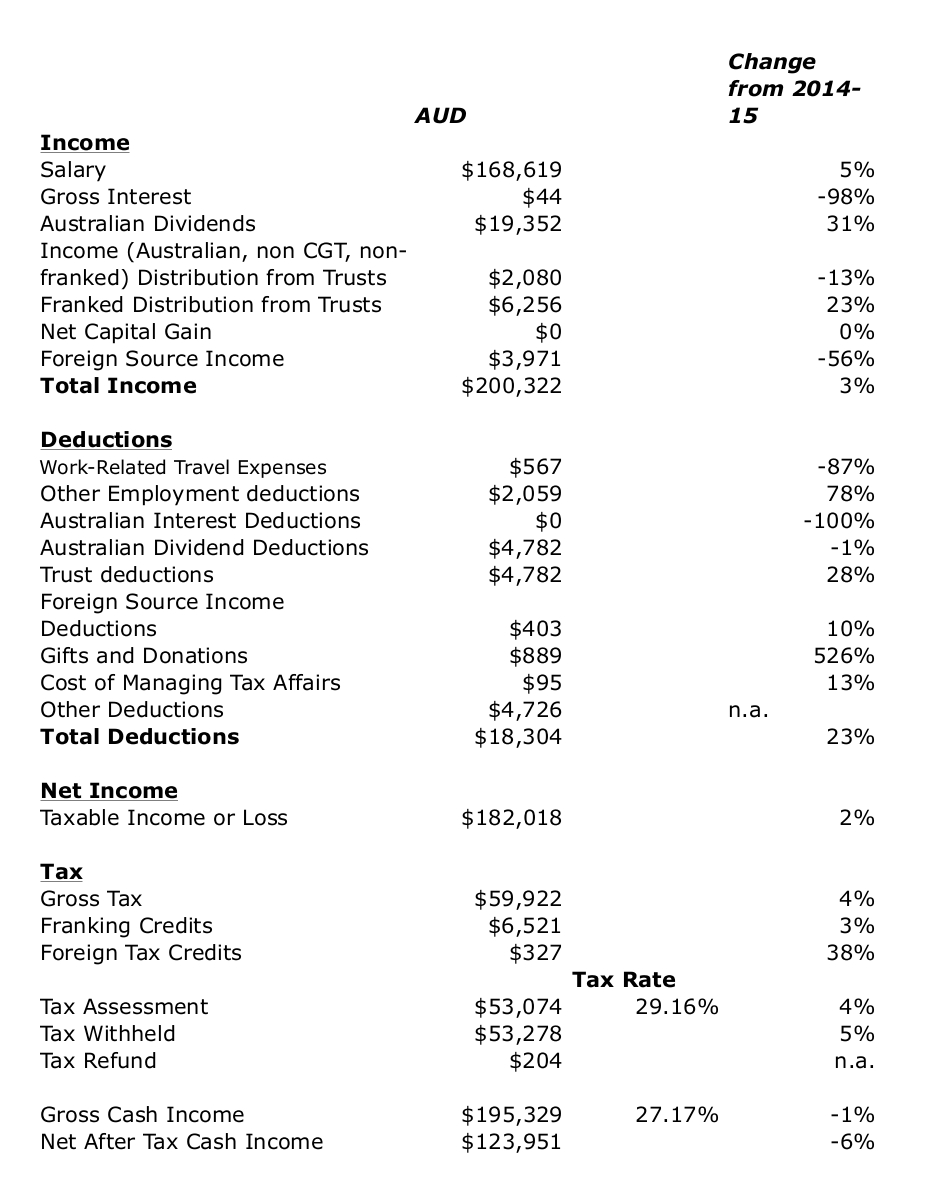

This was a good month all round - both strong investment performance and moderate spending. Here are our monthly accounts (in AUD):

Spending (not counting mortgage) was low at $4.6k. No large and exceptional purchases this month. Salaries etc. added up to $10.4k. Snork Maiden is again earning money - this are payments at the minimum wage she is receiving from the government through her employer while on maternity leave. I think there about 3 months of those. We decided to receive those now in the new financial year to minimize her taxes by spreading her maternity pay over two financial years.

After taking into account the mortgage payment of $3.6k - there were three mortgage payments this month (and which includes

implicit interest saving due to our offset account - the actual mortgage payment was about $420 less than this) - which shows up as a transfer to the housing account, we saved $2.2k on the current account. We made $3.1k of retirement contributions , and saved a net $1.6k in added housing equity. Net saving was, therefore, $6.9k across the board.

The Australian Dollar rose from USD 0.7433 to USD 0.7598. The ASX 200 rose 6.29%, the MSCI World Index 4.34%, and the S&P 500 rose 3.69%. We gained 5.27% in

Australian Dollar terms and 7.61% in US Dollar terms. So we underperformed the Australian market and outperformed the international markets. The best performing investment (in total dollars not RoR) was, not surprisingly, the Colonial First State Geared Share Fund, which gained $34k. Unisuper and PSSAP gained $9k and $7k, respectively. There were lots of other strong performers. IPE,AX was the worst performer losing $750. All asset classes gained, with Australian Small Caps the best at 6.54%.

As a result of all this, net worth rose AUD 72k to $1.600 million or rose USD 80k to $US 1.216 million.

Colonial First State closed new applications to their retail First Choice Investments platform. This made me realise that the minimum investment for the wholesale version of this platform is now only $5,000. I had thought it would be $100k per fund or something like that. Management fees are lower for the wholesale platform. As a result it absolutely makes sense to move my CFS superannuation account to this platform. Probably, moving our managed (mutual) funds will result in capital gains tax bills. As I mentioned last month, I have a large carried over capital loss, of more than $60k. I estimate that moving all my managed funds will result in a capital gain of $50k. So, I would still have a capital loss carryover. Yes, this has an opportunity cost as it brings nearer the day that I would have to pay capital gains tax. The actual bill would be $12k. The value of funds is $222k. It would, therefore, take around 8 years to pay off in terms of lower management fees. But I figure that if I keep the funds "forever" it is worth it and if I sell at some point in the nearer future I will have to pay CGT anyway. Also, if Labor get into government next time, they are likely to raise the capital gains tax rate.

For Moominmama (formerly Snork Maiden), the number of years to pay off the tax hit is shorter and this year her tax rate (due to maternity leave) will be lower than other years. So, that's a no brainer.

Just need to find time to meet with someone at the bank and discuss all the details. Probably will wait a couple of months as workwise this is a crunch time in the next couple of months.