In September the Australian Dollar fell from USD 0.6729 to USD 0.6752. The MSCI World Index rose 2.15% and the S&P 500 1.87%. The ASX 200 rose 2.08%. All these are total returns including dividends. We gained 0.52% in Australian Dollar terms and 0.87% in US Dollar terms. The target portfolio lost 0.28% in Australian Dollar terms and the HFRI hedge fund index lost 0.27% in US Dollar terms. So, though we under-performed all three stock indices we out-performed our target portfolio and the HFRI. Updating the monthly returns chart:

Here is a report on the performance of investments by asset class (futures includes managed futures and futures trading):

Things that worked well this month:

- Hedge funds shined as Platinum Capital, Regal, and Cadence gained significantly but Tribeca lost more money.

- Pengana Private Equity gained.

- Gold and Winton Global Alpha lost significantly, partly reversing recent gains.

- Tribeca lost as noted above.

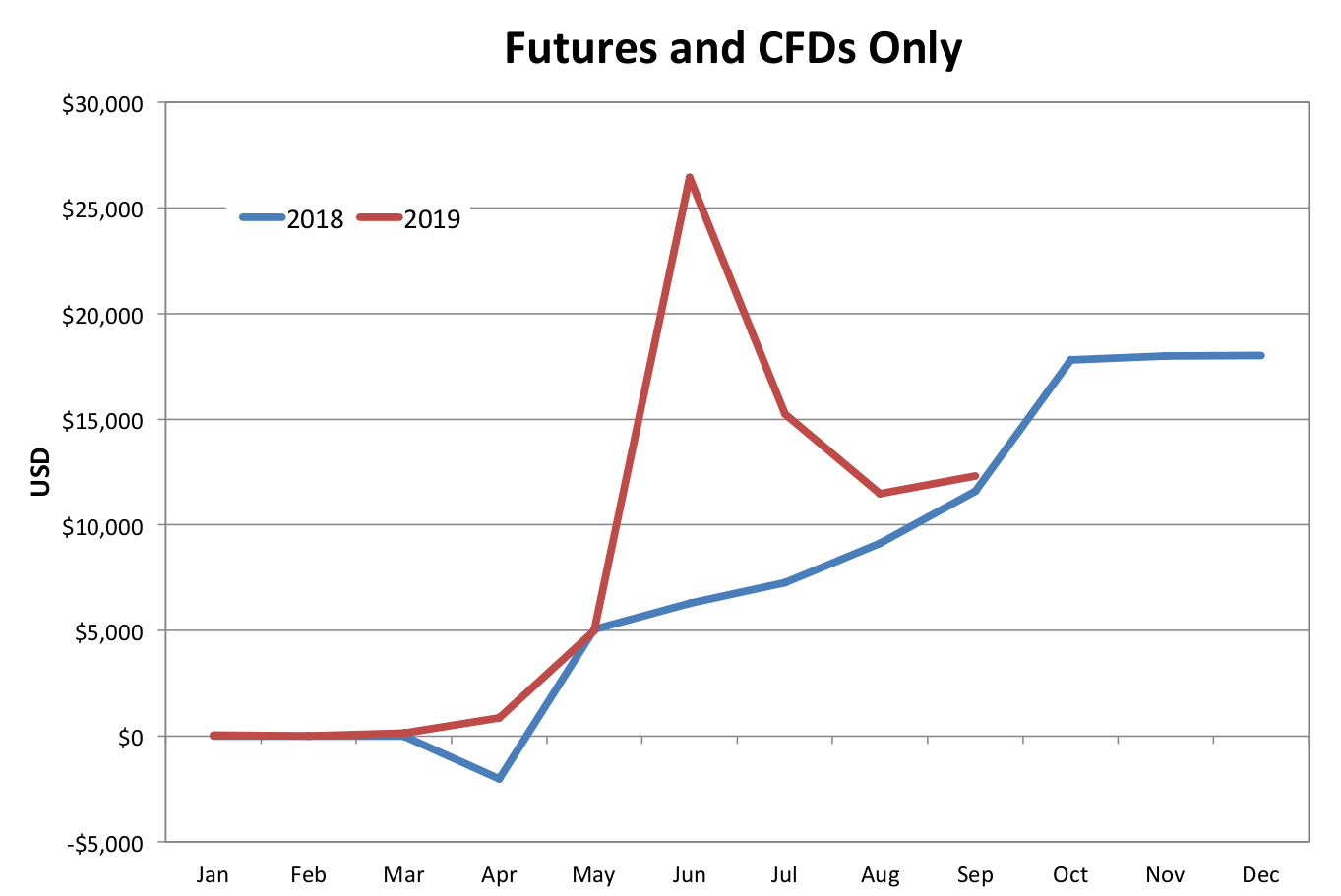

The picture is better using the broader definition.

We moved a further towards our new long-run asset allocation.* Cash increased most and private equity and bonds decreased most as we received the proceeds from the IPE.AX delisting:

On a regular basis, we also invest AUD 2k monthly in a set of managed funds, and there are also retirement contributions. Then there are distributions from funds, dividends, and interest. Other moves this month:

- We sold $50k of Tenet Health Care bonds when they were called and $50k of Discovery Bonds matured. We bought $50k of HSBC bonds So, our direct bond holdings declined by $50k.

- We traded with moderate success, as discussed above.

- I bought a small number of Platinum Capital shares as their price was a lot below net asset value.

- We started buying Australian Dollars again, buying AUD 20k this month.

- We received the proceeds from the delisting of Oceania Capital.

- As a result of all this our cash holdings increased by around AUD 120k.