The Australian Dollar fell from USD 0.7185 to USD 0.6909 and gold fell steeply. International stock markets lost a little and the Australian market still managed to underperform in USD terms, though it gained in AUD terms. The following results are preliminary–we won't get venture and art results for a while.

Here is the performance of our benchmarks (total returns including dividends):

US Dollar Indices

MSCI World Index (gross): -0.77%

S&P 500: -0.95%

HFRI Hedge Fund Index (forecast): -0.16%

Australian Dollar Benchmarks

ASX 200: 0.73%

Target Portfolio (forecast, depends on HFRI): -0.03%

Australian 60/40 benchmark: 1.36%

In Australian Dollar terms we gained 0.51% and in US Dollar terms we lost 3.35%. The only benchmark we outperformed was the target portfolio. The SMSF also underperformed, losing 0.67% while Unisuper gained 2.05% and PSS(AP) 2.23%. Why did the target portfolio have weak performance this month? Gold detracted 0.82% of return and venture capital 0.84%. If we add those two back, the return would be 1.63%, which is between the ASX 200 and MSCI (AUD) returns. We outperformed the target largely due to not experiencing those negative venture returns.

Australian superannuation funds report performance for the Australian financial year which ends on 30 June. For this period, the SMSF gained 12.2% (pretax), Unisuper, 8.9%, and PSS(AP) 11.3% (estimated pretax). So, we beat both benchmarks.

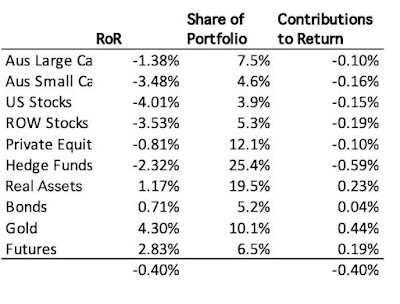

Here is a report on the performance of investments by asset class:

The asset class returns are in currency neutral terms and gross asset terms and do not include investment expenses such as margin interest, and so the total differs from the Australian Dollar returns on net assets mentioned above. Gold and futures lost a lot and private equity a little. All other asset classes gained with rest of world stocks having the highest return and Australian large cap, hedge funds, and US stocks each contributing about a quarter of a percent of returns.

There was a lot of dispersion of returns, with lots of big winners and big losers. Things that worked well this month:

- Eight investments made AUD 10k or more: L1 Global Long-Short (GLS.AX, 49k), Acadian Global Long-Short (24k), Unsiuper (17k), 3i (III.L, 16k), Regal Investment Fund (RF1.AX, 14k), PSS(AP) (11k), Regal Partners (RPL.AX, 10k), and WCM Global Quality Active ETF (WCMQ.AX, 10k).

What really didn't work:

- Five investments lost more than AUD 10k: Gold (-59k), Pershing Square Holdings (PSH.L, -40k), Australian Dollar Futures (-30k), Pengana Private Equity (PE1.AX, -22k), Tribeca Global Resources (TGF.AX, -22k).

Our distance from our target allocation increased a little. Our actual allocation currently looks like this:

Moominmama receives employer superannuation contributions every two weeks. We also make monthly concessional contributions to Moominmama's superannuation to reach the annual cap on contributions. There will still be capital calls from Aura Venture Fund II and III. I am receiving monthly pension payments from both Unisuper and our SMSF totalling AUD 5,150 per month. I made the following other moves this month:

- I did invest in five new startups via Angellist! So, I was busy reading all the investment memos and pitch decks of companies I didn't end up investing. One of the startups is a secondary sale of Polymarkets shares, which is a private company, but beyond the startup phase.

- I sold 10k Regal Investment Fund (RF1.AX) shares and bought 20k Pengana Private Equity (PE1.AX) shares, which were undervalued after the SpaceX IPO. SpaceX is their biggest holding. My theory, is that people investing in Pengana's new AI fund, may have been sellling their PE1 shares.

- I bought 1k shares in Metrics Opportunities (MOT.AX)–a listed private credit fund.

- I bought 17.5k shares of Treasury Wine Estates (TWE.AX).

- I sold 50 Berkshire Hathaway shares and 1,000 ASX 200 ETF (IOZ.AX) shares to fund it.

- I bought 30k shares of the L1 Gold Fund (LFG.AX).

- I added to some of my trading positions at Masterworks after another painting realization.

- I bought a few additional shares of one of the NDIS properties I am invested in at Assetora using accumulated investment income there.

As you can see, while we have so much cash in our offset account, I am tending to still reinvest some of our investment income.

Here are the income and spending accounts * for this month ($ is Australian Dollar):

Other income includes Moominmama's salary and employer superannuation contributions but also the tax paid by the SMSF. Other retirement number is negative this month because I submitted a "Notice of Intent" to claim a tax deduction to Moominmama's employer super fund, which triggered 15% tax on the $22.5k of voluntary contributions I had made this year to it. Moominmama bought a new laptop for $2197, which her employer reimbursed–it is counted both in other income and spending. So, spending was a bit higher this month. This number does not include our mortgage payments, which are regarded here as saving and investment costs. Dissaving amounted to $8k, which is way within the 4% rule limit of AUD 23k. We gained $35k investing, mostly from retirement accounts and all because of the fall in the Australian Dollar. We got an estimated $8k in tax credits and implicit tax on our employer super, which are included in pretax investment returns but have to be deducted to get to the change in net worth. As a result of all this, net worth rose by AUD 19k to AUD 8.246 million.

* Results are shown separately for retirement and non-retirement accounts as well as housing, which nowadays doesn't have much activity. The grey shaded rows are additional notes. Total investment income is split into investment income before exchange rate moves and the contribution of exchange rates. Other income is non-investment income including salaries, employer superannuation contributions, net tax returns minus superannuation contribution tax and all SMSF tax payments to the ATO. Investment income is shown pre-tax. Tax credits include franking credits on Australian Dividends etc. in non-retirement accounts and the SMSF and imputed tax on industry superannuation returns. These are taken away from investment income to get changes in actual net worth. Inheritances include gifts from relatives. Saving is from non-investment income, transfers, and inheritances not investment income.

.jpg)

.jpg)