BigChrisB sent me the ASX200 Accumulation Index data

he had collected and I have now measured my investment performance since 1996 (monthly data) against it and compared that to the other indices I've been tracking performance against:

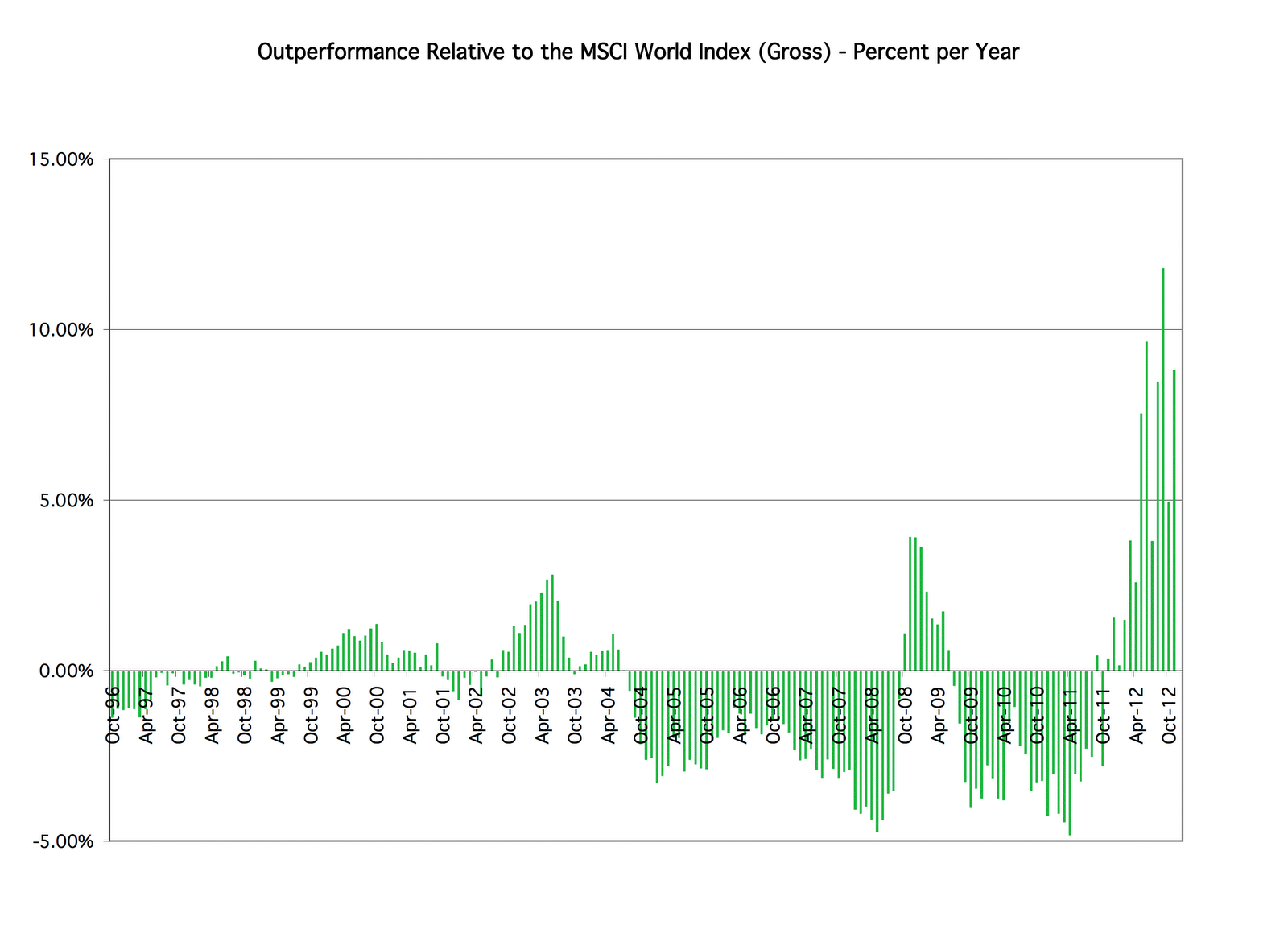

The table shows that you get very different performance figures depending on which index you benchmark against. First the MSCI World Index in USD terms and using the US risk free rate to do the standard CAPM regression analysis. In other words, I measure my investment returns in US Dollars too. Estimated beta is 1.23 - a 1% change in the index is associated with a 1.23% change in my portfolio. Alpha is 0.44% which means I am beating the index on a risk adjusted basis. My monthly percentage rate of return is most correlated with the returns of this index. R-Squared is 0.74 which means that 74% of the variation in my rate of return is explained by the changes in the index. Results are quite different when I measure my rate of return and that of the index in Australian Dollars. The R-Squared is only 0.39, beta is much lower, and alpha is a little negative. Switching back to US Dollars my correlation with the S&P 500 is worse than with the MSCI but I underperformed the index by 1.6% per year, risk adjusted. Finally, in comparison to the Australian ASX 200 index and measuring things in Australian Dollars I underperformed by 3.89% a year, beta is 0.89 and R-Squared is 0.51. The ASX has been a fantastic performer over this period of time:

This explains why I benchmark against the MSCI in USD terms even though I live in Australia.

The table shows that you get very different performance figures depending on which index you benchmark against. First the MSCI World Index in USD terms and using the US risk free rate to do the standard CAPM regression analysis. In other words, I measure my investment returns in US Dollars too. Estimated beta is 1.23 - a 1% change in the index is associated with a 1.23% change in my portfolio. Alpha is 0.44% which means I am beating the index on a risk adjusted basis. My monthly percentage rate of return is most correlated with the returns of this index. R-Squared is 0.74 which means that 74% of the variation in my rate of return is explained by the changes in the index. Results are quite different when I measure my rate of return and that of the index in Australian Dollars. The R-Squared is only 0.39, beta is much lower, and alpha is a little negative. Switching back to US Dollars my correlation with the S&P 500 is worse than with the MSCI but I underperformed the index by 1.6% per year, risk adjusted. Finally, in comparison to the Australian ASX 200 index and measuring things in Australian Dollars I underperformed by 3.89% a year, beta is 0.89 and R-Squared is 0.51. The ASX has been a fantastic performer over this period of time:

This explains why I benchmark against the MSCI in USD terms even though I live in Australia.