Reading one of ESI Money's millionaire interviews I was inspired to track our income from previous tax returns (all on this blog). While I was at it, I added the tax as well:

Reading one of ESI Money's millionaire interviews I was inspired to track our income from previous tax returns (all on this blog). While I was at it, I added the tax as well:

I just completed our tax returns for this year. As usual they only took a few hours as I am very well-prepared with spreadsheets updated throughout the year. Preparing taxes is mainly a case of checking that all the spreadsheet links and calculations are correct and refreshing my memory about some of the details of what goes where on the tax form. Last year's taxes are here.

On the income side, Australian dividends, capital gains, and foreign source income are all up strongly. My salary still dominates my income sources but is not really growing and we have a pay freeze for next year.

Interest is Australian interest only and is up strongly due to interest on Macquarie, Woolworths, and Virgin Australia bonds.

Unfranked distributions from trusts is up strongly due to the huge distribution from the APSEC fund I invested in just before the end of the tax year. That was a bad move. Foreign source income is mostly dominated by foreign bond interest and losses on futures trading. Other income is gains on selling bonds. These aren't counted as capital gains.

After recording a net capital gain for the first time in a decade last year, I again have zero capital gains and I am carrying forward around $150k in losses to next year. Foreign source income is mostly from futures trading and bond interest.

In total, gross income rose 6%.

Increased deductions are mostly due to losses on selling bonds. Interest rates are historically low and most bonds that you will be able to buy have higher nominal interest rates. As a result, these bonds are priced above par. If you hold them to maturity you have a loss that is more than offset by the interest received.

Dividend, foreign source income, and trust deductions are all mostly interest on loans.

Total deductions rose strongly, and as a result, net income fell 2%.

Gross tax is computed by applying the rates in the tax table to the net income. In Australia, you don't enter the tax due in your tax return, but I like to compute it so that I know how big or small my refund will be.

Franking credits (from Australian dividends), foreign tax paid, and the

Early Stage Venture Capital (ESVCLP) offset are all deducted from gross

tax to arrive at the tax assessment. I again expect to pay extra tax.

I paid 30% of net income in tax. Tax was withheld on my salary at an average rate of 32%.

Moominmama's (formerly Snork Maiden) taxes follow:

Her salary was down a lot because of maternity leave. Dividends and capital gains were up strongly due to investment in various listed investment companies and Commonwealth Bank hybrid securities. Foreign source income was down strongly due to losing on trading this year rather than gaining last tax year. As a result, total income fell by 23%.

Deductions rose dramatically, because of recording trading losses as deductions and starting to deduct interest against dividends. As a result, net income fell 42%. Tax was 15% of net income. Tax withheld on her salary was really high for this income level.

I posted recently the internal rates of return for 66 of my investments. I've now completed the calculations for all 94 investments that were held for more than one year:

Shaded returns are investments that I currently hold. The median rate of return is 5.1%. Most of the larger investments are above the median as are the majority of current investments. The median return of current investments is 9.1%.

Powertel and Looksmart were some dotcom era investments that worked out. DeepSkyWeb one that didn't. I can't even remember what FTS was. I held it in 2007-8. Newcastle was a mortgage fund that blew up in the GFC. Legend was a Joe Gutnick mining company that went to zero and HIH an insurance company that was the worst bankruptcy in Australia's history.

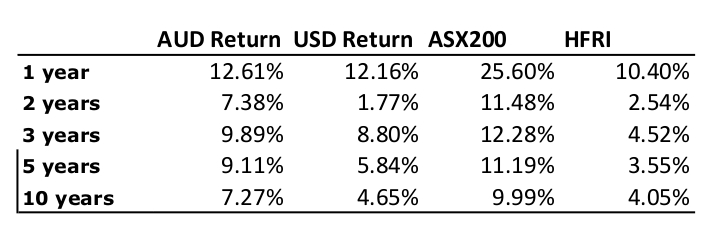

As my performance statistics over the last 5 years are looking good again, I thought I would start posting them again :)

The first two rows give the average annual rate of return and the Sharpe statistic in the two currencies. These are the kind of numbers I would aim for... Until recently, I was performing better in Australian Dollar terms. Now it depends on which statistic you look at.

The remaining four lines compare performance to the MSCI (global stocks), ASX200 (Australian stocks), and HFRI (Hedge fund) indices. The first two have all dividends and tax credits included. My portfolio has a subdued reaction to the first two indices (beta < 1) but is more volatile than HFRI. Alpha is the annual return after deducting the part explained by the index. It helps increase the upside and reduce the downside moves.

The final two rows show the same thing in a different way. Down capture divides the average return of the portfolio by the average return of the index in the months that the index went down. Up capture does the same in the months that the index rose. I have a positive asymmetry against all three indices.

I have now computed the internal rate of return for 66 investments including all current investments. I excluded all trading involving futures, shorting etc and all names held for less than a month. There are still around a hundred closed investments that need to still be evaluated. In the meantime, here are the results:

I was just listening to a pod-cast where the host asked the guest (Karsten Jeske) what their best investment was and they could give an answer in annual percentage terms. Up to now, I have tracked returns of individual investments in absolute dollar terms. I can easily say which has been my best and my worst on that basis. The best was the Colonial First State Geared Share Fund and the worst has been the Tribeca Global Resources Fund. But dollar returns depend on the amount invested. I do have average monthly percentage returns for many investments, but properly taking into account transactions is hard. So, I thought that I could compute the internal rate of return. This does take all transactions properly into account. You need to compute each monthly net cashflow into the investment (which I already have in individual spreadsheets I keep on each investment) and then for the current month assume that the investment is sold at the current price. Excel has an IRR function that can be applied to the column of cashflows.

I plan to do this slowly as I have invested in around 200 different things. The first three I did are gold (34% p.a.), China Fund (14% p.a.), and 3i (6% p.a.). 3i was surprising as this is a lot less than the average annualized monthly return of almost 14%, that I previously computed.

Masterworks are a fairly new firm offering securitized investments in artworks. They buy paintings by recent and living artists and then sell shares to investors. They charge a 1.5% per annum management fee and plan to charge 20% of profits when an artwork is sold. They also get a markup on the price that they pay, presumably to cover acquisition and offering costs. I am interested in investing a small amount and have scheduled an interview to talk to them. They interview all new clients. One thing that interests me is our family connection to art. My father's family were antique and art dealers before the Second World War in Germany. My brother is an amateur artist who has sold a couple of paintings, I think, and my mother painted as well. But this doesn't give me any particular insight on the financial side of the art market. I'd aim to diversify across the paintings they are offering.

This investment is more equivalent to private equity buyout rather than venture capital. It doesn't make sense for the firm to buy a painting for $10k or $100k by an unknown artist hoping that it will appreciate because they make a separate special purpose vehicle filed with the SEC for each of their offerings. So they are buying paintings at around $2 million or so a piece.

P.S. 25 August

I had my interview today with a representative from Masterworks and was approved to start investing. I learnt that there is a USD10k minimum investment for the primary offerings. I now made my first purchase and have transferred the money using OFX. Based on the spot exchange rate, it cost 1.45%. I tried using my US bank but couldn't work out an online method that works.

The value of shares in the Aura Venture jumped from AUD 0.75 to AUD 1.28 in the June quarter. This turned our performance for June from a negative Australian Dollar return to a positive 0.84%.

The 75 cents price reflects that only 75% of the capital was called at that point. Since then there was a further 10 cents call. This big increase moves this investment from a losing investment to our 7th best of all time in dollar terms. And the gains are tax-free. Of course, all such valuations are somewhat theoretical until they actually exit the investments, but it makes me feel better about this investment and my commitment to invest in their next fund. On the other hand, the portfolio value was upvalued based on the announced acquisition of one investee company at around 2 times the entry price and a funding round at another that reflected a valuation 109% premium over the fund's entry point.

Given the continued underperformance of managed futures, I think I am going to again lower my allocation to this asset class to 5% from 10%. I've never gotten above 5% in managed futures funds anyway. In place of this, I could raise the allocation to real estate to 15% or raise both real estate and gold to 12.5%. Or is there something else I should allocate capital to?

The table presents snapshots on 1 February, before the pandemic had effects in Western countries, and today. The number of shares held is self-explanatory. Investment is the net cash invested in that investment. So, making an investment increases the number and withdrawal reduces it, but dividends and distributions that aren't re-invested also reduce it. All the numbers are in Australian Dollars and so the numbers also declined for 3i, Boulder, China Fund, and Pershing as the Australian Dollar rose. Investment per share is the investment number divided by the number of shares.

In total, I added $334k to these investments over this period. Most of this money came from maturing bonds. There are a lot of different patterns though. I might have made a mistake in investing the most in funds that were trading at the biggest discount to net asset value rather than what turned out to be the strongest funds. I didn't invest anything in Hearts and Minds and not much in Regal. I got a lot of extra shares in Cadence and Tribeca, which is a bet that they'll do better in the future. I increased my Pengana investment mostly because I thought I needed to invest more in private equity and because the fund had been trading at a big premium to net asset value. It's partly a bet that the premium will come back.

In general though, I have been cautious investing during this period because I invested a lot in early 2008 after the initial fall in the market, only to lose big later in the year.