This month we spent a lot of money. We went on vacation to Singapore - our first trip overseas with little Moomin. Since last year there are now direct flights between our city and there - one of two international destinations now available on direct flights. I think next time we will go to the other country where the weather is much more to my liking, at least in the summer. The trip ended up costing a lot more than expected...

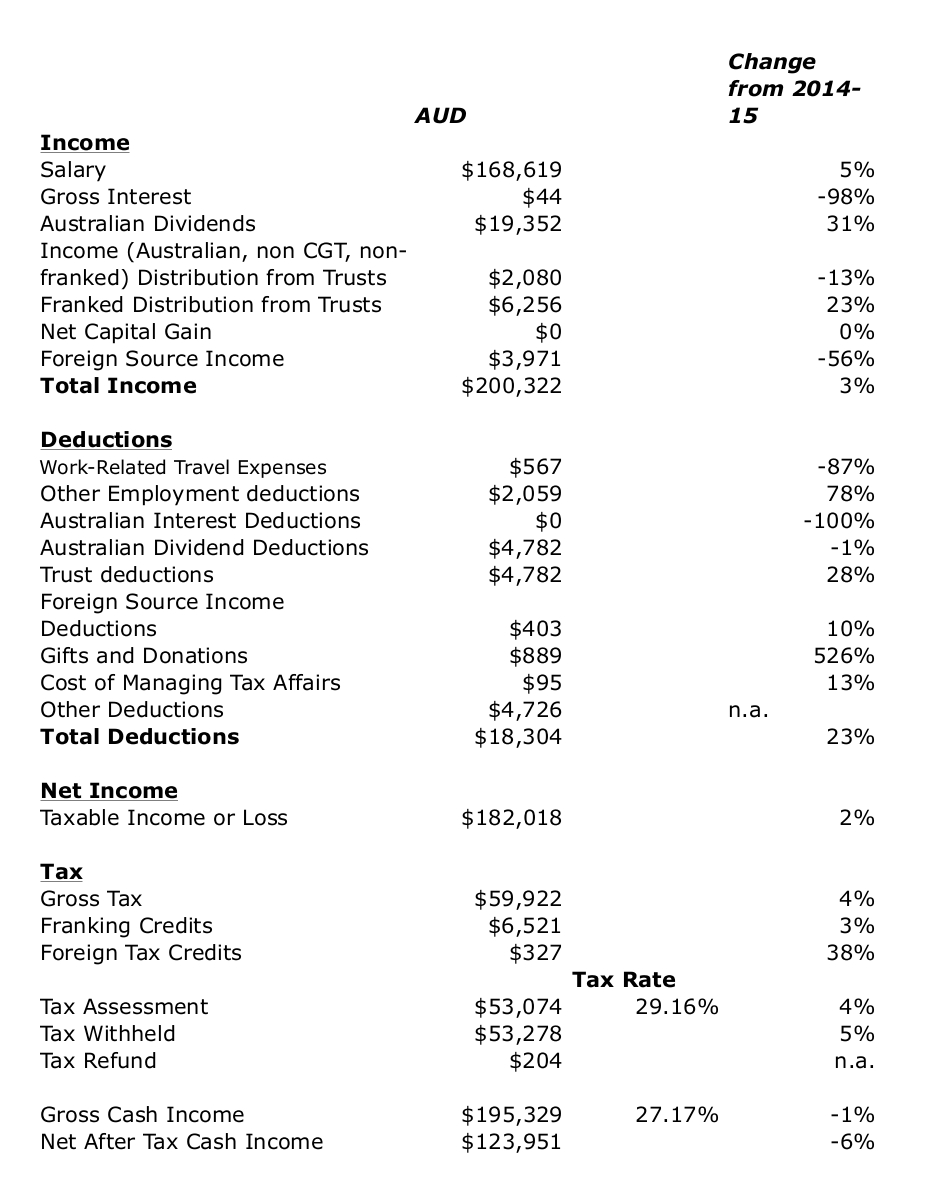

This month's accounts are very preliminary as they include estimates of franking (tax) credits on managed funds ($3.9k) that we won't actually know till the end of July. Here are our monthly accounts (in AUD):

"Current other income", which is mainly salaries, was a bit higher than usual at $14.8k. Spending (not counting mortgage) was very high at $10.9k. After deducting the mortgage payment of $5.5k (which includes

implicit interest saving due to our offset account - the actual mortgage payment was about $698 less than this) - there were three mortgage payments this month rather than the usual two - we dissaved $1.5k on the current account and added $3.5k in added housing equity. Retirement contributions were quite high at $5.1k as I got three retirement contributions this month. Net saving was, therefore, $7.1k across the board.

"Current other income", which is mainly salaries, was a bit higher than usual at $14.8k. Spending (not counting mortgage) was very high at $10.9k. After deducting the mortgage payment of $5.5k (which includes

implicit interest saving due to our offset account - the actual mortgage payment was about $698 less than this) - there were three mortgage payments this month rather than the usual two - we dissaved $1.5k on the current account and added $3.5k in added housing equity. Retirement contributions were quite high at $5.1k as I got three retirement contributions this month. Net saving was, therefore, $7.1k across the board.

From next month I will stop my voluntary retirement contributions of $100 a week due to the reduction in the concessional contribution cap from $35k a year to $25k a year. My employer contributions will actually exceed the cap. As is usual in the public sector they are much higher than the 9.5% compulsory contributions. The excess will just be taxed at my marginal rate like a non-concessional contribution. I might still add some non-concessional contributions to superannuation in a few years time but don't feel like locking up more money than necessary when there is no immediate tax advantage and the rules on taxation in the retirement phase, could change at any time...

The Australian Dollar rose from USD 0.7437 to USD 0.7681. The ASX 200 rose by 0.17%, the MSCI World Index gained 0.50%, and the S&P 500 0.62%. We gained 0.38% in Australian Dollar terms and 3.68% in US Dollar terms. So, unusually we outperformed both the Australian and international markets. The best performer in dollar terms was CFS Geared Share Fund up $5.6k. Next best was Platinum Capital, gaining $3.0k across our various different holdings. The worst performer was PSSAP superannuation fund, losing $0.8k. Small cap Australian stocks was the best performing asset class in percentage terms, followed by hedge funds. All other asset classes gained apart from commodities and real estate.

As a result of all this, net worth rose AUD 9k to $1.839 million (new high) or rose USD 51k to USD 1.413 million (also a new high).

30th June is the end of the Australian financial year. Over the last 12 months we had a rate of return of 13.7% in AUD terms (17.5% in USD terms). The ASX200 gained 14.1%, while the MSCI gained 19.4% in USD terms. Net worth increased AUD 262k and we are still on track to get close to the optimistic projection for 2017. Of course, anything could happen in the next 6 months!

This month's accounts are very preliminary as they include estimates of franking (tax) credits on managed funds ($3.9k) that we won't actually know till the end of July. Here are our monthly accounts (in AUD):

From next month I will stop my voluntary retirement contributions of $100 a week due to the reduction in the concessional contribution cap from $35k a year to $25k a year. My employer contributions will actually exceed the cap. As is usual in the public sector they are much higher than the 9.5% compulsory contributions. The excess will just be taxed at my marginal rate like a non-concessional contribution. I might still add some non-concessional contributions to superannuation in a few years time but don't feel like locking up more money than necessary when there is no immediate tax advantage and the rules on taxation in the retirement phase, could change at any time...

The Australian Dollar rose from USD 0.7437 to USD 0.7681. The ASX 200 rose by 0.17%, the MSCI World Index gained 0.50%, and the S&P 500 0.62%. We gained 0.38% in Australian Dollar terms and 3.68% in US Dollar terms. So, unusually we outperformed both the Australian and international markets. The best performer in dollar terms was CFS Geared Share Fund up $5.6k. Next best was Platinum Capital, gaining $3.0k across our various different holdings. The worst performer was PSSAP superannuation fund, losing $0.8k. Small cap Australian stocks was the best performing asset class in percentage terms, followed by hedge funds. All other asset classes gained apart from commodities and real estate.

As a result of all this, net worth rose AUD 9k to $1.839 million (new high) or rose USD 51k to USD 1.413 million (also a new high).

30th June is the end of the Australian financial year. Over the last 12 months we had a rate of return of 13.7% in AUD terms (17.5% in USD terms). The ASX200 gained 14.1%, while the MSCI gained 19.4% in USD terms. Net worth increased AUD 262k and we are still on track to get close to the optimistic projection for 2017. Of course, anything could happen in the next 6 months!