Following up on my post on the best portfolios for Australia, this post will lay out the new target portfolio allocation. The basic idea is to reduce the allocation to managed futures from 25% in my previous target portfolio to 10%. This is because I plan to do little active trading going forward and futures funds have had lacklustre performance for several years. Maybe they will come back, but we should see them more as a potential hedge than as a main asset class at this point I think.

At the top level the portfolio is 60% in stocks and 40% in other assets. The other assets are allocated equally between bonds, futures, gold, and real estate. The stocks allocation is roughly equally divided between Australian and international stocks. 10% of the portfolio is allocated to private equity and 50% to public. Then the public allocation is divided between long only and hedge fund strategies. Within the long only Australian allocation, 1/3 is devoted to small cap stocks. The full allocation is:

10% Australian large cap

5% Australian small cap

12.5% International stocks

10.75% Australian oriented hedge funds

10.75% International oriented hedge funds

10% Private equity

10% Bonds

10% Real estate

10% Gold

10% Managed futures

1% Cash

We will also usually use some leverage or gearing. 1% in cash seems sufficient given the ability to borrow.

Sunday, December 29, 2019

The Best Portfolio for Australia

The portfolio charts website, I wrote about before, now lets you do analysis using Australian assets, inflation etc! It turns out that the best portfolio for Australia isn't the same as the best for the US... The following table shows the average and standard deviation of real returns, the maximum drawdown, and the safe and permanent withdrawal rates (preserves capital) for a 30 year retirement horizon:

This is based on data since 1970. Based on the permanent withdrawal rate the Ivy Portfolio developed by Meb Faber is best. The 100% Aussie stocks portfolio (TSM) has a slightly higher return, but the lowest permanent withdrawal rate. So, I think Aussie investors should start to think about portfolio design from something similar to the Ivy Portfolio. It's no surprise that I have been a fan of Meb Faber and endowment style portfolios...

This is based on data since 1970. Based on the permanent withdrawal rate the Ivy Portfolio developed by Meb Faber is best. The 100% Aussie stocks portfolio (TSM) has a slightly higher return, but the lowest permanent withdrawal rate. So, I think Aussie investors should start to think about portfolio design from something similar to the Ivy Portfolio. It's no surprise that I have been a fan of Meb Faber and endowment style portfolios...

Using ETFs, this portfolio recommends putting 20% into each of Australian stocks, international stocks, intermediate term bonds, commodities, and REITs.

Using the build your own portfolio tool you can see what tweaking this beginning portfolio can do. For example, replacing half the commodities allocation with gold and half the bond allocation with extra international stocks, increases the return to 6.1% and the SWR and PWR to 5.2% and 4.4% with almost no increase in drawdowns.

Going to 60% stocks divided equally between Australia and the rest of the world and 10% in each of bonds, gold, commodities, and REITs, is actually quite similar in return profile to the Ivy Portfolio. The key thing is to hedge Australian stocks with international and real assets. This latter portfolio is probably going to tbe basis of my own new target portfolio.

Using ETFs, this portfolio recommends putting 20% into each of Australian stocks, international stocks, intermediate term bonds, commodities, and REITs.

Using the build your own portfolio tool you can see what tweaking this beginning portfolio can do. For example, replacing half the commodities allocation with gold and half the bond allocation with extra international stocks, increases the return to 6.1% and the SWR and PWR to 5.2% and 4.4% with almost no increase in drawdowns.

Going to 60% stocks divided equally between Australia and the rest of the world and 10% in each of bonds, gold, commodities, and REITs, is actually quite similar in return profile to the Ivy Portfolio. The key thing is to hedge Australian stocks with international and real assets. This latter portfolio is probably going to tbe basis of my own new target portfolio.

Thursday, December 12, 2019

Pulling the Plug on Short-Term Trading

I've decided to stop short-term trading. In recent months it hasn't made any money, it takes up a lot of time, and it gives me a lot of anxiety. Even though I am doing systematic trading I find myself looking at the market a lot and worrying about my positions. I can't seem to stop it. And my current position sizes are quite small. After a sleepless night, I've had enough. I already cancelled my orders that were waiting to execute. I will keep the existing Bitcoin and palladium positions until they exit naturally

Going forward, I will need to think about our overall financial plan again. Trend following funds aren't doing well in recent years, so we won't want to allocate that much to them compared to the current target allocation to "futures". What should we invest in instead? Should I still plan to set up an SMSF? I delayed that while I waited to see if trading was going to be a big part of it.

I've been here a couple of times before.

Friday, December 06, 2019

Trading Update

Well, that didn't last long. In November's report I said I would raise the risk allocation to palladium and soybeans. I just got stopped out of palladium futures though the contract is ending the day more or less where it began. I actually made a little money on the trade, but I'm not willing to take so much risk. So, I'm going to go back to trading palladium CFDs with a smaller amount of risk. I'll cut soybeans back to USD 2,500 risk as well. Yesterday, Bitcoin had a double stop out. First the long position was closed for a loss and a short opened and then the short was stopped out intraday. After all that, the contract ended near where it started:

I'm seriously thinking again of giving up on trading. Yes, you can make money doing this and I am now disciplined enough to always do the trades the algorithm says to do. But in practice there is still quite a lot of anxiety and mood swings. If I keep trading so small that I only make say a thousand dollars a month at it, it's not really worth the hassle. But if I make it big enough to make a difference I will have too much anxiety. That's the dilemma at this point. So far this financial year I am just losing money. I've given back all of last month's profit in the first week of this month.

I'm seriously thinking again of giving up on trading. Yes, you can make money doing this and I am now disciplined enough to always do the trades the algorithm says to do. But in practice there is still quite a lot of anxiety and mood swings. If I keep trading so small that I only make say a thousand dollars a month at it, it's not really worth the hassle. But if I make it big enough to make a difference I will have too much anxiety. That's the dilemma at this point. So far this financial year I am just losing money. I've given back all of last month's profit in the first week of this month.

Monday, December 02, 2019

November 2019 Report

A less frenetic month financially but somehow I didn't get to make any blogposts since October's monthly report. We started on refinancing our mortgage at a lower interest rate, but the transaction is not yet complete.

The Australian Dollar fell from USD 0.6894 to USD 0.6764. The MSCI World Index rose 2.48% and the S&P 500 3.63%. The ASX 200 gained 3.51%. All these are total returns including dividends. We gained 2.17% in Australian Dollar terms but only 0.25% in US Dollar terms. The target portfolio is expected to have gained 1.53% in Australian Dollar terms and the HFRI hedge fund index is expected to have gained 0.75% in US Dollar terms. So, we out-performed our target portfolio but lagged other benchmarks. Updating the monthly AUD returns chart:

The Australian Dollar fell from USD 0.6894 to USD 0.6764. The MSCI World Index rose 2.48% and the S&P 500 3.63%. The ASX 200 gained 3.51%. All these are total returns including dividends. We gained 2.17% in Australian Dollar terms but only 0.25% in US Dollar terms. The target portfolio is expected to have gained 1.53% in Australian Dollar terms and the HFRI hedge fund index is expected to have gained 0.75% in US Dollar terms. So, we out-performed our target portfolio but lagged other benchmarks. Updating the monthly AUD returns chart:

Here is a report on the performance of investments by asset class (futures includes managed futures and futures trading):

Stocks and real estate did well while hedge funds, private equity, and gold did poorly. The largest positive contribution to the rate of return came from large cap Australian stocks and the greatest detractor was gold. The returns reported here are in currency neutral terms.

Things that worked well this month:

- The Unisuper superannuation fund gained more than any other investment in dollar terms.

- Soybeans and Bitcoin were the next best performers.

- Crude oil and gold lost heavily.

- Regal Funds (RF1.AX) fell sharply after it was reported that the firm was under investigation by the regulator, ASIC.

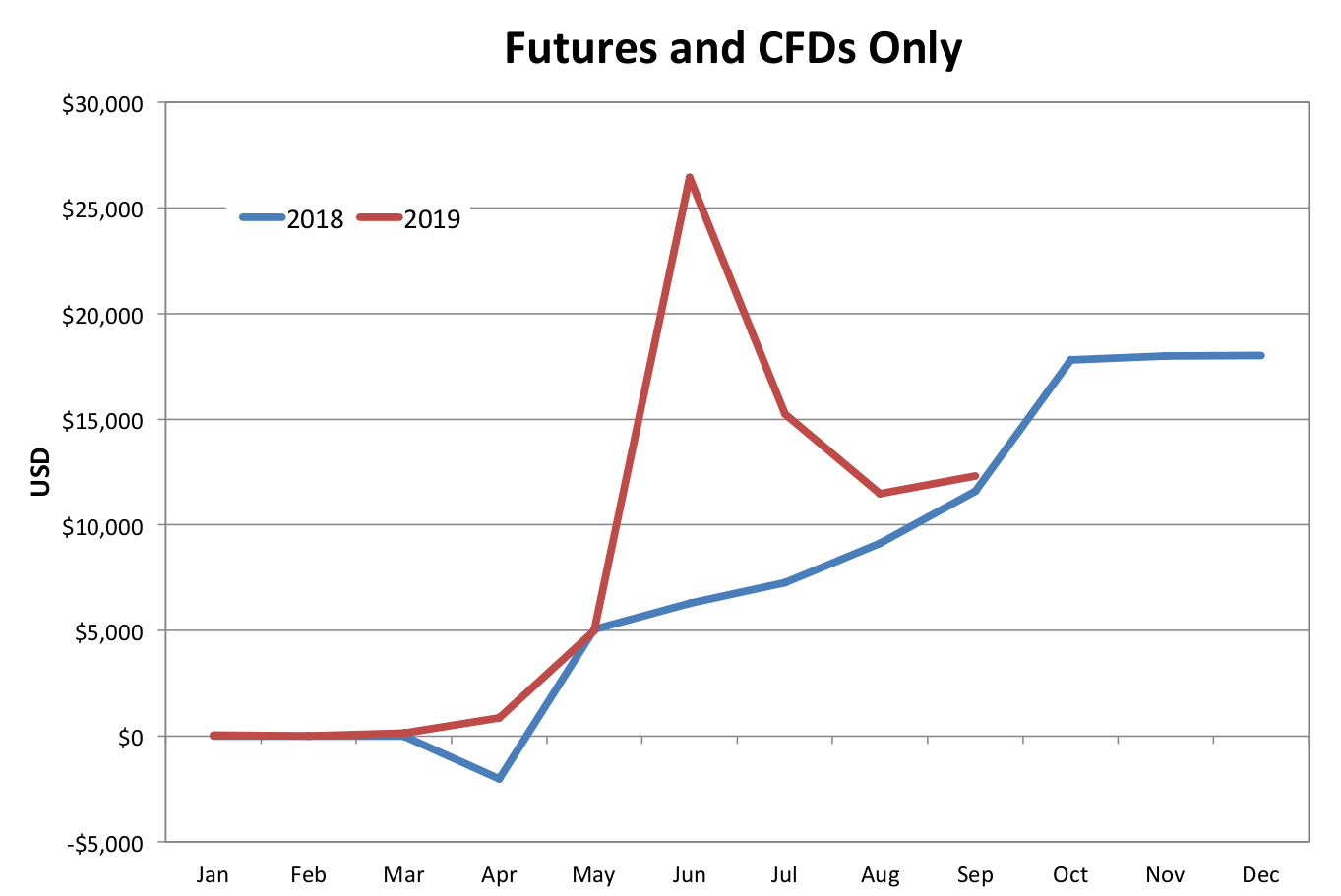

Using a narrower definition including only futures and CFDs we made 3.55% on capital used in trading or USD 6.5k. Including ETFs we lost just 0.01% or AUD 46. Using the narrow definition, we are catching up to last year's returns. This graph shows cumulative trading gains using the narrower definition year to date:

I think I should increase the risk allocations to soybeans and palladium to USD 5,000 each from USD 2,500 and AUD 1,250 currently. These would be roughly the allocations suggested by the portfolio optimization given current allocations to Bitcoin and oil (USD 3,670 and 2,500). Risk allocation is the maximum potential loss on a single trade.

We moved further towards our new long-run asset allocation.

On a regular basis, we invest AUD 2k monthly in a set of managed funds, and there are also retirement contributions. Other moves this month:

- I rebought 100,000 shares of Domacom (DCL.AX).

- I bought 10,000 shares of Regal Funds (RF1.AX) after the price fell sharply following an ASIC investigation of the firm.

- USD 100k of bonds (Virgin Australia & Viacom) matured. I bought USD 25k of Dell, 16k of Nustar, and 25k of Tupperware bonds. So our direct exposure to corporate bonds fell by USD 34k.

- I transferred AUD 45k to my Colonial First State superannuation account, investing in the Conservative Fund.

- I bought around AUD 43k and GBP 7k, selling US dollars.

- I bought 750 shares of 3i.

Saturday, November 30, 2019

Performance of Optimal Portfolio

The graph shows the monthly profits from idealized trading of an optimal portfolio of Bitcoin, palladium, crude oil, and soybeans futures. The risk budget is the maximum loss possible in one day under ideal conditions.

My results this year somewhat track these. My trading hasn't always been ideal, I have been developing my methods, and my portfolio doesn't have the optimal weights yet. Midyear there were strong returns available and I also did well. Then, in the last four months returns were lower or negative and I also lost money. November was again a good month though not as good as April-June.

Next month I am looking to move closer to the optimal weights and increase the risk budget so that the average return would in theory be around the same amount as my salary, which is one of the goals I have set.

Monday, November 25, 2019

PAYG Installments

I received a letter from the Australian Tax Office that I need to pay quarterly estimated tax payments. However, if the total estimated tax is less than AUD 8,000 you can pay the installments annually. If you self-prepare your tax this means apparently that you don't actually need to pay any installments. So, I selected that option online.

On the other hand, I think Moominmama is going to need to make quarterly payments.

On the other hand, I think Moominmama is going to need to make quarterly payments.

Saturday, November 02, 2019

October 2019 Report

This month we "inverted" our mortgage, paying off the mortgage and then redrawing it for investment purposes. As a result the mortgage interest should now be tax deductible. I carried out quite a lot of trades and money shuffling to carry this out.

The Australian stockmarket fell a bit in October and the Australian Dollar rose, but overseas markets rose. The Australian Dollar rose from USD 0.6752 to USD 0.6894. The MSCI World Index rose 2.76% and the S&P 500 2.17%. The ASX 200 fell 0.35%. All these are total returns including dividends. We lost 0.20% in Australian Dollar terms but gained 1.90% in US Dollar terms. The target portfolio lost 1.03% in Australian Dollar terms and the HFRI hedge fund index is expected to have gained 0.83% in US Dollar terms. So, we out-performed our target portfolio, the HFRI, and the ASX, while underperforming compared to the MSCI World Index and the S&P 500 (a bit). Updating the monthly AUD returns chart:

Hmmm... It is looking like my performance is an average of the MSCI and the target portfolio in recent months.The Australian stockmarket fell a bit in October and the Australian Dollar rose, but overseas markets rose. The Australian Dollar rose from USD 0.6752 to USD 0.6894. The MSCI World Index rose 2.76% and the S&P 500 2.17%. The ASX 200 fell 0.35%. All these are total returns including dividends. We lost 0.20% in Australian Dollar terms but gained 1.90% in US Dollar terms. The target portfolio lost 1.03% in Australian Dollar terms and the HFRI hedge fund index is expected to have gained 0.83% in US Dollar terms. So, we out-performed our target portfolio, the HFRI, and the ASX, while underperforming compared to the MSCI World Index and the S&P 500 (a bit). Updating the monthly AUD returns chart:

Here is a report on the performance of investments by asset class (futures includes managed futures and futures trading):

Things that worked well this month:

- Pengana Private Equity and Bluesky Alternatives did very well, gaining AUD 8.7k and AUD 10k, respectively. Hearts and Minds gained AUD 5.3k.

- Gold gained (AUD 7.3k).

- Winton Global Alpha lost significantly, reversing recent gains.

- Pershing Square, Cadence Capital, and Tribeca Natural Resources all lost money.

We moved further towards our new long-run asset allocation.

On a regular basis, we invest AUD 2k monthly in a set of managed funds, and there are also retirement contributions. Other moves this month:

- USD 21K of Kraft-Heinz bonds were called early and we didn't buy any new bonds So, our direct bond holdings declined by USD 21k.

- We traded at a small loss, as discussed above.

- I sold 100k of Domacom (DCL.AX), 40k of Tribeca Global Natural Resources (TGF.AX), and 79k of Cadence Capital (CDM.AX) shares to harvest tax losses and obtain cash for the mortgage inversion. I subsequently bought back 40k of Tribeca and 80k of Cadence. I now have the funds which are marginable and/or are likely to pay large franking credits in my account and the non-marginable funds, which mostly also are likely to pay out fewer franking credits in Snork Maiden's account. As franking credits are applied to the tax bill it doesn't actually matter which account they are in, but I like to see my larger tax bill cut more :) I have a margin account with Commonwealth Securities, while Interactive Brokers don't offer margin loans to Australian customers.

- I bought 20k shares of Hearts and Minds (HM1.AX) before the upcoming annual Sohn Conference. The fund is currently winding down the investments in the stocks recommended at the last conference and will invest in new recommendations following this year's conference. The share price is very close to NAV and I think following the conference there could be a boost in price. The fund has done very well since inception.

- I went to Regal Fund's presentation here and was impressed and bought 20k more shares of RF1.AX.

- I sold 50k of Pengana Private Equity (PE1.AX) shares because the price seemed unsustainably high but then bought back 50k at lower prices. This is not looking like a good move given the tax implications

- We bought AUD 40k of Australian Dollars.

- We moved around AUD 1/4 million to our offset account and paid off the mortgage. We then redrew AUD 1/2 million and sent it to my CommSec account and Moominmama's Interactive Brokers account. This reduced my margin loan a lot and increased the cash in her account a lot. The latter is deemed to be "futures" in the pie chart above. Cash in our offset account fell to AUD 40k.

Passed-in at Auction

There was an auction today for the house next door to us. It is almost identical though it is in better condition inside (our house will probably need AUD10-20k of refurbishment to put on the market I reckon). It doesn't have as good views/surroundings. The highest bid was AUD 690k from a bidder in another state on the phone and it passed in. Unless there was a post-auction negotiation, I guess we will see it on the market next week at a fixed price. Next week we should also hear from HSBC on how much their valuer values our house at.

P.S. 7 November

This house is now for sale at $829,500. In the meantime, the bank's valuer valued our house at $850,000. I guess they want to sell fast.

Wednesday, October 30, 2019

Mortgage Refinancing: Reality Check

I met today with a "Premier Relationship Manager" at HSBC. We are going ahead with the mortgage refinancing. They will send a valuer to value our house tomorrow...

So, she first checked whether I could service the loan based on the data I submitted. Based on just my salary of AUD 176k per year and our spending and a AUD 500k loan the answer was no. Given my salary is supposedly in the top 5% or higher, our house value is only a bit above the median price for houses here, and lots of people drive luxury cars etc. and we don't, you'd think this wouldn't be a problem. She said our spending was "very high". Either government income data is too low (but the banks ask for tax returns), or people somehow hide spending from the banks (but the banks ask for bank statements), or what? It's hard to reconcile what I see with the data.

Our net worth is in the top 300,000 or so of households and my income in the top 400,000 of taxpayers according to this official data.

By the way, five plus years ago, when we were looking to buy a house, the banks were willing to lend us much more money. Lending standards really have tightened.

So, she first checked whether I could service the loan based on the data I submitted. Based on just my salary of AUD 176k per year and our spending and a AUD 500k loan the answer was no. Given my salary is supposedly in the top 5% or higher, our house value is only a bit above the median price for houses here, and lots of people drive luxury cars etc. and we don't, you'd think this wouldn't be a problem. She said our spending was "very high". Either government income data is too low (but the banks ask for tax returns), or people somehow hide spending from the banks (but the banks ask for bank statements), or what? It's hard to reconcile what I see with the data.

Our net worth is in the top 300,000 or so of households and my income in the top 400,000 of taxpayers according to this official data.

By the way, five plus years ago, when we were looking to buy a house, the banks were willing to lend us much more money. Lending standards really have tightened.

Monday, October 28, 2019

Capitalise

Capitalise is an automated trading platform that uses commands written in near natural English at a very high level. I heard about it when Interactive Brokers told us that we now have access to it. At the moment the service is free. You can put in commands where buy/sell levels and stops depend on functions of past prices and also various technical indicators. There is no need to learn a formal programming language like Python or understand any of the intricacies of actually executing strategies. They are based in Israel.

This would be great for me except at the moment it doesn't allow position sizing based on functions of prices. You have to give it a numerical position size. I chatted with Arica on their platform and she said that they might develop that functionality in the future. For now I can handle updating my orders each morning (Australian time) as I am only systematically trading in 3 markets (Bitcoin, palladium, and oil). Maybe they will have this functionality by the time I can't handle trading manually anymore and I won't need to learn Python etc or collaborate with someone who does know that stuff.

This would be great for me except at the moment it doesn't allow position sizing based on functions of prices. You have to give it a numerical position size. I chatted with Arica on their platform and she said that they might develop that functionality in the future. For now I can handle updating my orders each morning (Australian time) as I am only systematically trading in 3 markets (Bitcoin, palladium, and oil). Maybe they will have this functionality by the time I can't handle trading manually anymore and I won't need to learn Python etc or collaborate with someone who does know that stuff.

Sunday, October 27, 2019

Mortgage Inversion Complete, What Next?

I completed the transfer of money into our brokerage accounts from the "mortgage inversion". That completes a major step in our financial restructuring since the inheritance. We've completed the first two steps on this list. I am thinking of refinancing our mortgage to get a lower interest rate now I don't care about having an offset account with my main bank. But how to go about this? Should I go to a mortgage broker or just contact a bank, like HSBC, who are offering a low rate?

Saturday, October 26, 2019

Silver, Six Losing Bitcoin Trades in a Row...

I tested silver futures as a possible addition to the trading portfolio. When combined with Bitcoin, palladium, and crude oil its optimal portfolio weight was 2%. So, I'm not going to be trading that.

Overnight and in today action in Bitcoin has been insane. I was up around USD 5k on my last Bitcoin trade and then it became a USD 1k losing trade, the sixth in a row. We switched to long from short and subsequently bitcoin skyrocketed to over 10,000 from around 7,500. This long trade is only one contract though compared with two contracts on the previous short. It seems like this spike might have been generated by Xi Jinping's new enthusiasm for blockchain. He told party members to study blockchain. This is despite China banning cryptocurrency exchanges, though a lot of Bitcoin mining takes place in China.

Overnight and in today action in Bitcoin has been insane. I was up around USD 5k on my last Bitcoin trade and then it became a USD 1k losing trade, the sixth in a row. We switched to long from short and subsequently bitcoin skyrocketed to over 10,000 from around 7,500. This long trade is only one contract though compared with two contracts on the previous short. It seems like this spike might have been generated by Xi Jinping's new enthusiasm for blockchain. He told party members to study blockchain. This is despite China banning cryptocurrency exchanges, though a lot of Bitcoin mining takes place in China.

Wednesday, October 23, 2019

Five Losing Bitcoin Trades in a Row

The bad news is that the worst historical losing run in Bitcoin is eleven losing trades in a row. The good news is that least we now have the losses more under control after adopting position sizing and a constant (more or less as we use rounding of contract numbers) maximum dollar risk. I am also now 100% disciplined in following the algorithms. That was a big struggle. We are now back to short again.

Without slippage the previous trade would have been a $120 win. We had a $30 loss. The last trade though was a $2,000 loss when rounded up to two contracts.

Mortgage Redrawn

Just enter the amount, press the button, and:

Now to transfer the money to investment. This is how I account for this re-structure:

Almost all our historical savings from wages etc ("current savings") have now been converted into housing equity and extra retirement contributions. Housing equity is now a few hundred dollars short of the value of the house as I left a small amount of the mortgage unpaid in order not to potentially trigger something undesirable by totally paying it off.

Tuesday, October 22, 2019

Monday, October 21, 2019

Trading and Mortgage Inversion Update

We switched from short one contract of Bitcoin to long two this morning, booking a USD 30 loss on the short trade. We are long two as the per contract risk is lower now. After four losing Bitcoin trades, hopefully this is a winning one...

I sold a lot of shares this morning and already was allowed to move some of the proceeds to our offset account. I also paid down AUD 100k of the mortgage and was surprised to see that I could redraw it immediately. I had thought I would need to wait to 4th November for the redraw balance to update. This means that I might be able to complete the inversion this week.

P.S.

So I paid off another AUD 300k later in the day. Am still waiting on a transfer of AUD 100k from my margin loan. When I get it I should be able to complete the "inversion".

I sold a lot of shares this morning and already was allowed to move some of the proceeds to our offset account. I also paid down AUD 100k of the mortgage and was surprised to see that I could redraw it immediately. I had thought I would need to wait to 4th November for the redraw balance to update. This means that I might be able to complete the inversion this week.

P.S.

So I paid off another AUD 300k later in the day. Am still waiting on a transfer of AUD 100k from my margin loan. When I get it I should be able to complete the "inversion".

Monday, October 14, 2019

Optimizing Trading Portfolios and Shifting to Return on Risk Metric

I started exploring testing portfolios of trading strategies. For this, I decided that in looking at return on capital where capital is the face value of a futures contract doesn't make much sense. It seems to make more sense to look at the return on money at risk. It makes the most sense to measure that in dollars as a share of a total risk budget. This then leads me to making the primary measure of return also to be in dollars. Here is an optimized portfolio of Bitcoin, oil, and palladium:

The portfolio has a total risk budget of USD 5,000. This is then allocated across the three markets with the resulting profit curves. The analysis assumes that you can trade fractional futures contracts. Oil and palladium help diversify Bitcoin and increase the information ratio. Using a zero benchmark and daily returns on risk the portfolio IR is 2.96 rising from 2.17 for Bitcoin alone.

Oil hasn't gone anywhere in the last year, but did well in 2018 when Bitcoin struggled. Going forward, I will test whether each new market I look at improves the portfolio IR or not.

This approach then also leads to computing the prices for continuous futures contracts additively rather than multiplicatively – so that differences in dollars are preserved -– and to focusing on a constant risk budget in dollars. It also allowed me to simplify the back-testing program quite a bit. In the following chart the blue line is the daily profit curve for trading one contract of Bitcoin futures:

The red curve is based on completed trades only. The green curve has a constant dollar risk equal to the average of the single contract. To be more realistic I have rounded the number of contracts to the nearest whole number, which could be zero. This keeps the strategy out of the market in late 2017 and early 2018, when the single contract strategy had a big drawdown. The constant risk strategy has a higher return and a smaller maximum drawdown than trading a single contract. So, this is the strategy I am adopting for Bitcoin going forward. This morning, we switched from one contract long to one contract short...

The portfolio has a total risk budget of USD 5,000. This is then allocated across the three markets with the resulting profit curves. The analysis assumes that you can trade fractional futures contracts. Oil and palladium help diversify Bitcoin and increase the information ratio. Using a zero benchmark and daily returns on risk the portfolio IR is 2.96 rising from 2.17 for Bitcoin alone.

Oil hasn't gone anywhere in the last year, but did well in 2018 when Bitcoin struggled. Going forward, I will test whether each new market I look at improves the portfolio IR or not.

This approach then also leads to computing the prices for continuous futures contracts additively rather than multiplicatively – so that differences in dollars are preserved -– and to focusing on a constant risk budget in dollars. It also allowed me to simplify the back-testing program quite a bit. In the following chart the blue line is the daily profit curve for trading one contract of Bitcoin futures:

The red curve is based on completed trades only. The green curve has a constant dollar risk equal to the average of the single contract. To be more realistic I have rounded the number of contracts to the nearest whole number, which could be zero. This keeps the strategy out of the market in late 2017 and early 2018, when the single contract strategy had a big drawdown. The constant risk strategy has a higher return and a smaller maximum drawdown than trading a single contract. So, this is the strategy I am adopting for Bitcoin going forward. This morning, we switched from one contract long to one contract short...

Thursday, October 10, 2019

2018-19 Income and Spending Breakdown

After doing our tax returns I can now report the breakdown of income and spending for the 2018-19 financial year, following up on the breakdown for 2017-18:

On the right there is a breakdown of some of the larger categories into sub-categories. Unlike some bloggers I can't say what we spend on food, or clothes etc. I just know how much we spend at different sorts of retail outlets.

One of the biggest changes from last year is the reduction in cash spending from 13% to 3.5% as we started to use credit and debit cards more to track our spending better. Restaurants is up as former cash spending was converted to spending using cards. Other major changes are:

Income was up strongly on the previous year, mainly due to futures trading. As a result, taxes were also up strongly to over AUD 100k. OTOH total spending and saving also rose strongly. Note that "current saving" here is much higher than my usual definition of saving, which only includes saving from salaries and similar income. Here, total income includes investment income and so saving is correspondingly higher.

On the right there is a breakdown of some of the larger categories into sub-categories. Unlike some bloggers I can't say what we spend on food, or clothes etc. I just know how much we spend at different sorts of retail outlets.

One of the biggest changes from last year is the reduction in cash spending from 13% to 3.5% as we started to use credit and debit cards more to track our spending better. Restaurants is up as former cash spending was converted to spending using cards. Other major changes are:

- An increase in health spending from 7% to 16% due mainly to costs of pregnancy/childbirth.

- A major increase in housing spending from 16% to 26% as we undertook renovation work and paid more mortgage interest due to having less money in our offset account.

- A major reduction in travel from 14% to 3% as we only went on a trip to Sydney this year instead of to Europe and Japan.

Income was up strongly on the previous year, mainly due to futures trading. As a result, taxes were also up strongly to over AUD 100k. OTOH total spending and saving also rose strongly. Note that "current saving" here is much higher than my usual definition of saving, which only includes saving from salaries and similar income. Here, total income includes investment income and so saving is correspondingly higher.

Tuesday, October 08, 2019

Planning the Mortgage Inversion

I first wrote about this four years ago. I realized today that I could actually pull this off next month. At this point, I have close to AUD 300k in our bank account (which is an offset account). The mortgage is AUD 490k. If I sell some shares, which are currently in the red, like Tribeca Global Resources, realizing capital losses and transfer some Australian dollars from Interactive Brokers I can reach half a million dollars in our bank account. The amount of cash that can be redrawn is only updated on the 4th of the month, so I will wait to a little later this month to sell the shares and transfer the cash and pay off almost all the mortgage. Then in early November I will redraw the cash and transfer it to our brokers. As the mortgage is in both our names, I will transfer the money 50/50 to accounts in each of our names. After that, almost all of our mortgage interest should be tax-deductible. Of course, I could just pay off the mortgage. But the interest rate for a home equity loan is higher than for an owner occupier mortgage and am happy to have debt at relatively low interest rates and invest it in stuff that hopefully will pay a higher return.

Monday, October 07, 2019

2018-19 Taxes

Here are my taxes for another year:

On the income side, Australian dividends, capital gains, and foreign source income are all up strongly. I finally ran out of past capital gains tax losses and so recorded a net capital gain for the first time in a decade. Foreign source income is mostly from futures trading and bond interest. My salary still dominates my income sources. As far as replacing salary with other income goes, you need to consider the joint picture with Moominmama's tax return below and the earnings of our superannuation accounts...

Increased deductions are mostly due to increased margin loan interest.

Franking credits (from Australian dividends), foreign tax paid, and the Early Stage Venture Capital (ESVCLP) offset are all deducted from gross tax to arrive at the tax assessment. Unlike in the past, I expect to pay a lot of extra tax.

Gross cash income deducts franking credits and adds the long-term capital gains discount to gross income. The former aren't paid out as cash and the latter are but aren't included in taxable income.

Net after tax cash income then deducts tax and deductions from gross cash income.

Moominmama's (formerly Snork Maiden) taxes follow:

Work related travel expenses were down to almost nothing, as the tax year started during our last big trip to conferences etc. I haven't yet managed to do the mortgage inversion that should increase deductions and so deductions are down.

As a result, income and taxes were up dramatically and we will owe a lot of tax. I expect we will have to start making quarterly tax payments from now on.

Trading Progress

I've now tested Bitcoin, ASX200, palladium, and crude oil futures trading using Barchart data. So far, only ASX200 futures were not profitable. I'm now trading one contract long or short of Bitcoin futures, trading palladium with position sizing using CFDs, and have put in an order to short crude oil futures.

With palladium I am aiming to risk about 10% of the CFD account on each trade. My current position is long 10 ounces of palladium and I have an order to short 20 ounces of palladium. The typical risk for trading a 100 ounce palladium futures contract is too big at this stage. The contract face value is around USD 160k. So, even if the stop is 5% from the current price you are risking USD 8000.

On the other hand, a crude oil contract has a face value of around USD 50k (1000 barrels of oil). I am targeting 5% of the face value as the risk we can take on. To compute the number of contracts we can trade we calculate: 0.05*price/abs(price-stop) and round it up or down to the nearest integer. If that is zero then we don't put an order in. This is why I only have a short order at the moment and no order to go long.

Both oil and palladium have longer optimal periods for measuring breakouts against than Bitcoin does. My palladium strategy looks for breakouts from the last seven days of prices in either direction. My oil strategy uses breakouts from the last eleven days. However, it will exit a long (short) position if the price falls below (rises above) the previous day's low (high).

Palladium has about the same risk/return trade off as Bitcoin, but oil isn't as good a risk/return ratio. Here are the average maximum potential loss and the average trade profit for trading with a single contract:

Bitcoin: Risk = USD 3,722, profit = USD 1,036, ratio = 0.28

Palladium: Risk = USD 4,910, profit = USD 1.462, ratio = 0.30

Crude oil: Risk = USD 2,030, profit = USD 225, ratio = 0.11

Compared to face value of the contract, the average Bitcoin profit is a 2.7% return, while for palladium and oil it is 0.9% and 0.4%, respectively. Relative to required margin, though, Bitcoin is not so good compared to the others.

The reason for trading all three of them at this stage is for diversification. I want to have more consistent returns rather than boom and bust. That's why I am still allocating the largest amount of risk to Bitcoin. I also still have a treasuries futures trade on and am long more than 100 ounces of gold via the IAU ETF.

At this point, I think I got beyond the experimental stage of trading and am now in a more developmental period. My backtesting programs work pretty well, I have good quality data, am more used to trading in a disciplined way, and am now testing which markets and position sizes make most sense.

With palladium I am aiming to risk about 10% of the CFD account on each trade. My current position is long 10 ounces of palladium and I have an order to short 20 ounces of palladium. The typical risk for trading a 100 ounce palladium futures contract is too big at this stage. The contract face value is around USD 160k. So, even if the stop is 5% from the current price you are risking USD 8000.

On the other hand, a crude oil contract has a face value of around USD 50k (1000 barrels of oil). I am targeting 5% of the face value as the risk we can take on. To compute the number of contracts we can trade we calculate: 0.05*price/abs(price-stop) and round it up or down to the nearest integer. If that is zero then we don't put an order in. This is why I only have a short order at the moment and no order to go long.

Both oil and palladium have longer optimal periods for measuring breakouts against than Bitcoin does. My palladium strategy looks for breakouts from the last seven days of prices in either direction. My oil strategy uses breakouts from the last eleven days. However, it will exit a long (short) position if the price falls below (rises above) the previous day's low (high).

Palladium has about the same risk/return trade off as Bitcoin, but oil isn't as good a risk/return ratio. Here are the average maximum potential loss and the average trade profit for trading with a single contract:

Bitcoin: Risk = USD 3,722, profit = USD 1,036, ratio = 0.28

Palladium: Risk = USD 4,910, profit = USD 1.462, ratio = 0.30

Crude oil: Risk = USD 2,030, profit = USD 225, ratio = 0.11

Compared to face value of the contract, the average Bitcoin profit is a 2.7% return, while for palladium and oil it is 0.9% and 0.4%, respectively. Relative to required margin, though, Bitcoin is not so good compared to the others.

The reason for trading all three of them at this stage is for diversification. I want to have more consistent returns rather than boom and bust. That's why I am still allocating the largest amount of risk to Bitcoin. I also still have a treasuries futures trade on and am long more than 100 ounces of gold via the IAU ETF.

At this point, I think I got beyond the experimental stage of trading and am now in a more developmental period. My backtesting programs work pretty well, I have good quality data, am more used to trading in a disciplined way, and am now testing which markets and position sizes make most sense.

Wednesday, October 02, 2019

September 2019 Report

In September the Australian Dollar fell from USD 0.6729 to USD 0.6752. The MSCI World Index rose 2.15% and the S&P 500 1.87%. The ASX 200 rose 2.08%. All these are total returns including dividends. We gained 0.52% in Australian Dollar terms and 0.87% in US Dollar terms. The target portfolio lost 0.28% in Australian Dollar terms and the HFRI hedge fund index lost 0.27% in US Dollar terms. So, though we under-performed all three stock indices we out-performed our target portfolio and the HFRI. Updating the monthly returns chart:

Here is a report on the performance of investments by asset class (futures includes managed futures and futures trading):

Things that worked well this month:

- Hedge funds shined as Platinum Capital, Regal, and Cadence gained significantly but Tribeca lost more money.

- Pengana Private Equity gained.

- Gold and Winton Global Alpha lost significantly, partly reversing recent gains.

- Tribeca lost as noted above.

The picture is better using the broader definition.

We moved a further towards our new long-run asset allocation.* Cash increased most and private equity and bonds decreased most as we received the proceeds from the IPE.AX delisting:

On a regular basis, we also invest AUD 2k monthly in a set of managed funds, and there are also retirement contributions. Then there are distributions from funds, dividends, and interest. Other moves this month:

- We sold $50k of Tenet Health Care bonds when they were called and $50k of Discovery Bonds matured. We bought $50k of HSBC bonds So, our direct bond holdings declined by $50k.

- We traded with moderate success, as discussed above.

- I bought a small number of Platinum Capital shares as their price was a lot below net asset value.

- We started buying Australian Dollars again, buying AUD 20k this month.

- We received the proceeds from the delisting of Oceania Capital.

- As a result of all this our cash holdings increased by around AUD 120k.

Saturday, September 28, 2019

ASX200 Futures

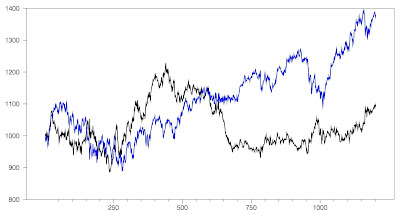

I put together a dataset for the ASX 200 futures for the past 5 years - Barchart have this data. Every possible "Turtle" strategy I tested lost money. So, we're definitely not going to trade this! I tested breakouts from 1 to 40 day periods and they all have similar poor performance. Position sizing to always trade the same percentage risk made things much worse.

Here is a 2,2 strategy without position sizing assuming no slippage – The best case scenario:

The blue line is the continuous futures contract price I constructed and black is the equity line of the strategy. This actually makes a slight gain over the 1200 trading days. But including reasonable slippage, it will turn into a loss. A 2,2 strategy means that you buy or sell breakouts from the previous two days highs or lows and exit those positions on breakouts from the same number of trading days in the opposite direction.

I have now put on a small (10 ounce) Palladium trade using CFDs. I'll probably test trading oil next.

Here is a 2,2 strategy without position sizing assuming no slippage – The best case scenario:

The blue line is the continuous futures contract price I constructed and black is the equity line of the strategy. This actually makes a slight gain over the 1200 trading days. But including reasonable slippage, it will turn into a loss. A 2,2 strategy means that you buy or sell breakouts from the previous two days highs or lows and exit those positions on breakouts from the same number of trading days in the opposite direction.

I have now put on a small (10 ounce) Palladium trade using CFDs. I'll probably test trading oil next.

Monday, September 23, 2019

Data Quality Matters

I did an analysis of the optimal trading strategy for Palladium futures using Barchart data. Previously, using free data, I had found that we should make trading decisions based on very short periods of past prices. For example we might go long (short) if prices broke out above (below) the previous day's high (low), or maybe the high or low of the previous two days. Now I find that the optimal strategies use periods of 7 to 18 days for breakouts. This shows that using good quality data really matters in trading, and not just a little bit. Using one day breakouts would actually lose money over the last five years of data that I tested. I lost money on all the Palladium trades I previously made... though four trades is not a large sample.

At the moment Palladium is in a winning long trade, but I am reluctant to go long at this point. So, I put in a short trade which will activate if the market reverses.

I also found out today that Barchart has past ASX 200 futures prices. I don't know if these are as high quality as their US futures data. I will download them next.

At the moment Palladium is in a winning long trade, but I am reluctant to go long at this point. So, I put in a short trade which will activate if the market reverses.

I also found out today that Barchart has past ASX 200 futures prices. I don't know if these are as high quality as their US futures data. I will download them next.

Sunday, September 15, 2019

Variable Position Size, Again

I signed up for the Barchart Premier subscription. Among other things, this gives access to daily open, high, low, close etc. data for all US based futures contracts back to 2000. The data seems to be much more accurate than the various free sources. To start with, I downloaded all Bitcoin futures contracts data. I constructed a continuous series of prices going back to the beginning of trading in Bitcoin futures. I use proportional splicing that preserves percentage changes rather than absolute dollar changes. I also saved the actual futures prices for computing trading costs.

When we include the very volatile period right after the all time high in Bitcoin, the optimal trading strategy changes:

This graph shows the drawdown for a simple strategy that always buys the same number of contracts (in red) with a strategy that always has the same initial risk in percentage terms (in green). The latter targets a constant maximum 5% potential loss of the face value of the Bitcoin contracts before stopping out. The simple strategy soon finds itself 40% down at the end of January 2018. On the other hand, it manages to claw back that loss by late March... The constant risk strategy only loses a maximum of 15% over this period. On the other hand it performed worse during the string of 11 losing trades in a row in late 2018. But the Sharpe ratio for the constant risk strategy (2.45) is quite a lot higher than for the constant position size strategy (2.21). So, I am going to start varying position size, targeting a maximum loss of USD 5,000.

I will also start to revisit other markets to see where there is potential.

Previously, I found that there was a positive relationship between the initial risk of a trade and its return. When volatility is low moves seem to be more noise than signal. Looking at the relationship between initial risk and return, there is now a negative correlation between them, though it isn't statistically significant:

On the other hand, the "lowest risk" trades here mostly had negative outcomes.

When we include the very volatile period right after the all time high in Bitcoin, the optimal trading strategy changes:

This graph shows the drawdown for a simple strategy that always buys the same number of contracts (in red) with a strategy that always has the same initial risk in percentage terms (in green). The latter targets a constant maximum 5% potential loss of the face value of the Bitcoin contracts before stopping out. The simple strategy soon finds itself 40% down at the end of January 2018. On the other hand, it manages to claw back that loss by late March... The constant risk strategy only loses a maximum of 15% over this period. On the other hand it performed worse during the string of 11 losing trades in a row in late 2018. But the Sharpe ratio for the constant risk strategy (2.45) is quite a lot higher than for the constant position size strategy (2.21). So, I am going to start varying position size, targeting a maximum loss of USD 5,000.

I will also start to revisit other markets to see where there is potential.

Previously, I found that there was a positive relationship between the initial risk of a trade and its return. When volatility is low moves seem to be more noise than signal. Looking at the relationship between initial risk and return, there is now a negative correlation between them, though it isn't statistically significant:

Wednesday, September 04, 2019

Individual Investment Returns, August 2019

Tuesday, September 03, 2019

August 2019 Report

Stock markets fell in August but we did OK in Australian Dollar terms and not so bad in US Dollar terms. The Australian Dollar fell from USD 0.6879 to USD 0.6729. The MSCI World Index fell 2.33% and the S&P 500 1.58%. The ASX 200 fell 2.05%. All these are total returns including dividends. We gained 0.93% in Australian Dollar terms and lost 1.27% in US Dollar terms. The target portfolio is expected to have gained 1.82% in Australian Dollar terms and the HFRI hedge fund index is expected to have lost 0.70% in US Dollar terms. So, we had a relatively strongly performing month, beating all three stock indices but under-performing our target portfolio and the HFRI. Updating the monthly returns chart:

Here is a report on the performance of investments by asset class (futures includes managed futures and futures trading):

Things that worked well this month:

- Gold gained 7.8%.

- The Winton Global Alpha Fund also did very well gaining 5.6%...

- I was impressed by the PSS(AP) balanced fund, which actually gained this month. But generally, diversified investments did well as bond performance outweighed the fall in stocks.

- Trading. Not including gold we lost 2.48%. Including gold it was a 2.18% gain for the month. Near the beginning of the month we had a big winning trade in Bitcoin, gaining USD 16k. We then gave it back in losing trades as the cryptocurrency chopped around. I have now reduced my position size in case this chop continues. The treasuries steepening trade also lost as the yield curve inverted more.

- Tribeca Global Resources Fund (TGF.AX) did horribly in terms of its share price. It's trading at quite a large discount. Cadence Capital (CDM.AX) returned to its position of being my worst investment ever in dollar terms, down AUD 20.6k cumulatively (AUD 3.2k this month).

- $25k of Scorpio Bulkers baby bonds matured slightly early, $25k of Hertz bonds were called, and $50k of Macquarie Bank bonds matured. I bought $50k of Energy Transfer bonds and $15k of Ford bonds. So, our direct bond holdings declined by $35k.

- We traded unsuccessfully, as discussed above.

- I opened a small position (10,000 shares) in URF, an Australian based REIT investing in US residential property, that was trading at a large discount to net asset value.

- I increased our holding of Domacom (DCL.AX) shares to 100k. It's still a very small position – 0.2% of net worth.

- I bought 1,000 more shares of the IAU gold ETF.

- I invested the inheritance of baby moomin. This reduced our cash and debt by the same amount as I was holding cash for this purpose but recording a loan from him in our accounts. Reported net worth does not include the net worth of our children, just my wife and I.

Sunday, August 25, 2019

Understanding Wills and Estate Planning

As we don't yet have a will, I have been reading this book, which is a simple guide to this topic with plenty of examples. I now see that there is more to estate planning in Australia than I thought. There are no inheritance taxes in Australia, so I thought that "estate planning" wasn't a big deal here. But after reading the book I now see that you might want to design things to prevent various scenarios occurring, and yes there are some tax issues, and then there are all the issues of making sure your wishes are carried out.

For example, in the case of my mother, after she lost the ability to make decisions, we ended up being dictated to by the government about how we managed her money etc. We had to sell all her financial assets and reinvest them in an approved way. We had a power of attorney to act on her behalf, but crazily this became invalid when she most needed us to act on her behalf! This was because prior to 2017 apparently you couldn't have an enduring power of attorney in her country. So, it is important to set up an enduring power of attorney.

I aspire that my children will inherit in real terms at least as much as I inherited from my parents. Of course, we can't guarantee this as who knows what might happen to the economy etc. But we can try to prevent some adverse events happening. An example is if one of us dies and the other gets a new partner. Then they die and the partner inherits everything and decides to give none of the money in their will to our children. Maybe because they have existing children and rewrite their will to include only them.... This kind of case is mentioned in the book but the solution isn't provided. On p58 it says that the survivor should see a lawyer before remarrying...

I am thinking the solution is to set up a testamentary trust on the death of the first spouse incorporating their share of the total assets. The beneficiaries would be the surviving spouse and the children. The surviving spouse will earn income from the trust during the remainder of their life after which the children will be the sole beneficiaries of the trust. So, clearly, we are going to need to discuss with a lawyer all of this.

Currently, if our nuclear family all died, it would be my mother-in-law who would inherit everything according to Australian law. I can't imagine she would handle that very well and given the large inheritance component from my parents, that hardly seems fair. So, we also need to have contingent inheritors to result in a more reasonable distribution of assets in that extreme case.

We also will need to think about who would be a guardian for our children if we both died. I can't really think of someone here in Australia that we would want to do this and who would agree to it as neither of us have relatives here. But it is something we are going to have to determine.

There are probably lots of things I still haven't considered but I think we are going to need to have rough ideas about all of these before meeting a lawyer. By the way, if anyone can recommend a lawyer that they have used, that would be great!

Sunday, August 18, 2019

Individual Investment Performance, July 2019

In July, generally alternative investments and small cap stocks did well and gold and our trading did poorly. Some things were just bouncing back from previous poor performance like Tribeca Global Natural Resources (TGF.AX) or Domacom (DCL.AX).

Monday, August 12, 2019

Trading Back on Track

After suffering some losses, it looks like I've got our trading back on track for the moment:

We were stopped out of Bitcoin this morning for a USD 16k gain at $11595 and $11600 in the August futures (3 contracts in total). As we are only doing long trades in Bitcoin, we don't have a Bitcoin position. This should be the impetus for subscribing to a data service and doing some backtesting of other markets...

We are also net positive in trading since 1996. However, the month is still not half-way over, so anything could happen by the end of the month.

We were stopped out of Bitcoin this morning for a USD 16k gain at $11595 and $11600 in the August futures (3 contracts in total). As we are only doing long trades in Bitcoin, we don't have a Bitcoin position. This should be the impetus for subscribing to a data service and doing some backtesting of other markets...

We are also net positive in trading since 1996. However, the month is still not half-way over, so anything could happen by the end of the month.

Sunday, August 04, 2019

Designing a Portfolio for Baby Moomin

I decided that the best provider of investment bonds is Generation Life. This is mainly because they seem to be scandal free, not about to be sold off to an overseas manager, and have lower fees than other providers. Next I needed to pick an investment portfolio from their investment options. I decided on the following rules and criteria:

50% Dimensional World Allocation 50/50 Trust. Here I compared a Vanguard balanced fund with this fund. In the long run, DFA have done much better than Vanguard:

Here, Portfolio 1 is a DFA stock fund and Portfolio 3 the Vanguard equivalent. The equity curves are for someone withdrawing 5% per year in retirement. Portfolio 2 is a DFA 60/40 stock/bond portfolio. The difference is stunning. Recently, DFA hasn't done as well as value stocks are out of favor. I am betting on them coming back. If there is a major market correction we might shift this core holding to a more aggressively equity focused fund.

Here, Portfolio 1 is a DFA stock fund and Portfolio 3 the Vanguard equivalent. The equity curves are for someone withdrawing 5% per year in retirement. Portfolio 2 is a DFA 60/40 stock/bond portfolio. The difference is stunning. Recently, DFA hasn't done as well as value stocks are out of favor. I am betting on them coming back. If there is a major market correction we might shift this core holding to a more aggressively equity focused fund.

10% Ellerston Australian Market Neutral Fund. Ellerston has done horribly in the past year, but prior to that it did very well for a market neutral fund. It now seems to be rebounding. This fund manager originally managed James Packer's money and then branched out.

10% Magellan Global Fund. This has been one of the best Australia based international equity funds. It did particularly well during the GFC.

10% Magellan Infrastructure Fund. This fund seems better than the other real estate options. It didn't do very well during the GFC, but all the others were worse.

10% Generation Life Tax Effective Australian Share Fund. This fund is managed by Redpoint Investments. The idea is to tilt a bit towards tax effective Australian shares given the high taxes on this investment bond overall. The manager is pretty much an index hugger, but the other options for actively managed Australian shares seem worse.

5% PIMCO Global Bond Fund. PIMCO is the gold standard for actively managed bonds. I decided to split my allocation to PIMCO between international bonds and

5% PIMCO Australian Bond Fund, as Australian bonds have actually done very well recently.

- 50/50 equities/fixed income and alternatives

- 50/50 passive and active management

- 50/50 Australian and international assets

- Pick the best fund from alternatives in each of these niches - focusing on long-term "alpha" and in particular their performance during the Global Financial Crisis and the recent December 2018 mini-crash.

50% Dimensional World Allocation 50/50 Trust. Here I compared a Vanguard balanced fund with this fund. In the long run, DFA have done much better than Vanguard:

10% Ellerston Australian Market Neutral Fund. Ellerston has done horribly in the past year, but prior to that it did very well for a market neutral fund. It now seems to be rebounding. This fund manager originally managed James Packer's money and then branched out.

10% Magellan Global Fund. This has been one of the best Australia based international equity funds. It did particularly well during the GFC.

10% Magellan Infrastructure Fund. This fund seems better than the other real estate options. It didn't do very well during the GFC, but all the others were worse.

10% Generation Life Tax Effective Australian Share Fund. This fund is managed by Redpoint Investments. The idea is to tilt a bit towards tax effective Australian shares given the high taxes on this investment bond overall. The manager is pretty much an index hugger, but the other options for actively managed Australian shares seem worse.

5% PIMCO Global Bond Fund. PIMCO is the gold standard for actively managed bonds. I decided to split my allocation to PIMCO between international bonds and

5% PIMCO Australian Bond Fund, as Australian bonds have actually done very well recently.

Friday, August 02, 2019

July 2019 Report

July was another positive month for long term investments, but we lost money trading.

In July the Australian Dollar fell from USD 0.7012 to USD 0.6879. The MSCI World Index rose 0.33% and the S&P 500 1.44%. The ASX 200 rose 2.94%. All these are total returns including dividends. We gained 2.25% in Australian Dollar terms and 0.31% in US Dollar terms. The target portfolio is expected to have gained 2.38% in Australian Dollar terms and the HFRI hedge fund index is expected to have gained only 0.10% in US Dollar terms. So, we had a relatively strongly performing month, almost a bit below the ASX200 and more or less matching our target portfolio and the MSCI and beating HFRI. Updating the monthly returns chart I posted last month :

Here is a report on the performance of investments by asset class (futures includes managed futures and futures trading):

Things that worked very well this month:

- Hedge funds, private equity, and Australian small cap all did well. I think this could be because many of these investments were not doing well and were probably sold to crystallize tax losses last month before the end of the Australian financial year and then rebought this month. The CFS Developing Companies Fund gained 5.86%.

- I marked Oceania Capital to $2.30 at the end of the month, which was the record date for the buyback associated with the delisting that was approved at the extra-ordinary meeting. The buyback price is $2.30 a share. This translated to a 7% gain for the month.

- The Winton Global Alpha Fund also did well gaining 2.46%. A big contrast to my own trading...

- We had major losses trading Bitcoin, though, so far, it is just a "correction". I closed short positions early which would have been winners. The Bitcoin "model" also suffered its worst percentage loss to date on a long trade. As I have been trading double the size long as short this just compounded the loss. Going forward I will only take long Bitcoin trades for the moment.

We moved a little more towards our new long-run asset allocation.* Gold and cash increased most and bonds decreased most:

- We tendered USD 40k of Avon Products bonds into an early redemption and sold USD 21k of Deutsche Bank bonds. Also, USD 50k of Citibank bonds matured. I bought USD 10k of Lexmark bonds, USD 25k of Kraft-Heinz bonds, and USD 25k of Dish bonds. So, our direct bond allocation fell by USD 51k.

- We traded unsuccessfully, as discussed above.

- I bought 1,000 more shares of the IAU gold ETF.

- I bought another 450 shares of Oceania Capital.

Subscribe to:

Posts (Atom)