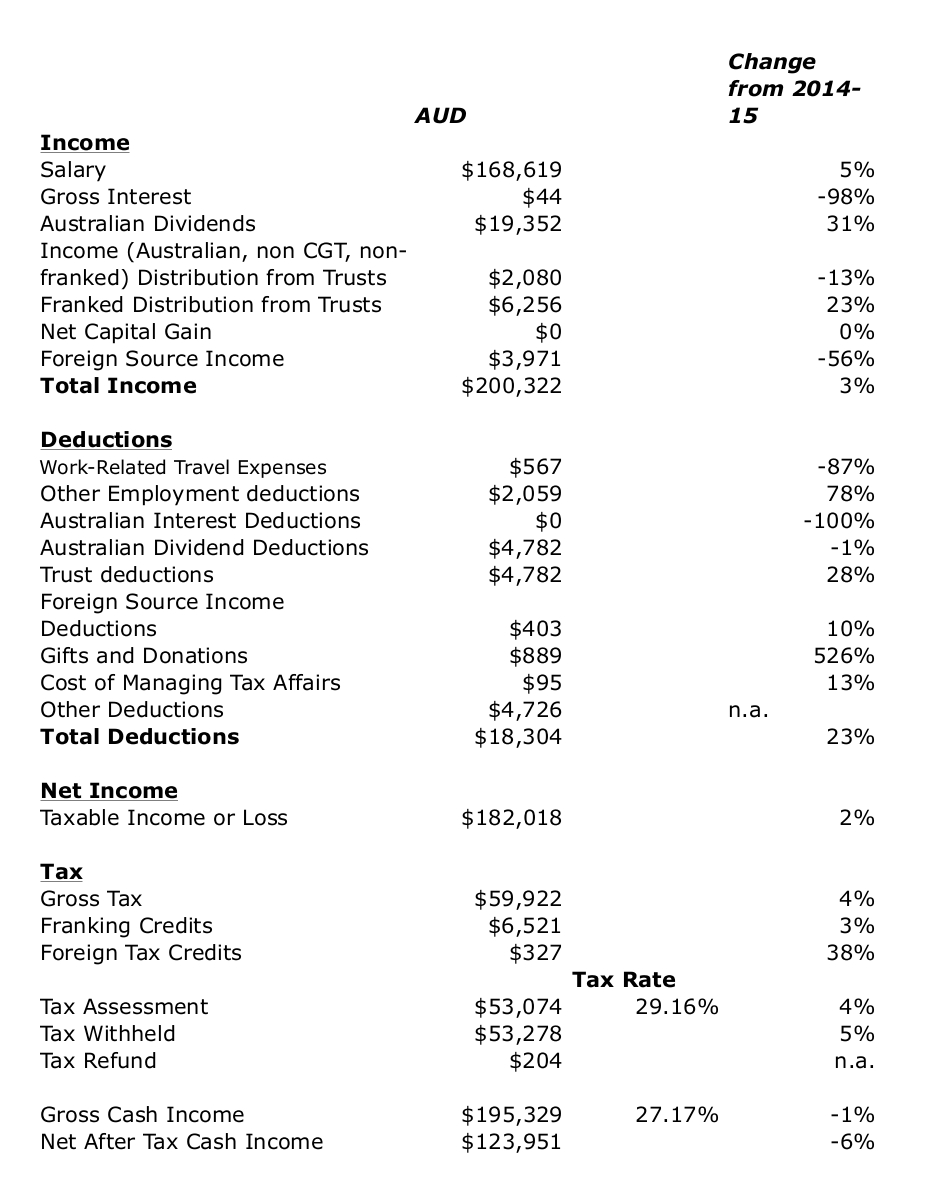

It was another positive month for the markets and us. We did a big restructure of some of our investments, which I'll discuss after this month's numbers. Here are our monthly accounts (in AUD):

Spending (not counting mortgage) was normal at $7.8k. Salaries etc. added up to $11.8k (after tax). After taking into account the mortgage payment of $3.8k (which includes

implicit interest saving due to our offset account - the actual mortgage payment was about $650 less than this) - which shows up as a transfer to the housing account, we saved only $250 on the current account. We made $3.6k of retirement contributions, and saved a net $1.8k in added housing equity. Net saving was, therefore, $5.7k across the board. One reason for higher spending is that we are now spending $306 a week (for 3 days) for childcare and so far not getting any government benefit for this. Yes, people on our income can get a big subsidy for childcare here in Australia.

Spending (not counting mortgage) was normal at $7.8k. Salaries etc. added up to $11.8k (after tax). After taking into account the mortgage payment of $3.8k (which includes

implicit interest saving due to our offset account - the actual mortgage payment was about $650 less than this) - which shows up as a transfer to the housing account, we saved only $250 on the current account. We made $3.6k of retirement contributions, and saved a net $1.8k in added housing equity. Net saving was, therefore, $5.7k across the board. One reason for higher spending is that we are now spending $306 a week (for 3 days) for childcare and so far not getting any government benefit for this. Yes, people on our income can get a big subsidy for childcare here in Australia.

The Australian Dollar rose from USD 0.7580 to USD 0.7686. The ASX 200 gained 2.25%, the MSCI World Index gained 2.85%, and the S&P 500 3.97%. We gained 1.83% in Australian Dollar terms and gained 3.23% in US Dollar terms. So, we underperformed the Australian market and outperformed the international markets. The best performer in dollar terms the CFS Geared Share Fund ($11k) followed by Oceania Capital Partners (OCP.AX), which gained $4k. Every asset class gained, with private equity the best performing asset class and Australian small cap stocks the worst.The worst performer was the CFS Global Resources Fund down $1.9k.

As a result of all this, net worth rose AUD 36k to $1.745 million (new high) or rose USD 45k to $US 1.341 million (ditto).

We shifted most of our Colonial First State managed funds and superannuation from the old now closed to new investors retail platforms to the newer wholesale platforms. I have no idea why these new platforms are called wholesale as you don't need to invest very much. The fees are lower on the newer platform. I did a little reallocation especially for my superannuation fund. This reduced our overall exposure to large cap Australian shares by 8% points of total assets. Total leverage (gearing) went down by a similar amount. All other asset classes increased their shares, especially small cap Australian shares. But generally we are now a bit more diversified and a bit less levered and cloe to what I think is an optimal allocation for us.

The Australian Dollar rose from USD 0.7580 to USD 0.7686. The ASX 200 gained 2.25%, the MSCI World Index gained 2.85%, and the S&P 500 3.97%. We gained 1.83% in Australian Dollar terms and gained 3.23% in US Dollar terms. So, we underperformed the Australian market and outperformed the international markets. The best performer in dollar terms the CFS Geared Share Fund ($11k) followed by Oceania Capital Partners (OCP.AX), which gained $4k. Every asset class gained, with private equity the best performing asset class and Australian small cap stocks the worst.The worst performer was the CFS Global Resources Fund down $1.9k.

As a result of all this, net worth rose AUD 36k to $1.745 million (new high) or rose USD 45k to $US 1.341 million (ditto).

We shifted most of our Colonial First State managed funds and superannuation from the old now closed to new investors retail platforms to the newer wholesale platforms. I have no idea why these new platforms are called wholesale as you don't need to invest very much. The fees are lower on the newer platform. I did a little reallocation especially for my superannuation fund. This reduced our overall exposure to large cap Australian shares by 8% points of total assets. Total leverage (gearing) went down by a similar amount. All other asset classes increased their shares, especially small cap Australian shares. But generally we are now a bit more diversified and a bit less levered and cloe to what I think is an optimal allocation for us.