The new net worth is $A553k. The previous high water mark in Australian Dollars was $A527k in August 2007, which was the month Snork Maiden and I merged finances in preparation to move to Australia. So in that sense we have finally recovered from the trauma of the GFC (and the costs of moving to Australia) but profit levels are very depressed and so in that sense we haven't recovered at all. It's mostly down to saving:

As you can see from both these graphs, non-retirement savings is the main driver. We also hit a new high in USD at $US586k. The previous high was $US574k in April last year. The income /expenditure accounts in US Dollars look like this:

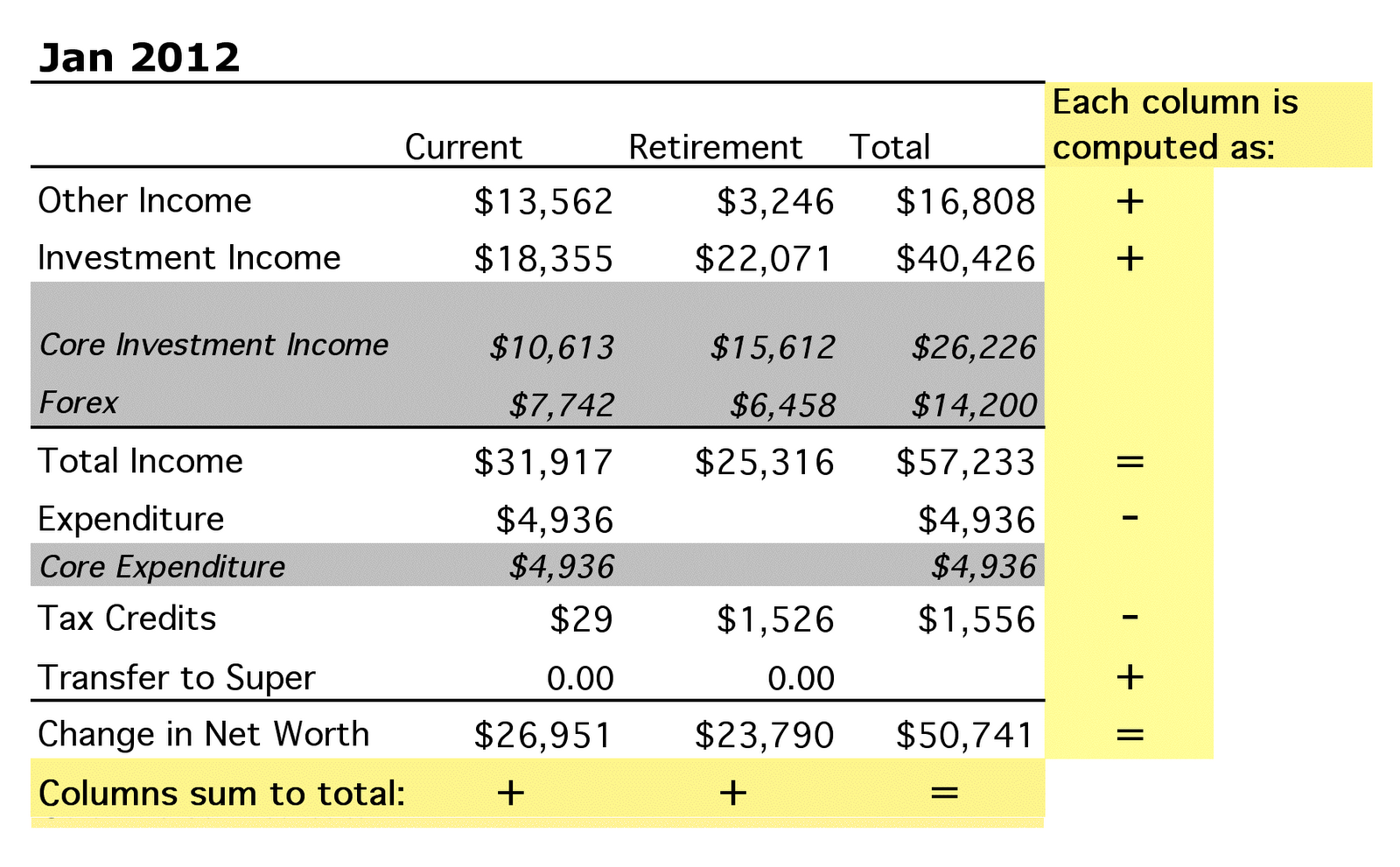

Investment income was high and the Australian Dollar gained to almost $US1.06. Expenditure was higher than last month but within recent norms. Net worth increased by $US50k ($A30k).

The MSCI World Index gained 5.84% in USD terms and the S&P500, 4.48%. We gained 7.55% in USD terms (4.05% in AUD terms and 4.90% in currency neutral terms). We reduced cash and net loans and the allocation to large cap Australian stocks increased most (to 44.76%) due to market performance. US stocks were our highest performing asset class.