

2012-13

2011-12

2010-11

2009-10

2008-9

2007-8

Saturday, April 18, 2015

Redrawing Mortgage for Investment Purposes

Following up finally on comments that bigchrisb made about paying off the mortgage faster and then redrawing the money to investment in shares/refinance margin loans. This appears to be the ATO ruling on this. So, there is no problem to do this, but I have been thinking about the practicalities. It seems to me that if you pay off say $50k of the mortgage and then withdraw the money for investment, then the next $50k you pay off just repays the redraw and so your tax deductible loan gets no bigger. So, it only makes sense then to do the redraw after paying off as much of the mortgage as you want in the long term before doing the investment loan. So, in the meantime I think we will continue to accumulate money in the offset account, which gives more flexibility. If you are wondering why we should pile up cash while having a margin loan, actually the effective untaxed interest on the offset account is higher than the after tax rate on the margin loan. So, it makes sense to borrow more on the margin loan while piling money up in the offset. I think I will stop automatic re-investments of distributions and dividends where there is no discount for re-investment to speed the process a little. The only one I think is with my Colonial First State funds. When we are nearer an amount I think is reasonable then it would make sense to actually sell investments and add that money to the pile. But that should be a final step I think. I do have a lot of tax losses so that the first $60k of capital gains is tax free. This will be a project over several years. Of course, maybe in the end we would take the cash pile and use it as a downpayment on an investment property instead :) So, lots of things are possible.

P.S.

For U.S. readers who might wonder about why go through this complicated plan.... in Australia, mortgage interest is not tax deductible for owner occupiers. But investment interest is, even if it exceeds the income on the investment so that you make a net loss. The latter is known as "negative gearing".

P.P.S.

From March on, I'll include the implicit saved mortgage interest as part of investment return. That means that it also needs to be included in the "transfer from current account to housing" and included in housing expenses in the account in order to balance all the books. I'll also include the "core housing expenditure" in the accounts which will be the actual interest paid to the bank.

P.S.

For U.S. readers who might wonder about why go through this complicated plan.... in Australia, mortgage interest is not tax deductible for owner occupiers. But investment interest is, even if it exceeds the income on the investment so that you make a net loss. The latter is known as "negative gearing".

P.P.S.

From March on, I'll include the implicit saved mortgage interest as part of investment return. That means that it also needs to be included in the "transfer from current account to housing" and included in housing expenses in the account in order to balance all the books. I'll also include the "core housing expenditure" in the accounts which will be the actual interest paid to the bank.

Sunday, March 08, 2015

How Much Could We Save by Renting Our House out for a Year?

Bigchrisb commented on my recent post that we could save money by renting our new house out rather than going to live in it immediately. This is because the stamp duty paid to buy new properties is in this territory immediately tax deductible for investors. In Australia no costs of owner occupiers are tax deductible. So, I've calculated roughly what I think the financial gain from renting our house out for a year would be and come up with $18k:

The main deductions are the stamp duty, mortgage interest and depreciation. The first two we are going to pay ourselves anyway and so aren't actually additional costs while the latter is probably not a real cost, or we are going to suffer it anyway. Next there are property management fees, which might help in getting a tenant fast etc. and the difference between land tax on investors and rates on owner occupiers. There are real extra costs.

Assuming we could rent the house for one year at $650 a week we would earn $33800 in rent. So, the net income is -$34k and the tax saved at 40% is $13.5k. On the other hand we make $33.8k we would otherwise not have, but pay $25.8k in rent on our existing apartment that we would not have to pay if we lived in the new house as well as $3.7k in extra actual costs. So the net financial gain is $17.8k.

Let me know if you think I got something major wrong.

So, if we don't do this, economists would say that our revealed preference shows that the utility of living in our new house a year earlier and avoiding dealing with the hassles of being a landlord are worth at least $17.8k to us. For me, $17.8k is about 1.2% of net worth and so it's not enough to make a difference. It's not a lot more than our after tax salaries for one month. I asked Snork Maiden how big the number would have to be before she would be willing to do it and she said $50k. I know that if it was $100k I probably would do it :)

The main deductions are the stamp duty, mortgage interest and depreciation. The first two we are going to pay ourselves anyway and so aren't actually additional costs while the latter is probably not a real cost, or we are going to suffer it anyway. Next there are property management fees, which might help in getting a tenant fast etc. and the difference between land tax on investors and rates on owner occupiers. There are real extra costs.

Assuming we could rent the house for one year at $650 a week we would earn $33800 in rent. So, the net income is -$34k and the tax saved at 40% is $13.5k. On the other hand we make $33.8k we would otherwise not have, but pay $25.8k in rent on our existing apartment that we would not have to pay if we lived in the new house as well as $3.7k in extra actual costs. So the net financial gain is $17.8k.

Let me know if you think I got something major wrong.

So, if we don't do this, economists would say that our revealed preference shows that the utility of living in our new house a year earlier and avoiding dealing with the hassles of being a landlord are worth at least $17.8k to us. For me, $17.8k is about 1.2% of net worth and so it's not enough to make a difference. It's not a lot more than our after tax salaries for one month. I asked Snork Maiden how big the number would have to be before she would be willing to do it and she said $50k. I know that if it was $100k I probably would do it :)

Monday, March 02, 2015

Guardianship

My mother suffers from dementia. Up till recently my brother had power of attorney to make financial decisions for her, but financial providers now wanted him to have guardianship. So he is now the official guardian but the guardianship office where he and my mother live says that her investment portfolio is too risky. They want us to not have more than 20% in equities, get rid of all alternative investments and have the rest in cash and AAA bonds. It is not as if my brother and I decided on the current allocation. It's not a lot different to how it was when my mother could make her own decisions. The problem is that cash earns almost nothing anywhere and short term bonds less than inflation. Long-term bonds have the risk that their value will fall when one day central banks raise interest rates again.

We have tried to resist this and the guardianship office people met with my brother and his lawyer but the only concession they made was to give us a year to sort it out. In the meantime we also discovered (I read about this in an article in the New York Times) that the inheritance tax free threshold in the US for foreign estates was only $60k. That means that around 40% of the money in the US based separately managed accounts in my mother's name would be taxed away after she died - the accounts had minimal if any profit - so it would be taxing savings rather than earnings. So, we closed those accounts avoiding US inheritance tax and reducing the equity share of the portfolio to about 20%. Anyway, this is a warning to get good arrangements in place while you are still capable of making your own decisions rather than having a court imposed solution.

I need to think also about how to avoid US inheritance tax. I only have about $60k of direct US investments in stocks and mutual funds. But I also have another $70k in a 403b retirement account (TIAA-CREF). So, if I suddenly died there would be about $30k in inheritance tax that Snork Maiden would have to pay (no spouse allowance for foreigners...). There are various options including trying to roll my 403b into an Australian super fund now or setting up an Australian self-managed super fund (SMSF) and transferring the US individual investments into it. My thinking is that this would then be like having units in an Australia based managed fund. Would need to get proper advice on that first. Of course, it's not worth setting up an SMSF for just USD 60k in investments - that would be just one of the holdings of the SMSF. So, watch out if you have individual stocks in the US and aren't a US citizen.

We have tried to resist this and the guardianship office people met with my brother and his lawyer but the only concession they made was to give us a year to sort it out. In the meantime we also discovered (I read about this in an article in the New York Times) that the inheritance tax free threshold in the US for foreign estates was only $60k. That means that around 40% of the money in the US based separately managed accounts in my mother's name would be taxed away after she died - the accounts had minimal if any profit - so it would be taxing savings rather than earnings. So, we closed those accounts avoiding US inheritance tax and reducing the equity share of the portfolio to about 20%. Anyway, this is a warning to get good arrangements in place while you are still capable of making your own decisions rather than having a court imposed solution.

I need to think also about how to avoid US inheritance tax. I only have about $60k of direct US investments in stocks and mutual funds. But I also have another $70k in a 403b retirement account (TIAA-CREF). So, if I suddenly died there would be about $30k in inheritance tax that Snork Maiden would have to pay (no spouse allowance for foreigners...). There are various options including trying to roll my 403b into an Australian super fund now or setting up an Australian self-managed super fund (SMSF) and transferring the US individual investments into it. My thinking is that this would then be like having units in an Australia based managed fund. Would need to get proper advice on that first. Of course, it's not worth setting up an SMSF for just USD 60k in investments - that would be just one of the holdings of the SMSF. So, watch out if you have individual stocks in the US and aren't a US citizen.

Monday, December 08, 2014

Murray Report on the Australian Financial System and Superannuation

The findings of the Murray review of the Australian financial system have been released. I am most interested in their recommendations for superannuation (retirement accounts). Of course, there is no way to know yet what recommendations the government (or future governments) will take on board. This just adds to the uncertainty surrounding super. I had been thinking that now I am 50 years old, as soon as we buy a house I would start making after tax ("nonconcessionary") contributions to super. This is because once you retire there is no tax on superannuation earnings and it is only 10 years till I am 60 and could withdraw money. Though pre-tax contributions ("concessionary" - actually they are taxed at 15% instead of your marginal rate) are limited to $35k per year, you can contribute up to $150k per year after tax. But if they actually withdraw the advantageous tax status of super and worse still if they end up forcing people to take an annuity instead of being able to access their money as they like then I wouldn't want to put any extra money in super at all. The review recommends making annuities a default option, which people will have to opt out of, but I can imagine it becoming compulsory. So, for now, even when we have bought a house I wouldn't plan on adding any extra non-concessionary contributions to super.

And yes I sold Qantas too soon :(

Subscribe to:

Posts (Atom)