Doing the accounts for March this morning... Looks like we hit a net worth of $A600k for the first time, partly because of the fall in the Australian Dollar to $US1.03 this month. But I'm noticing that quite a lot of our investments are hitting all time highs in terms of the profit we have made on them. These are:

CFS Developing Companies Fund

CFS Diversified Fund

PSS(AP) (Snork Maiden's superannuation fund)

Qantas

Celeste Australian Small Companies

Acadian Global Equity Long-Short

Argo Investments

CFS Geared Global Share Fund

Some others are also quite close to peak profit levels. Of course a lot of other investments are still way down from their peak profit level or are underwater... Two common themes among the winners are small cap stock funds and recent investments. Small caps have been doing very well - they usually do at the beginning of the business cycle, which is why we have invested in them quite heavily. Recent investments haven't yet had a chance to lose money :)

Our house-buying fund has reached $A82,973 from $A77,386 last month. The goal is to reach around $A100k.

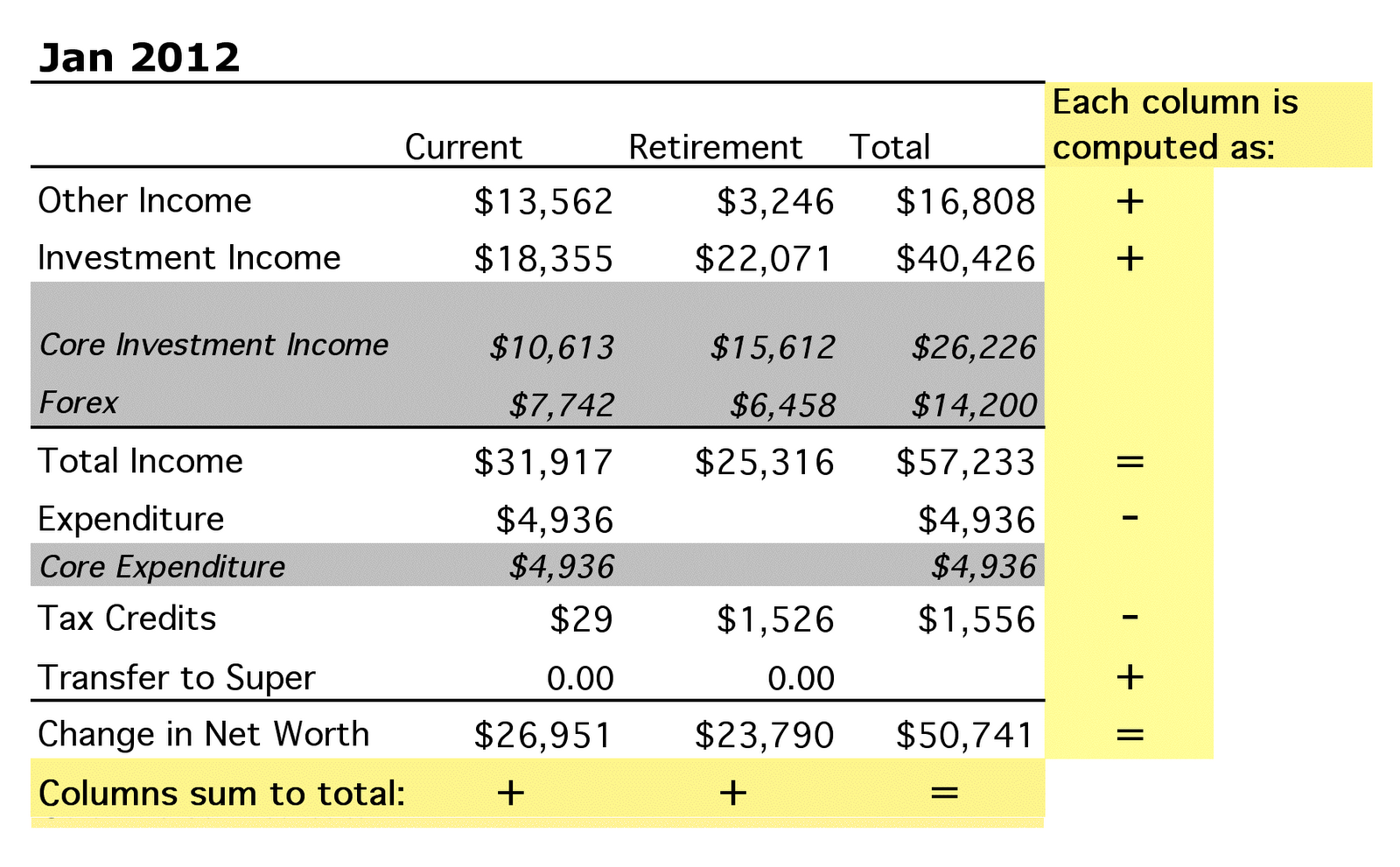

Apart from computing rates of return, I use the monthly accounting to check up on whether all our retirement contributions have been properly made by our employers, whether the fees we are being charged are correct, and whether we have been paid money we are owed. I found that my superannuation provider has been charging around $A100 a month for "inbuilt benefits"

since I cut my member contribution to zero in September. This makes no sense to me as there is nothing in the prospectus (PDS) about increased fees if you cut your contributions. It does say that you can't get optional life insurance etc. and in fact the fund refused me the

coverage, which I tried to get. So I think they are now charging me for coverage that I don't have. I sent them an e-mail querying this...

Anyway this is how our Australian superannuation accounts are doing:

The green line is Snork Maiden's account and the blue line my current account, both of which we are contributing to. The red is my account from when I worked in Australia previously. I rolled it over into a commercial fund manager and it is invested rather riskily. Hence the big fluctuations. We have now managed to save $100k in our new super accounts.

I'm also still owed money for travel to a conference back last November, and for

consulting over the last six months. In the latter case, government budget cuts and local circumstances look like I lost the gig now (right after

my security clearance was finally approved at the end of February, but it would be nice to get paid for what I already did! The conference money is also owed by another university. My own employer is actually great at reimbursing money. I submitted a bill for our recent overseas trip this Tuesday and already the money was in my account on Friday!