I blogged recently about the proposed merger between the Australian Unity Diversified Property Fund and a Cromwell office fund. Today, I was called by a representative who told me about the plan and timeline and asked if I had questions and whether I would support the proposal So, I told him that I understood the reasons for seeking a merger and that I thought this merger was better than previous proposal but also that I invested in the fund to get exposure to a diversified portfolio and now it was going to be a office dominated fund, a sector that's not doing too well. So, I wasn't really sure which way to vote. He sounded disappointed and said he understood my thinking...

Wednesday, July 26, 2023

Got a Call from Australian Unity

Thursday, July 13, 2023

New Australian Unity Merger Proposal

Australian Unity Diversified Property Fun has a new merger proposal on the table following the failed merger in 2021-22. This is a merger with the unlisted Cromwell Direct Property Fund. This seems like a fair deal unlike the previous one. It has various advantages. The only downside is that the merged fund will have 70% of its assets in offices. The attraction of AUDPF was that it was truly diversified and not dominated by offices.

I expect I will stay in the fund (there is only a limited near term opportunity to withdraw) and think about withdrawing in 2025 when a full liquidity event is promised. The main risk is that office properties are downvalued in 2024 and 2025 after the merger happens. I am seeing a decline in value in the TIAA Real Estate Fund even though only a quarter of their assets are in offices. I reduced my holdings near peak value, should have reduced them more. So, maybe I should try to withdraw some of our investment when allowed later this year...

Sunday, July 09, 2023

Spending 2022-23

For the last six years I've been putting together reports on our spending over the Australian financial year, which runs from 1 July to 30 June. This makes it easy to do a break down of gross income including taxes that's comparable to many you'll see online, though all our numbers are in Australian Dollars. At the top level we can break down total income (as reported in our tax returns plus superannuation contributions) into the following categories of spending:

The gross income for this year (bottom line) is just an estimate. It is based on the gross income we expect to report in our tax returns (before investment expenses etc) plus employer superannuation contributions. Tax includes local property tax as well as income tax and tax on superannuation contributions. Investing costs include margin interest. Mortgage interest is included in spending, while mortgage principal payments are considered as saving. Spending also includes the insurance premia paid through our superannuation. Current saving is then what is left over. This is much bigger than saving out of salaries because gross income includes investment returns reported in our tax returns. The latter number depends on capital gains reported for tax purposes, so is fairly arbitrary. Spending increased substantially, though we also expect income to hit a high though it's been fairly constant over the last five years. Graphically, it looks like this:

We break down spending into quite detailed categories. Some of these are then aggregated up into broader categories:

Our biggest spending category, if we don't count tax, is now childcare and education, which continues to trend upwards. As mentioned above, the income and tax numbers are all estimates. Commentary on each category follows:

Employer superannuation contributions: These include employer contributions (we don't do any salary sacrifice contributions) but not concessional contributions we paid to the SMSF this year.

Superannuation contributions tax: The 15% tax on concessional superannuation contributions. This includes tax on our concessional contributions to the SMSF.

Franking credits: Income reported on our tax returns includes franking credits (tax paid by companies we invest in). We need to deduct this money which we don't receive as cash but is included in gross income. Foreign tax paid is the same story.

Income tax is one category that has fallen since 2017-18!

Life and disability insurance: I have been trying to bring this under control and the amount paid has also fallen since 2017-18 a result.

Health: Includes health insurance and direct spending. Spending peaked with the birth of our second child. It is up this year because I had an operation early this calendar year.

Housing: Includes mortgage interest, maintenance, and body corporate fees (condo association). Rising interest rates have pushed up spending this year.

Transport: About half is spending on our car and half is my spending on Uber, e-scooters, buses etc.

Utilities: This includes water, gas, electricity, telephone, internet, and online storage etc.

Subscriptions: This is a new category this year, split out from utilities. It's been trending up strongly.

Supermarkets: Includes convenience stores, liquor stores etc as well as supermarkets. Seems crazy that it has almost doubled in five years and is now our third biggest spending category.

Restaurants: This was low in 2017-18 because we spent a lot of cash at restaurants. It was low in the last two years because of the pandemic but doubled this year as life got more back to normal and prices are climbing I feel particularly in this area.

Cash spending: This has collapsed to almost zero. I try not to use cash so that I can track spending. Moominmama also gets some cash out at supermarkets that is included in that category.

Department stores: All other stores selling goods that aren't supermarkets. No real trend here.

Mail order: This seems to have leveled out in the last three years and actually came down this year,

Childcare and education: We are paying for private school for one child, full time daycare for the other, plus music classes, swimming classes...

Travel: This includes flights, hotels etc. It was very high in 2017-18 when we went to Europe and Japan. In 2020-21 it was down to zero due to the pandemic and having a small child. This year we went to Sydney for a week and this is mostly how much the accommodation cost.

Charity: Not sure why this is trending down.

Other: This is mostly other services. It includes everything from haircuts to professional photography.

This year's increased spending was mainly driven by increased childcare and education costs and higher mortgage interest. I expect education to fall a little next year as private primary school is cheaper than daycare.

Monday, June 12, 2023

What I Get Out of Tracking Spending Categories

Ramit Sethi advocates only tracking about four categories of spending and is critical of couples who do more fine-grained tracking. For the last few years I have been tracking 15 top level spending categories and 27 more detailed spending categories. So, what do I get out of this. I think the following:

- I can track which items have grown fast and maybe we should cut back on. This has resulted in saving money on car insurance, health insurance, and mortgage interest.

- Some things that I think we are spending a lot on, and should cut back on are actually not that big. For example, our current spending on restaurants is AUD 3k per year or 1.7%. My spending on bus, Uber, taxis etc. is AUD 4.5k per year or 2.5%, which is less than half our spending on transport. These are two of my three areas of "luxury" or personal spending. The other is spending money on subscriptions online etc So, being able to see these numbers makes me feel more comfortable about my spending in these areas.

- Perhaps some things seem small and we can consider raising them, like our spending on charity at only 0.4%.

- Well, yes it's neat to see what we are spending money on and comparing to other people :)

Sunday, June 11, 2023

May 2023 Report

In May, markets were mixed. The MSCI World Index (USD gross) fell 1.00% while the S&P 500 rose 0.43% in USD terms. The ASX 200 fell 2.30% in AUD terms. All these are total returns including dividends. The Australian Dollar fell from USD 0.6605 to USD 0.6479. We lost 1.07% in Australian Dollar terms or lost 3.09% in US Dollar terms. The target portfolio lost 0.06% in Australian Dollar terms and the HFRI hedge fund index is expected to lose 0.12% in US Dollar terms. So, we under-performed all benchmarks apart from the ASX 200.

Here is a report on the performance of investments by asset class:

The asset class returns are in currency neutral returns as the rate of return on gross assets. I then add in the contributions of leverage and other costs and the Australian Dollar to the AUD net worth return. We underperformed the target portfolio benchmark mainly because of negative returns on hedge funds in particular. Private equity had the most positive returns and contributed most to the return for the month, while gold and futures also performed positively. Australian small caps were the worst performers.

Things that worked well this month:

- 3i (III.L) gained the most (AUD 18k) followed by Cordish Dixon PE Fund 3 (CD3, 8k), and Winton Global Alpha (7k).

What really didn't work:

- Cadence Capital (CDM.AX), Regal Funds (RF1.AX), and Cadence Opportunities (CDO.AX) lost the most: AUD 18k, 13k, and 11k respectively.

The investment performance statistics for the last five years are:

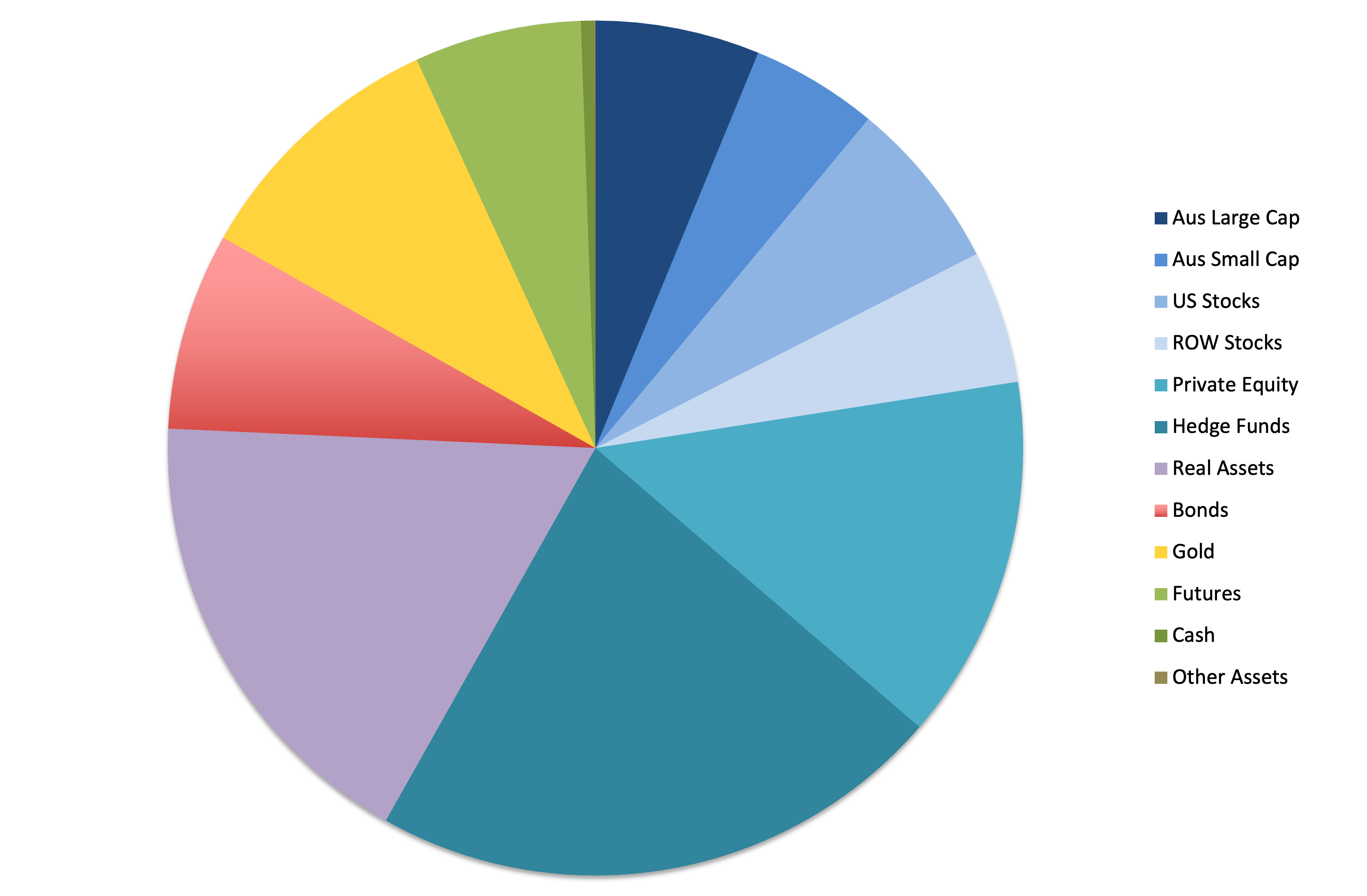

We are now very close to our target allocation. Our actual allocation currently looks like this:

We receive employer contributions to superannuation every two weeks. We are now contributing USD 10k each quarter to Unpopular Ventures Rolling Fund and less frequently there will be capital calls from Aura Venture Fund II. It was a very quiet month. The only additional investment move I made was:

- I bought a net 250 shares of PMGOLD.AX.

Friday, June 09, 2023

Fixed My Margin Loan Interest Rate

I fixed my margin loan interest rate for the next year at 7.69% instead of a variable rate 9.15%. I am paying the interest in arrears. At the moment I can't see the RBA really cutting interest rates by an average of 1.5% over the next year. It's the first time I have done this. One reason for that is that my balance is relatively low at the moment and I expect it will increase, so I won't have the problem of early termination. I am withdrawing AUD 15k every quarter to invest in the Unpopular Ventures Rolling Fund.

Saturday, May 06, 2023

April 2023 Report

In April, stock markets continued to rise. The MSCI World Index (USD gross) rose 1.48% and the S&P 500 1.56% in USD terms, while the ASX 200 gained 2.03% in AUD terms. All these are total returns including dividends. The Australian Dollar fell from USD 0.6695 to USD 0.6605. We gained 1.09% in Australian Dollar terms but lost 0.45% in US Dollar terms. The target portfolio gained 1.98% in Australian Dollar terms and the HFRI hedge fund index is expected to gain 1.19% in US Dollar terms. So, we under-performed all benchmarks :(

Here is a report on the performance of investments by asset class:

Several asset classes made moderate positive contributions with private equity leading, while ROW stocks and hedge funds had negative returns

Things that worked well this month:

- Gold was the greatest gainer at AUD 9k, but several other investments gained between AUD 6-9k including Unisuper, 3i (III.L), Hearts and Minds (HM1.AX), Regal Funds (RF1.AX), Winton Global Alpha, WAM Alternatives (WMA.AX), and PSS(AP).

What really didn't work:

- Tribeca Global Resources (TGF.AX) was again the biggest loser with a loss of AUD 14k. Followers up were: The China Fund (CHN, -8k) and Pershing Square Holdings (PSH.L, -6k).

The investment performance statistics for the last five years are:

We are now very close to our target allocation. Our actual allocation currently looks like this:

We receive employer contributions to superannuation every two weeks. We are now contributing USD 10k each quarter to Unpopular Ventures Rolling Fund and less frequently there will be capital calls from Aura Venture Fund II. In addition, we made the following investment moves this month:

- I invested USD 2,500 in a Latin-American start-up company through the Unpopular Venture Syndicate.

- I bought 5,000 more Cordish-Dixon 3 (CD3.AX) shares.

Thursday, May 04, 2023

Moominmama's Manager Made the Whole Thing Up!

So, Moominmama talked to HR about the "voluntary redundancy". They said that there was no restructuring in progress and she would only be considered for voluntary redundancy if she literally volunteered and that basically her manager just made the whole thing up! This sounds like real incompetence or professional malpractice on his part.

Thursday, April 27, 2023

Redundancy Package

Moominmama was offered a redundancy package. Seems a bit like an offer you can't refuse. When she asked if she would be fired anyway if she rejected it, her boss told her he couldn't tell her that... We don't know the details of the package yet. Her lower level manager said that as she is only working two days a week it's hard to involve her in projects or for them to take on projects that need her skills because she doesn't work enough. But she wants to take the package and doesn't want to work more days.

She plans to reduce the daycare days of our almost 4 year old for the second half of this year. After that he should be in full time pre-school.

I ran a simulation and through the end of 2024 the effect is a reduction in net worth of about AUD35k before considering the value of the package and after considering the likely value of the package it is about even. After that the effect gets progressively larger, but, surprisingly, in the long run (2029 and 2044) net worth is around 2% lower than in the base case. This is in contrast to the scary numbers that we are currently spending AUD 177k per year and my after tax salary is AUD 130k.

I feel like I must have done something wrong in the simulation.

Sunday, April 09, 2023

March 2023 Report

In March, stock markets rebounded. The MSCI World Index (USD gross) rose 3.15% and the S&P 500 3.67% in USD terms, while the ASX 200 only gained 0.25% in AUD terms. All these are total returns including dividends. The Australian Dollar fell from USD 0.6740 to USD 0.6695. We gained 0.55% in Australian Dollar terms but lost 0.15% in US Dollar terms. The target portfolio gained 1.84% in Australian Dollar terms and the HFRI hedge fund index is expected to gain 1.47% in US Dollar terms. So, we only out-performed the ASX200.

Here is a report on the performance of investments by asset class:

Gold was the main positive contributor to returns and the highest returning asset class while futures were the largest detractor and worst performing asset class. The trend-following managed futures funds got caught in the sudden movement in US bonds during the month associated with the banking crisis.

Things that worked well this month:

- Gold gained AUD 54k - the biggest monthly gain in a single investment since I started investing.

What really didn't work:

- Tribeca Global Resources (TGF.AX) lost AUD 11k. Followers up were: Pershing Square Holdings (PSH.L, -10k), Aspect Diversified Futures (-9k), Hearts and Minds (HM1.AX, -9k), and Winton Global Alpha (-8k).

The investment performance statistics for the last five years are:

We are now very close to our target allocation but we mived away from it quite sharply during the month. In particular, real assets increased as we added to URF.AX and it rose, while private equity fell as we took profits in PE1.AX. Our actual allocation currently looks like this:

We receive employer contributions to superannuation every two weeks. We are now contributing USD 10k each quarter to Unpopular Ventures Rolling Fund and less frequently there will be capital calls from Aura Venture Fund II. In addition, we made the following investment moves this month:

- I sold 100 China Fund (CHN) shares.

- I sold 3,500 WAM Leaders (WLE.AX) shares.

- I sold 10k MCP Income Opportunities (MOT.AX) when the price spiked back up to AUD 2.10.

- I bought 12k shares net of Cordish-Dixon Private Equity Fund 3 (CD3.AX).

- I did a losing trade in bond futures.

Friday, March 31, 2023

Comments Stuck in Moderation

I just found that a lot of comments people made in the past were stuck in moderation. I didn't know "sometimes moderation" was on. I approved all the substantive comments and turned moderation off. I apologize to everyone who commented but whose comment wasn't published up till now. I really appreciate all the comments. They made me feel less lonely on this journey.

Monday, March 27, 2023

Yield Curve Trade

I entered a new yield curve trade - betting on a reduction in the inversion:

This executed by buying a spread that is long two year treasuries futures and short ten year treasuries futures. If we have a repeat of the late 1970s and early 1980s it will lose but inflation was much higher than now then. Last time I tried this in late 2019 to early 2020 I lost about USD 1,500. I was right but too early.

31 March

The trade went badly right from the start and it started making me more and more anxious. I didn't sleep last night and couldn't get to sleep tonight, so I closed the trade. But I still can't sleep yet. So, thought writing this update might help. I would have thought that I had learnt my lesson that I can't cope with overnight futures trades where I could decide to change the trade. It's just not something I can do. I had planned to do some more work on trading in the next few months, but now think I shouldn't do it.

Sunday, March 05, 2023

February 2022 Report

In February, stock markets fell again. The MSCI World Index (USD gross) fell 2.83% and the S&P 500 2.44% in USD terms, while the ASX 200 lost 2.25% in AUD terms. All these are total returns including dividends. The Australian Dollar fell from USD 0.7113 to USD 0.6740. We also lost money: 0.47% in Australian Dollar terms or 5.69% in US Dollar terms. The target portfolio gained 0.72% in Australian Dollar terms and the HFRI hedge fund index is expected to lose about 0.83% in US Dollar terms. So, we out-performed the ASX200 but under-performed all the other benchmarks.

Here is a report on the performance of investments by asset class:

Real assets were the main positive contributor to returns and the highest returning asset class while hedge funds were the largest detractor.

Things that worked well this month:

- URF.AX (US residential real estate) was the biggest gainer adding AUD 11k, followed by two managed futures funds: Winton Global Alpha (9k) and Aspect Diversified Futures (6k).

What really didn't work:

- Tribeca Global Resources (TGF.AX) lost AUD 30k. The next worse were the China Fund (CHN, -19k) and Australian Dollar Futures (-15k).

The investment performance statistics for the last five years are:

We are now very close to our target allocation but we mived away from it quite sharply during the month. In particular, real assets increased as we added to URF.AX and it rose, while private equity fell as we took profits in PE1.AX. Our actual allocation currently looks like this:

About 70% of our portfolio is in what are often considered to be alternative assets: real estate, art, hedge funds, private equity, gold, and futures. A lot of these are listed investments or investments with daily, monthly, or quarterly liquidity, so our portfolio is not as illiquid as you might think.

We receive employer contributions to superannuation every two weeks. We are now contributing USD 10k each quarter to Unpopular Ventures Rolling Fund and less frequently there will be capital calls from Aura Venture Fund II. In addition, we made the following investment moves this month:

- I bought 1,000 shares of the gold ETF, PMGOLD.AX.

- I sold 4,000 shares of WAM Leaders (WLE.AX).

- I sold 59,976 shares of Pengana Private Equity (PE1.AX).

- I bought 29,638 shares of the Cordish-Dixon private equity fund CD3.AX.

- I bought 25,000 shares of MCP Income Opportunities private credit fund (MOT.AX).

- I bought 65,000 shares of URF.AX (US residential real estate).

Wednesday, March 01, 2023

January 2022 Report

In January, stock markets rebounded. The MSCI World Index (USD gross) gained 7.19% and the S&P 500 6.28% in USD terms, and the ASX 200 gained 6.23% in AUD terms. All these are total returns including dividends. The Australian Dollar rose from USD 0.6816 to USD 0.7113. We gained 2.21% in Australian Dollar terms or 6.66% in US Dollar terms. The target portfolio rose 1.45% in Australian Dollar terms and the HFRI hedge fund index around 2.8% in US Dollar terms. So, we out-performed the S&P 500, the HFRI, and our target portfolio and under-performed the others.

Here is a report on the performance of investments by asset class:

The asset class returns are in currency neutral returns as the rate of return on gross assets. I have added in the contributions of leverage and other costs and the Australian Dollar to the AUD net worth return.

All asset classes had positive returns. Private equity was the largest contributor to returns Followed by hedge funds, while RoW stocks had the highest return.

Things that worked well this month:

- 3i (III.L) rose strongly, gaining AUD 22k. Tribeca (TGF.AX 18k), Unisuper (15k), PSSAP (14k), China Fund (CHN, 13k), and Hearts and Minds (HM1, 10k) all contributed more than AUD 10k.

What really didn't work:

- Three managed futures funds all lost money, with Winton Global Alpha losing the most (AUD 4k).

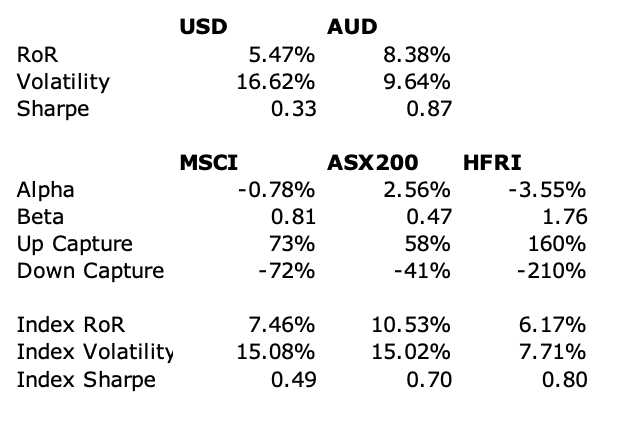

The investment performance statistics for the last five years are:

The first three rows are our unadjusted performance numbers in US and Australian dollar terms. The MSCI is reported in USD terms. The following four lines compare performance against each of the three indices over the last 60 months. The final three rows report the performance of the three indices themselves. We show the desired asymmetric capture and positive alpha against the ASX200 and the MSCI but not against the hedge fund index. We have a higher Sharpe Index than the ASX200 but lower than the MSCI in USD terms. We are performing about 2.6% per annum worse than the average hedge fund levered 1.75 times. Hedge funds have been doing well in recently.

We are now very close to our target allocation. Our actual allocation currently looks like this:

About 70% of our portfolio is in what are often considered to be alternative assets: real estate, art, hedge funds, private equity, gold, and futures. A lot of these are listed investments or investments with daily, monthly, or quarterly liquidity, so our portfolio is not as illiquid as you might think.

We receive employer contributions to superannuation every two weeks. We are now contributing USD 10k each quarter to Unpopular Ventures Rolling Fund and less frequently there will be capital calls from Aura Venture Fund II. In addition, we made the following investment moves this month:

- I bought 1,000 shares of the China Fund, CHN.

- I bought 3,000 shares of Ruffer Investment Company, RICA.L.

Friday, February 24, 2023

New Investment or Trade

I sold some Pengana Private Equity (PE1.AX) shares as they are trading above NTA and bought some Cordish Dixon Private Equity Fund III (CD3.AX) shares, which are trading more than 30% below NTA. Of the three traded Cordish-Dixon funds, I selected this one as it is youngest and so I figured has the most potential. Maybe the oldest fund maybe has only more problematic companies left in it, which are harder to sell? It is also the biggest of the three funds because it has made fewer distributions to date.

This was spurred by news that PE1 has made offers to acquire the CD funds, though these have been rejected to date.

In other updates, I have been tied up in other projects and haven't had time to reconcile the accounts for the last couple of months. When I do, I will post reports.

Friday, February 03, 2023

Rates of Return Over 20 Years

The graph shows the average annual rate of return over the previous 20 years up to that date. Our target diversified portfolio has had a very consistent 20 year return, as has the ASX 200. The MSCI World stock market index and the S&P 500 have been less consistent. My own performance was not good up to 2020 when seen from a 20 year perspective. By January this year, though, it's almost matching the target portfolio and is near the MSCI World Index (which doesn't deduct management fees). One reason for this, is I did really badly in 2000-2003 in the dot.com crash or tech wreck and so performance is now measured from the low point of March 2023. The chart is measured in Australian Dollars.

Saturday, January 14, 2023

Annual Report 2022

Overview

This was the first year that our net worth fell since 2008. Investment returns were negative but the value of our house increased a bit and we did save some money.* We were far short of the best case projection I made at the beginning of the year of a net worth of AUD 6.7 million. In my academic career, I spent a lot of time this year working on preparing and then teaching a new course, though I did get at least one newish research project completed. I was supposedly on long service leave for the first three months of the year but didn't really get to take any time off. This year, I plan on taking it a bit easier in the first half of the year before focusing on teaching in the second half of the year. Teaching was more in person this year and so a bit more enjoyable. I didn't leave the Canberra region all year since getting back from the coast right after New Year's Day.

This was the first year that our net worth fell since 2008. Investment returns were negative but the value of our house increased a bit and we did save some money.* We were far short of the best case projection I made at the beginning of the year of a net worth of AUD 6.7 million. In my academic career, I spent a lot of time this year working on preparing and then teaching a new course, though I did get at least one newish research project completed. I was supposedly on long service leave for the first three months of the year but didn't really get to take any time off. This year, I plan on taking it a bit easier in the first half of the year before focusing on teaching in the second half of the year. Teaching was more in person this year and so a bit more enjoyable. I didn't leave the Canberra region all year since getting back from the coast right after New Year's Day.

All $ signs in this report indicate Australian Dollars. I'll do a separate report on individual investments. I do a report breaking down of spending after the end of the financial year.

Investment Returns

In Australian Dollar terms we lost 3.7% for the year but in USD terms we lost 9.6% because of the fall in the Australian Dollar over the year. The MSCI lost 18.0% in USD terms but the ASX 200 gained 0.9% in AUD terms. The HFRI hedge fund index lost 1.5% in USD terms. Our target portfolio lost 4.2% in AUD terms. So, we beat the MSCI and the target portfolio benchmarks this year but not the ASX 200 or HFRI Index.

In Australian Dollar terms we lost 3.7% for the year but in USD terms we lost 9.6% because of the fall in the Australian Dollar over the year. The MSCI lost 18.0% in USD terms but the ASX 200 gained 0.9% in AUD terms. The HFRI hedge fund index lost 1.5% in USD terms. Our target portfolio lost 4.2% in AUD terms. So, we beat the MSCI and the target portfolio benchmarks this year but not the ASX 200 or HFRI Index.

This chart compares our portfolio to the benchmarks in Australian Dollar terms over the year:

We tracked the target portfolio quite closely. It acted as a less volatile weighted average of Australian and international equity markets. Here are the same indices in US Dollar terms with the target portfolio replaced by the HFRI hedge fund index:

Here are annualized returns over various standard periods:

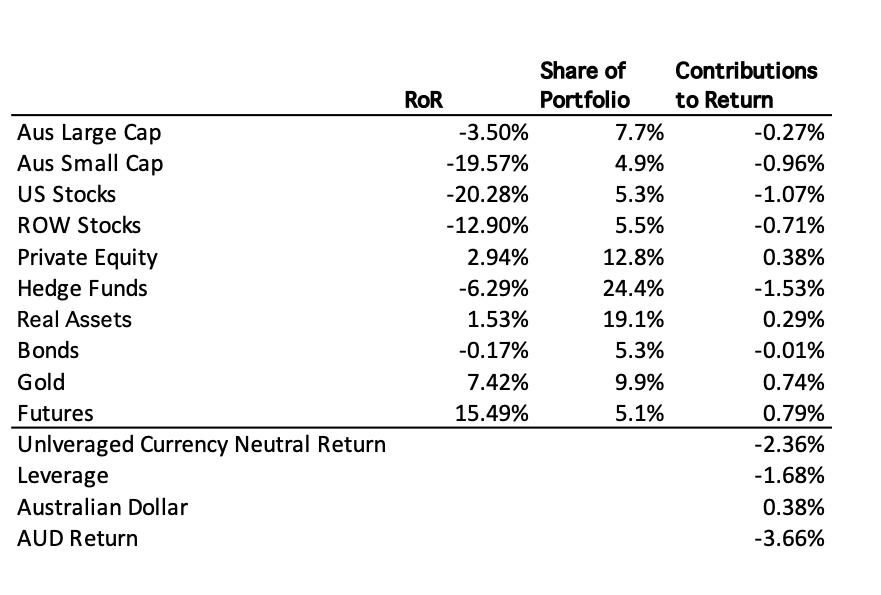

Here are the investment returns and contributions of each asset class in 2022:

The contributions to return from each asset class sum to the total portfolio return in gross asset and currency neutral terms. I then add on the contributions of leverage and the Australian Dollar to get the AUD net worth return. The portfolio shares are at the beginning of the year. Futures and gold did best and contributed most to the return. Private equity and real assets had small positive returns. Australian small cap stocks and foreign equities all did very badly.

Investment Allocation

There weren't large changes in asset allocation over the year:

Mainly, real assets fluctuated with our exposure to URF.AX, which is a very levered (effectively) US residential real estate fund.

Accounts

Here are our annual accounts in Australian Dollars:

Percentage changes are for the total numbers. There are lots of quirks in the way I compute the accounts, which have gradually evolved over time. There is an explanation at the end of this post.

We earned $153k after tax in salary etc. Total non-investment earnings including retirement contributions were $183k, down 9% on 2021. This was due to increased tax payments, fewer non-salary earnings, and fewer employee contributions to Moominmama's employer superannuation fund. We lost (pre-tax including unrealized capital gains) $166k on non-retirement account investments. A small amount of the gains were due to the fall in the Australian Dollar (forex). We lost $15k on retirement accounts with $30k in employer retirement contributions. The value of our house is estimated to have risen by $133k. As a result, the investment loss totaled -$45k and total income $139k.

Total spending (doesn't include mortgage payments) of $152k was again up 12% for the year. Spending was almost exactly equal to after-tax non-investment income. We saved just $488 from

salaries etc.

$25k of the current pre-tax investment income was tax credits – we don't actually get that money so we need to deduct it to get to the change in net worth. We transferred $120k into retirement accounts the SMSF from existing savings. This included $20k as a concessional contribution for Moominmama. Therefore, looking at just saving from non-investment income, we dissaved $120k. The change in current net worth, was therefore -$306k.

Taxes on superannuation returns are just estimated because apart from tax paid by the SMSF all we get to see are the after tax returns. I estimate this tax to make retirement and non-retirement returns comparable. The total implicit tax on supernnuation was a negative $1k because we lost money. Net worth of retirement accounts increased by $136k after the transfer from current savings.

Finally, total net worth fell by $37k.

Projections

Last year my baseline projection for 2022 was for a 16% rate of return, no increase in the value of our home, flat other income, and 6% growth in spending. This resulted in projected net worth increasing by $800k to around $6.7 million. Obviously, we came nowhere near this projection.

Projections

Last year my baseline projection for 2022 was for a 16% rate of return, no increase in the value of our home, flat other income, and 6% growth in spending. This resulted in projected net worth increasing by $800k to around $6.7 million. Obviously, we came nowhere near this projection.

This year the baseline projection (best case scenario) is for an 11.2% investment rate of return in AUD terms (assuming the Australian Dollar rises to 75 US cents), inflation of 7.6% and an 11% nominal increase in spending, and about a 3% increase in other income, leading to an $550k increase in net worth to around $6.5 million or a 9% increase. This would be very little gain in real terms after inflation. But, again, anything could happen.

Notes to the Accounts

Current account includes everything that is not related to retirement accounts and housing account income and spending. Then the other two are fairly self-explanatory. However, property taxes etc. are included in the current account. Since we notionally converted the mortgage to an investment loan, mortgage interest is counted in current investment costs. So, the only item in the housing account now is increases or decreases in the value of our house. This simplified the accounts a lot but I still keep a lot of cells in the spreadsheet that might again be used in the future.

Current other income is reported after

tax, while investment income is reported pre-tax. Net tax on investment

income then gets subtracted from current income as our annual tax refund

or extra payment gets included there. Retirement investment income gets

reported pre-tax too while retirement contributions are after tax. For

retirement accounts, "tax credits" is the imputed tax on investment

earnings which is used to compute pre-tax earnings from the actual

received amounts. For non-retirement accounts, "tax credits" are actual franking credits

received on Australian dividends and the tax withheld on foreign

investment income. Both of these are included in the pre-tax earning but

are not actually received month to month as cash....

For current accounts "core

expenditure" takes out business expenses that will be refunded by our

employers and some one-off expenditures. This year, there are

none of those one-off expenditures. "Saving" is the difference

between "other income" net of transfers to other columns and spending in

that column, while "change in net worth" also includes the investment

income.

* Venture capital returns haven't been reported yet for the December 2022 valuation, but I don't expect them to make a big difference.

Sunday, January 08, 2023

December 2022 Report

Venture capital returns won't be reported for another month, but I expect them to be flat, so that the final numbers are not far from what they are now. In December, stock markets fell. The MSCI World Index (USD gross) lost 3.90%, the S&P 500 5.76% in USD terms, and the ASX 200 3.13% in AUD terms. All these are total returns including dividends. The Australian Dollar rose from USD 0.6788 to USD 0.6816. We lost 1.24% in Australian Dollar terms or 0.83% in US Dollar terms. The target portfolio is expected to lose 2.43% in Australian Dollar terms and the HFRI hedge fund index around 1.3% in US Dollar terms. So, we out-performed all benchmarks.

Here is a report on the performance of investments by asset class:

The asset class returns are in currency neutral returns as the rate of return on gross assets. I have added in the contributions of leverage and other costs and the Australian Dollar to the AUD net worth return.

Only gold and private equity had positive returns. Gold was the biggest contributor to returns and hedge funds the greatest detractor.

Things that worked well this month:

- Gold gained AUD 14k and Pengana Private Equity (PE1.AX), 9k.

What really didn't work:

- Regal Funds (RF1.AX) lost AUD 12k followed by Hearts and Minds (HM1.AX) and Tribeca Global Resources (TGF.AX), which each lost 10k.

The investment performance statistics for the last five years are:

The first three rows are our unadjusted performance numbers in US and Australian dollar terms. The MSCI is reported in USD terms. The following four lines compare performance against each of the three indices over the last 60 months. The final three rows report the performance of the three indices themselves. We show the desired asymmetric capture and positive alpha against the ASX200 and the MSCI but not against the hedge fund index. We have a higher Sharpe Index than the ASX200 but lower than the MSCI in USD terms. We are performing about 2.5% per annum worse than the average hedge fund levered 1.7 times. Hedge funds have been doing well in recently.

We are now very close to our target allocation. Our actual allocation currently looks like this:

About 70% of our portfolio is in what are often considered to be alternative assets: real estate, art, hedge funds, private equity, gold, and futures. A lot of these are listed investments or investments with daily, monthly, or quarterly liquidity, so our portfolio is not as illiquid as you might think.

We receive employer contributions to superannuation every two weeks. We are now contributing USD 10k each quarter to Unpopular Ventures Rolling Fund and less frequently there will be capital calls from Aura Venture Fund II. In addition, we made the following investment moves this month:

- I bought 1,000 shares of PMGOLD.AX.

- I tried to do a trade with around 12k shares of Regal Funds (RF1.AX). It wasn't successful.

- I closed a tiny position of WLS.AX shares pending the merger of WLS into WCMQ.AX.

- The remainder of our WLS shares will convert to WCMQ and our URFPA shares will convert to URF at the turn of the year.

Monday, January 02, 2023

How Can They Afford It?

One of Moominmama's friends (from undergrad days in the world's most populous country) told her they have bought a house in one of the most expensive neighborhoods here. They plan to knock it down and build their dream home including a swimming pool. It is in walking distance of their two children's school, the most expensive private school here. Her reasoning is that it costs AUD 4 million to buy an existing house like they want, and this will be cheaper. Still, a crappy house there costs almost AUD 2 million. They haven't sold their existing town house in our neighborhood yet and they apparently also bought her parents an apartment here. She is an administrator at my workplace on probably AUD 100-110k a year and her husband was an associate professor (AUD 150-158k). He recently moved to Moominmama's employer.

My immediate reaction was: "How can they afford to do that?" I think Moominmama gets a lot of her aspirations from following this family, including sending our children to private school.

Sunday, January 01, 2023

Subscriptions

Our utilities spending category had been rising strongly over time and so I decided to split out the "subscriptions" component:

The graph is in Australian Dollars per year. Data for 2022-23 is for calendar year 2022 and previous years are 1 July to 30 June to match the Australian tax year. Back in 2017-18, subscriptions were less than AUD 1k and so I included them together with phone and internet access bills in a "phone and internet" subcategory that got then bundled into "utilities". But they underwent a step change in 2020-21. Now I am only including "infrastructure" costs - phone bills, internet access, data storage etc. in the phone and internet subcategory. All the subscriptions and payments for electronic services are now in "subscriptions". I moved web-hosting to the "professional" category.

At least "subscriptions" aren't increasing much since the pandemic step change took place. Utilities have increased 36% since 2017-18, which is less than our overall 58% increase in spending. So, there isn't really a problem there. Childcare and education has increased most, by 483%. It was AUD 55k in the 2022 calendar year compared to only AUD 9k in the 2017-18 financial year. Calendar year 2022 spending was AUD 170k (USD 115k).

Friday, December 23, 2022

Domacom Reinstated to ASX Quotation

On the last trading day before Christmas, Domacom has been reinstated to quotation. I wonder where the price will end up?

7:27pm

It went up! Closing at 7 cents a share. It was last quoted at 6.5 cents before being suspended. There were more shares on the buy side than the sell side most of the day.

Saturday, December 03, 2022

November 2022 Report

In November, stock markets continued their rebound and the Australian Dollar rose strongly increasing US Dollar returns relative to Australian Dollar returns. The MSCI World Index (USD gross) rose 7.80%, the S&P 500 5.59% in USD terms, and the ASX 200 6.78% in AUD terms. All these are total returns including dividends. The Australian Dollar rose from USD 0.6387 to USD 0.6744. We gained 3.05% in Australian Dollar terms or 8.81% in US Dollar terms. The target portfolio is expected to gain 1.23% in Australian Dollar terms and the HFRI hedge fund index around 1.0% in US Dollar terms. So, we out-performed all benchmarks apart from the ASX.

Our SMSF hit a new high in terms of cumulative returns, exceeding the previous high in September 2021. It is now up more than 15% since inception and well ahead of our employer superannuation funds:

These are all in pre-tax terms - franking credits are included but no tax deducted. This will be a bit over-generous to the employer superannuation funds on the way up and the opposite on the way down. The increase in my US retirement account (TIAA) is to a large extent because of the fall in the Australian Dollar. It fell this month as the Australian Dollar rose. But the TIAA Real Estate Fund also performed extremely well over this period until recently.

Here is a report on the performance of investments by asset class:

Only futures had a negative return. RoW stocks were the best performer partly because of the rebound in the China Fund and hedge funds were the largest contributors to the month's return.

Things that worked well this month:

- Tribeca Global Resources was again the top performer in terms of dollars gained (TGF.AX, AUD 25k). Coming in second and third were the China Fund (CHN, 18k) and Australian Dollar Futures (17k). Also gaining more than AUD 10k were 3i (III.L, 17k), Unisuper (16k), PSS(AP) (12k) Pershing Square Holdings (PSH.L, 12k), and gold (10k). With the exception of the China Fund and AUD futures, this is very similar to last month.

What really didn't work:

Winton Global Alpha Fund (-12k), Aspect Diversified Futures (-6k), and WAM Alternatives (WMA.AX, -4k) were the greatest detractors.

The investment performance statistics for the last five years are:

The first three rows are our unadjusted performance numbers in US and Australian dollar terms. The MSCI is reported in USD terms. The following four lines compare performance against each of the three indices over the last 60 months. The final three rows report the performance of the three indices themselves. We show the desired asymmetric capture and positive alpha against the ASX200 and the MSCI but not against the hedge fund index. We have a higher Sharpe Index than the ASX200 but lower than the MSCI in USD terms. We are performing more than 3% per annum worse than the average hedge fund levered 1.79 times. Hedge funds have been doing well in recent years.

We are now very close to our target allocation as Regal Funds diversifies its holdings. Our actual allocation currently looks like this:

About 70% of our portfolio is in what are often considered to be alternative assets: real estate, art, hedge funds, private equity, gold, and futures. A lot of these are listed investments or investments with daily, monthly, or quarterly liquidity, so our portfolio is not as illiquid as you might think.

We receive employer contributions to superannuation every two weeks. We are now contributing USD 10k each quarter to Unpopular Ventures Rolling Fund and less frequently there will be capital calls from Aura Venture Fund II. In addition, we made the following investment moves this month:

- I sold 5000 shares of WAM Leaders (WLE.AX) and bought 1000 shares of the China Fund (CHN).

- I sold USD 17.5k of the TIAA Real Estate Fund and bought the Social Choice Fund instead.

- I bought 4000 shares of Regal Partners (RPL.AX).

- I sold the 2000 shares I held in Fortescue Metals (FMG.AX). We made about AUD 4k on this trade.

- I sold 10k shares of Regal Funds (RF1.AX) and bought 500 shares of URFPA.AX - the US Masters Residential Fund converting preference notes.

- I sold 1,000 shares of Ruffer (RICA.L) to get money for our next subscription payment for Unpopular Ventures.

Thursday, December 01, 2022

Regal Funds Adds Private Credit

After recently adding a resource royalties strategy, Regal Funds (RF1.AX) are now adding a private credit strategy. They also announced a placement and rights issue to help implement the new strategy. The fund started primarily as a listed hedge fund with some private equity. But it is increasingly becoming a diversified alternatives fund. I suppose all these new strategies are supposed to reduce the correlation of the fund to the stockmarket. The fund has had a beta of 1. However, this looks like it will come at the expense of performance. You can't do 20% a year in strategies like private credit. Well, I guess you can lever up...

In any case, performance wasn't good in November, especially relative to the stockmarket which rose strongly. I sold 10,000 shares this week to increase my holding of URFPA. The rights offering is at AUD 3.01 a share (current NAV) with a maximum of AUD 30k per holder. I decided not to bother as I can't buy more than 2,000 shares without selling something else.

Saturday, November 05, 2022

October 2022 Report

In October, stock markets rebounded and the Australian Dollar ended close to flat. The MSCI World Index (USD gross) rose 6.06%, the S&P 500 8.10% in USD terms, and the ASX 200 6.06% in AUD terms. All these are total returns including dividends. The Australian Dollar fell from USD 0.6399 to USD 0.6387. We gained 2.85% in Australian Dollar terms or 2.66% in US Dollar terms. The target portfolio gained 3.07% in Australian Dollar terms and the HFRI hedge fund index is expected to be almost flat at 0.08% in US Dollar terms. So, we under-performed all benchmarks apart from HFRI, though we were not far from the target portfolio.

Here is a report on the performance of investments by asset class:

Only rest of the world stocks had a negative return, which was because of the poor performance of China. US stocks were the best performer and hedge funds the largest contributors to the month's return.

Things that worked well this month:

- Tribeca Global Resources (TGF.AX, AUD 18k), Unisuper (15k), Pershing Square Holdings (PSH.L, 12k), and PSS(AP) (10k) were the largest contributors.

What really didn't work:

The China Fund (CHN, -9k) and Fortescue (FMG.AX, -4k) were the greatest detractors.

The investment performance statistics for the last five years are:

The first three rows are our unadjusted performance numbers in US and Australian dollar terms. The following four lines compare performance against each of the three indices over the last 60 months. The final three rows report the performance of the three indices themselves. We show the desired asymmetric capture and positive alpha against the ASX200 but not against the hedge fund index nor the MSCI. We have a higher Sharpe Index than the ASX200. We are performing more than 3% per annum worse than the average hedge fund levered 1.76 times. Hedge funds have been doing well in recent years.

We moved towards our target allocation mainly by reducing exposure to hedge funds and gold. Our actual allocation currently looks like this:

About 70% of our portfolio is in what are often considered to be alternative assets: real estate, art, hedge funds, private equity, gold, and futures. A lot of these are listed investments or investments with daily, monthly, or quarterly liquidity, so our portfolio is not as illiquid as you might think.

We receive employer contributions to superannuation every two weeks. We are now contributing USD 10k each quarter to Unpopular Ventures Rolling Fund and less frequently there will be capital calls from Aura Venture Fund II. In addition, we made the following investment moves this month:

- We received the payout from the sale of Gargantua.

- I sold 5k shares of Cadence Capital (CDM.AX) to get some cash.

- I sold 11k shares of Regal Funds (RF1.AX) that I bought in September.

- I sold 1000 shares of PMGOLD (PMGOLD.AX) as the Australian Dollar gold price peaked a little. I'm now feeling that we are at a much more comfortable debt level in our margin accounts given the rise in interest rates and volatility.

Wednesday, October 26, 2022

Real Salary

I was wondering whether we were getting worse off over time at my employer and so plotted my real and nominal pre-tax salary for the time I have been in my current position. Halfway along there was a blip where I was department head and got paid more. In real terms I am now about $2000 below where I started in 2011. The union is asking for a 15% increase in the latest bargaining round. After tax that is a about an 11% increase (because of progressive tax rates).

Saturday, October 22, 2022

More Factoids from the 2019-2020 Australian Income and Wealth Survey

3.2% of households are in both the top income and top net worth deciles. That means their net worth is above $2.258 million and their annual income is above $235k.

Friday, October 21, 2022

2019-20 Australian Income and Wealth Distribution

I didn't notice when the Australian Bureau of Statistics released the 2019-20 data on Australian household income and wealth distribution. I previously reported on the 2015-16 and 2017-18 data.

Mean gross household income was $121k per year in 2019-20 (all $ are Australian Dollars). The median was $93k. These are not adjusted for household size. ABS provides data adjusted for household size in terms of the income a single person would need to achieve the economic well-being of the average household. To adjust these to the required income of a household with 2 adults and 2 children requires multiplying by 2.1. I seriously doubt that adding a child only increases costs by 0.3 of the first adult!

Mean gross household income in the ACT was $150k and the median $124k.

To be in the top 10% of households requires a gross income of at least $235k. To get information on the breakdown inside the top 10% you have to use their data on the number of households within each of different bands of weekly income. 4.7% of households have an annual income above $312k and another 3% between $260k and $312k. Our gross income was $264k (taxable income), so we just fall within this group and, therefore, in the top 7.7%.

Mean household net worth was $1.04 million and the median was $579k. To be in the top 10% you needed a net worth of $2.26 million. We were at $4.44 million at the end of June 2020. To be in the top 3.9% you needed a net worth of $4 million. So I estimate we were at the edge of the top 3.3%. I guess it makes sense given my age that we higher in the wealth distribution than in the income distribution.

1.2% of households had a net worth above $7 million and 0.6% above $10 million.

There is a lot more data on breakdown of assets etc. which I might report on another time.

To be in the US top 1% by net worth required USD 11 million ($17.75 million) in the same period. A top 1% US household income is around USD 600k and above.

Tuesday, October 18, 2022

Regal Investment Fund Implements Resource Royalties Strategy

Regal Investment Fund (RF1.AX) is continuing to diversify their portfolio. Recently, they added a water strategy through Kilter Rural. Now they are adding a resource royalties strategy through the Gresham Resource Royalties Fund. While the water strategy is only 2% of the fund, the resource royalties strategy will be 17% of the fund initially. I am categorizing both of these in the real assets class. From the announcement:

"A resource royalty is a right to receive payment usuallyreflecting the value of a percentage of revenue derived from the production from a mining, oil and gas or renewable project. A commodity stream is an agreement conferring a right to purchase all or a portion of the production produced from a mining, oil and gas or renewable project at a pre-set price. Royalties and commodity streams are often used interchangeably. Royalties and commodity streams are typically acquired for an upfront payment. They can provide investors with the upside potential of increased commodity prices, increased production and extended mineral reserves (and sometimes new discoveries) with no or limited exposure to variable operating costs and future capital calls to fund exploration or other capital costs."

Subscribe to:

Posts (Atom)