Saturday, April 29, 2006

Weekend Links

John Mauldin's latest weekly letter is all about the weakening US Dollar and the Federal Reserve. Included is this great video! :) We've been watching Ben Bernanke in the Introductory Economics course I teach. We use the textbook the coauthored with Robert Frank and keep uptodate on his progress. And then this crazy real estate listing! That wild insider trading case again, and, finally, an article on renting vs. buying from the Economist.

End of the Month

Looks like I made about a 5% investment return for April. Most of the move was due to the strong rally in the Australian Dollar. The core investment gain - not counting exchange rate movements - was pretty small.

Last month, by contrast, the move in the Aussie was negative and wiped out most of my core investment gains.

Net worth increased by almost $20,000. One of my highest monthly gains, but not unprecedented. I am about $10,000 ahead of the target I set for April based on my goal of increasing net worth by $100,000 in 2006.

Moominmama also saw strong gains due to the fall in the US Dollar.

There doesn't seem to be much awareness of the collapse in the US Dollar in the media.

In the coming days I will post the final results for April.

Last month, by contrast, the move in the Aussie was negative and wiped out most of my core investment gains.

Net worth increased by almost $20,000. One of my highest monthly gains, but not unprecedented. I am about $10,000 ahead of the target I set for April based on my goal of increasing net worth by $100,000 in 2006.

Moominmama also saw strong gains due to the fall in the US Dollar.

There doesn't seem to be much awareness of the collapse in the US Dollar in the media.

In the coming days I will post the final results for April.

Wednesday, April 26, 2006

What Does the Rise in the Gold Price Mean?

Interesting article that looks at whether the rising price of gold is a signal of future inflation. Especially interesting is the comparison of the price of gold to that of other metals. Industrial metals make gold look cheap! No crash yet - but the stock market remains weak. Today I added I took a slightly more bearish stance by buying more QQQQ puts with the cash in my Roth IRA account - doubling the number of contracts. I like to buy in the money options and pay a minimum of time premium. Buying at the money or out of the money options really does seem like gambling. The options have no current "intrinsic value" and unless the stock price moves in your direction by the expiry date you lose all your money... Deep in the money options are closer to futures contracts or heavily leveraged stock positions and are definitely more my "cup of tea" :)

Thursday, April 20, 2006

Potential Crash Warning

One of the things that maybe gives me some trading edge is a technical analysis indicator I developed myself. It is very different to traditional indicators and is based on an autoregression model computed in a spreadsheet. I apply it to the main stocks I trade.

I just did some forward simulations on my NDX spreadsheet using my autoregressive indicator. There is the potential for a massive crash in coming days and weeks. I can't forecast a crash with the indicator, all I can do is plug in some values for the index and see whether the indicators they yield make any sense. Basically the model finds turning points. So if I plug in a number for tomorrow or next week or whenever and it yields a turning point value (greater than one) then I know that is a bottom or top. Very large declines are now possible before the bottom is reached. This wasn't possible even a couple of days ago, but the last couple of days' rally has loosened things up and the index has come to a potential top turning point on my weekly spreadsheet.

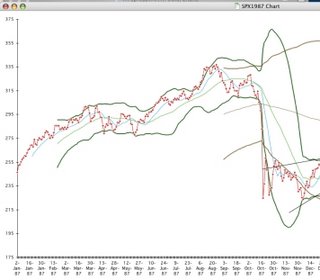

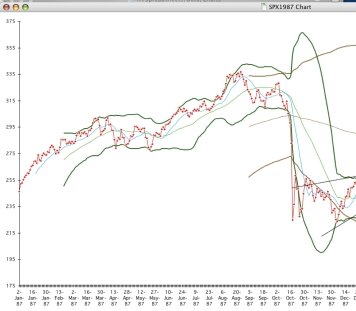

For those of you who remember, I reckon the current juncture has some of the feel of Fall 1987. Read the discussion of the crash in the Alchemy of Finance. Interest rates and the US Dollar played a key role in the crash. In fact the current NDX chart and the SPX chart from that period are uncannily similar in appearance:

Now check this.

Of course this isn't a forecast. Nothing may happen. Or perhaps it will.

I just did some forward simulations on my NDX spreadsheet using my autoregressive indicator. There is the potential for a massive crash in coming days and weeks. I can't forecast a crash with the indicator, all I can do is plug in some values for the index and see whether the indicators they yield make any sense. Basically the model finds turning points. So if I plug in a number for tomorrow or next week or whenever and it yields a turning point value (greater than one) then I know that is a bottom or top. Very large declines are now possible before the bottom is reached. This wasn't possible even a couple of days ago, but the last couple of days' rally has loosened things up and the index has come to a potential top turning point on my weekly spreadsheet.

For those of you who remember, I reckon the current juncture has some of the feel of Fall 1987. Read the discussion of the crash in the Alchemy of Finance. Interest rates and the US Dollar played a key role in the crash. In fact the current NDX chart and the SPX chart from that period are uncannily similar in appearance:

Now check this.

Of course this isn't a forecast. Nothing may happen. Or perhaps it will.

Sell in May and Go Away

Great article by Mark Hulbert on the "Sell in May and Go Away" saying. It is true that stocks perform worse in the summer and better in the winter. In the article he looks into the question of whether there is another asset class that performs better in summer and worse in winter. He finds that the Lehman US Bond Index does perform better in summer than winter. Therefore, an optimal strategy is to sell stocks and buy bonds for the summer. Of course this is just a statistical average over the long term and won't work every year. At the moment, though, I am net short stocks (including put options as shorts) and long bonds, which is a more extreme version of this strategy. I'm also 60% or so at least exposed to the Australian Dollar and only 20% to the US Dollar which is falling. In computing the latter I look at a firm's primary listing - for example, News Corp is a US Dollar asset even though I trade it in Australia. I'm now up to 2% allocated to gold (in my Roth IRA through GLD). Recent trades including buying TLT calls (today that doesn't look like such a great idea!) and this morning Yahoo puts. Yahoo's earnings report yesterday met expectations. So why the huge ramp in price? This is the kind of trade I do on news occasionally. When Fortune decides that finally it is time to get back into net stocks, it may actually be time to get out (or past time). This month the main news in my portfolio has been the rise in the Australian Dollar - each 1 US cent move up adds about $US3700 to my net worth.

Tuesday, April 18, 2006

Buying and Holding an Index Fund is so 20th Century

More Bond Bulls

These guys' Q1 report - highlighted in John Mauldin's latest letter - has an identical viewpoint to my own on inflation, bonds etc.

Monday, April 17, 2006

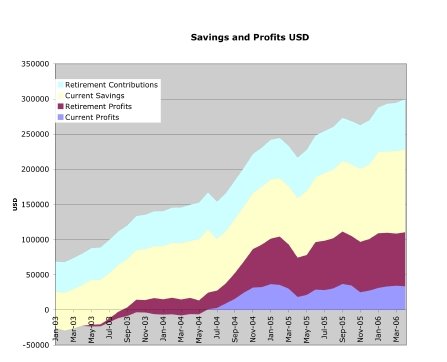

Savings vs. Profits

I was curious what fraction of my net worth accumulation had come from saving and how much from investment profits. I created this chart, which also breaks things down between retirement and non-retirement accounts. Profits on the retirement accounts now exceed contributions. Performance on the non-retirement accounts has not been as good. Cumulative profits in both categories were negative in January 2003 after substantial bear market losses. Non-retirement saving has not been much recently as I have fully funded a Roth IRA for 2005 and 2006.

Sunday, April 16, 2006

Clustermaps is Amazing

This Clustermaps application is so amazing! Every day I check the new red spots appear on the map. The latest entrants are for Bangkok, somewhere in southern Turkey, and Tokyo. Everyone I show it to is amazed also. I also installed one on my academic homepage.

Saturday, April 15, 2006

Is There a Housing Bubble?

There have been a couple of recent economic studies published that argue that there is no housing bubble. One paper by Himmelberg et al. and another by Hwang Smith and Smith.

Both studies value houses appropriately from the point of view of a potential homebuyer. I don't have any problems with their house pricing formula or data on existing prices, rents, and other variables. My problem is with their conclusion that their results indicate that there is no housing bubble.

The valuation formula takes into account rents for rental housing, interest rates, property tax, maintenance costs, federal and state tax deductions etc. and, crucially, potential capital appreciation. It makes sense to pay more for a house if you think its price will go up. So from the point of view of a potential buyer their formula for valuing a house is correct.

But this builds an expectations component into homeprices. If people think houseprices will rise they will pay more for houses. If houseprices continue to rise this will have turned out to be correct. But if houseprices in fact stop rising then the prices people are paying will turn out to be too high and prices will start to fall. Falling prices mean negative capital appreciation, which means prices should be even lower. There couldn't be a simpler and better bubble generating mechanism.

The two studies I cited assume house prices will continue to rise at historic rates. If you assume that, then people are not currently paying too much for housing in supposed bubble zones and hence the authors claim that there is no bubble - houses are not overvalued. But the instant prices stop rising - for example due to increasing interest rates - suddenly homes are overvalued and there is a bubble!

Similar mechanisms exist in the stock market - as discussed by Soros in The Alchemy of Finance. Stock prices partly depend on expectations of the growth rate of corporate profits. Soros pointed out that sometimes these contain a self-reflexive component where increasing stockmarket valuations feed back into increasing corporate profits. But in the housing market the growth component is even more self-reflexive. If everyone believes houseprices will rise then they will, until people no longer believe this.

In conclusion it is impossible to find whether a bubble exists by looking at whether house prices are currently overvalued based on historic capital appreciation rates. You have to be able to also model the future path of house prices and then ask: "Given this future path, are prices now too high". Yes the two depend on each other - the economics is dynamic and not as simple as the economics in these papers.

Both studies value houses appropriately from the point of view of a potential homebuyer. I don't have any problems with their house pricing formula or data on existing prices, rents, and other variables. My problem is with their conclusion that their results indicate that there is no housing bubble.

The valuation formula takes into account rents for rental housing, interest rates, property tax, maintenance costs, federal and state tax deductions etc. and, crucially, potential capital appreciation. It makes sense to pay more for a house if you think its price will go up. So from the point of view of a potential buyer their formula for valuing a house is correct.

But this builds an expectations component into homeprices. If people think houseprices will rise they will pay more for houses. If houseprices continue to rise this will have turned out to be correct. But if houseprices in fact stop rising then the prices people are paying will turn out to be too high and prices will start to fall. Falling prices mean negative capital appreciation, which means prices should be even lower. There couldn't be a simpler and better bubble generating mechanism.

The two studies I cited assume house prices will continue to rise at historic rates. If you assume that, then people are not currently paying too much for housing in supposed bubble zones and hence the authors claim that there is no bubble - houses are not overvalued. But the instant prices stop rising - for example due to increasing interest rates - suddenly homes are overvalued and there is a bubble!

Similar mechanisms exist in the stock market - as discussed by Soros in The Alchemy of Finance. Stock prices partly depend on expectations of the growth rate of corporate profits. Soros pointed out that sometimes these contain a self-reflexive component where increasing stockmarket valuations feed back into increasing corporate profits. But in the housing market the growth component is even more self-reflexive. If everyone believes houseprices will rise then they will, until people no longer believe this.

In conclusion it is impossible to find whether a bubble exists by looking at whether house prices are currently overvalued based on historic capital appreciation rates. You have to be able to also model the future path of house prices and then ask: "Given this future path, are prices now too high". Yes the two depend on each other - the economics is dynamic and not as simple as the economics in these papers.

Friday, April 14, 2006

Wealth Distribution

There has been some discussion on NetWorthIQ about what fraction of the US and world population are millionaires. It is surprisingly hard to get that information and there are various definitions including both total net worth, net worth excluding primary residence, and financial net worth. An expert on the topic is Edward Wolff, his paper on the topic of changes in the net worth of US households in the 1980s and 1990s includes official data from 2001. It doesn't quite give the answer but has lots of interesting data. Based on this, I estimate that in current dollars using a broad definition of net worth there are around 10 million millionaire households in the US. This is far above the Merrill Lynch estimate but close to the TNS estimate. Also my net worth is about average for someone of my age and income, though its composition is rather unusually biased to financial securities.

Update (20 April): Another survey on wealthy households in the US

Update (20 April): Another survey on wealthy households in the US

Wednesday, April 12, 2006

$300,000

Today I exceeded $300,000 in net worth for the first time. This is based on an update of all values yesterday and the change in exchange rates and my Ameritrade account today. The rise in the Australian Dollar and fall in the stockmarket pushed me over the line. A falling stockmarket has a positive effect on my short positions and put options. The beta of my portfolio is currently -0.35, which means that a 1% fall in the stock-market increases my net worth by 0.35% on average.

It took till November 2001 to reach the first $100,000. My net worth declined after that, though, to a low of $56,000 in September 2002 shortly after I moved back to the US. I again reached $100,000 in August 2003 and $200,000 in October 2004.

Let's see if I can stay in the new wealth bracket permanently!

It took till November 2001 to reach the first $100,000. My net worth declined after that, though, to a low of $56,000 in September 2002 shortly after I moved back to the US. I again reached $100,000 in August 2003 and $200,000 in October 2004.

Let's see if I can stay in the new wealth bracket permanently!

Sunday, April 09, 2006

Check that Tax Return!

Today I got my tax assessment letter from the IRS. Now I know why the refund they paid me was $1250.00 less than I expected. I forgot to fill in line 23 of my Schedule A! Line 23 asks you to add together lines 20 through 22. I did, but forgot to fill in the box. I used the number I calculated in computing line 26 which is where you deduct line 25 from line 23. As my line 23 had zero on it their computer told them my line 26 should have zero too. Instead I had $4981.04. As a result they raised my taxable income by that amount and taxed me $1250.00 more. I will phone the IRS and explain it to them. So, those of you out there who haven't yet filed - check all the relevant boxes are filled in and if the IRS changes your refund, don't assume they are right! I will recognize the extra $1250.00 in my net worth immediately.

Picking Stocks is Hard

Looks like Croesus Mining will survive though I have no idea what the shares will trade at on 28 April when the suspension ends. One reason I originally bought shares in this company was because I had read they were not doing much hedging of the gold price. And looking at the accounts over the years this seemed to be the case until suddenly their hedgebook exploded. Gold miners hedge by agreeing to sell their gold at a predetermined price using futures (or forward) contracts. This means that they miss out on any upside or downside in the gold price. It gives them more certainty. Any extra gold they produce could be sold at the spot price. A problem happens, I now understand when production falls short and the gold price is rising steeply. Then they need to buy gold at the spot price and sell it at their lower contract price. I knew also that Croesus was having some difficulties in operations, but it seemed like they were addressing these - for example selling a large part of their mineral concessions at a nominal profit. And the company kept putting out announcements on promising exploration results. Seemed that reserves while never big were being replenished. A warning sign I should have noted was when last year they appointed a new CEO who resigned within months. I thought I understood fairly well what was going on with this firm, but now I see I didn't. This is a reason that I don't try to pick many individual stocks in "industrial companies" for long term holdings (as opposed to closed end funds, and other financial operations). I have very few. It is hard for an individual investor to have any edge in this, unless they are knowledgable about a particular industry or there is a very clear undervaluation phenomenon.

Friday, April 07, 2006

Turning Point in the Bond Market?

Great article from Bill Gross explaining why the bear market in bonds (equals rising long term bond rates) should be almost over. It's a bet I have been making through holdings in bond and majority bond mutual funds, so far with neither good or bad results (apart from missing out on stock market gains I could have made. Colonial First State's Conservative Fund has however performed nicely over this period.

Today the gold price touched $600 per ounce in the futures market and a little less in the spot market. The Australian Dollar has been rally ever since I did that transfer to Australia - so good timing for once. On the other hand the stock market has been resilient but the McClellan Oscillator has been pretty weak the last three days.

Today the gold price touched $600 per ounce in the futures market and a little less in the spot market. The Australian Dollar has been rally ever since I did that transfer to Australia - so good timing for once. On the other hand the stock market has been resilient but the McClellan Oscillator has been pretty weak the last three days.

Tuesday, April 04, 2006

Salary Increase and March Report

Got the letter today. 1.5%. Inflation is 3.6% p.a. currently. The pool for all salary increases was 2.5%. The rest of the letter went on about how we should think of our department's performance measures as an opportunity for next year and beyond. My chairman ranked me as strong on two measures and outstanding on one of the three. Not much incentive is it.

In the end I got a -0.47% return on investment for March in US Dollar terms. In Australian Dollar terms I made 2.87%. The fall in the Australian Dollar more than wiped out all my positive performance when measured in USD. The MSCI world index returned 2.24%. As a result, net worth increased by only $US1,474 but by $A16,653 to $A411k ($US295k). Still that means I am up $25k so far this year which is exactly on track to add $100k to net worth by the end of the year.

In the end I got a -0.47% return on investment for March in US Dollar terms. In Australian Dollar terms I made 2.87%. The fall in the Australian Dollar more than wiped out all my positive performance when measured in USD. The MSCI world index returned 2.24%. As a result, net worth increased by only $US1,474 but by $A16,653 to $A411k ($US295k). Still that means I am up $25k so far this year which is exactly on track to add $100k to net worth by the end of the year.

Sunday, April 02, 2006

Federal Tax Refund

Received my refund and it is more than $1200 less than expected :( Will have to wait to get a statement to see why there is such a large discrepancy. Whether they disallowed something or I miscalculated something. Something very curious is that the number of cents after the decimal is exactly the same as what I calculated. In fact, the two figures are different by exactly $1250.00. Very weird. Am restating my February accounts and net worth.

PS: Sunday - decided to transfer $3000.00 - my refund + $500 to my Roth IRA. Enough to buy another 5 ounces of gold :)

PS: Sunday - decided to transfer $3000.00 - my refund + $500 to my Roth IRA. Enough to buy another 5 ounces of gold :)

Saturday, April 01, 2006

Google Enters the S&P 500 Index

Crazy action at the end of the trading day and after hours as GOOG entered the S&P 500 Index and Google's 5.3 million secondary share offering was priced. Huge volume. I would interpret the downward pressure towards the end as players who bought shares in the last week in the hope to sell them to mutual funds dumping their surplus. They should have a surplus if they didn't expect this 5.3 million share offering. We can't really know this unless we are actually inside these institutions, but it is a picture that makes sense. I stayed short GOOG at the end. Tried to play HANS. There was a rumor that they are in talks with Anheuser-Busch, which pushed the stock up in pre-market trading. I shorted but missed my opportunity to buy back before the news wires reported the story and pushed the stock up again. Covered after hours for a small loss. Trading has been harder recently, no big wins since WLS jumped $20 on the offer by William Lyon to buy out the company. My average return on a trade so far this year is now about 0.45%. The experiment will continue :)

In the next several days will calculate and report results for March.

In the next several days will calculate and report results for March.

Friday, March 31, 2006

Are We at a Market Top?

I think the probability that the downphase of the four year cycle is now underway is getting higher. Been looking over various of the usual charts this evening. I was looking for another up wave in the NASDAQ 100 Index. But the NASDAQ Composite and S&P 500 have reached new 5 year highs and it looks hard for them to push higher. The Australian All Ordinaries is at an all time high and a model I have developed is now sending a strong sell signal on that index. There are some countervailing indicators - as always the picture is not totally clear. The US Dollar is looking also very weak on the charts... this is surprising. I thought this wouldn't happen till the Fed stopped raising interest rates. The Australian Dollar has rallied since I bought a few days back.

My portfolio is now net short when taking into account the correlation of the various assets with the general market (beta). In fact for a 1% fall in the market I should see an approximately 0.2% rise in my portfolio, everything else held constant.

My portfolio is now net short when taking into account the correlation of the various assets with the general market (beta). In fact for a 1% fall in the market I should see an approximately 0.2% rise in my portfolio, everything else held constant.

pfblog.org

This site is cool. LInks to almost 400 personal finance blogs and data on how many visits they have received and how many clicks have been made on each entry. Moomin Valley is included. Which it isn't on pfblogs.com.

Gold

I bought some gold for the first time ever today (in my Roth IRA). This is through the Exchange Traded Fund GLD. Gold broke out of the trading range it was in and headed higher. And looks like going higher still... For several years now, gold has been rising and I put off buying because I held lots of Australian Dollars which traditionally have moved with gold... the link seems a bit broken now though (there was never a really good rationale for it). Also I had shares in a gold-mining firm (CRS.AX) which turned out to be rather a disaster...

I also bought more QQQQ put options in that account and sold Yahoo. So in my Roth there is 5 ounces of gold and around $20,000 of QQQQ shares sold short effectively. This is basically what the Prudent Bear mutual fund (BEARX) consists of.

I did a bunch of trades in my taxable Ameritrade accont too... am rather short...

I also bought more QQQQ put options in that account and sold Yahoo. So in my Roth there is 5 ounces of gold and around $20,000 of QQQQ shares sold short effectively. This is basically what the Prudent Bear mutual fund (BEARX) consists of.

I did a bunch of trades in my taxable Ameritrade accont too... am rather short...

Wednesday, March 29, 2006

Millionaire Households

Article on millionaire households. Not surprisingly Los Angeles County is #1 as it is the most populous county in the country (10 million people). What is surprising is that New York County (i.e. Manhattan) doesn't show up. Do the New York wealthy pretend to live somewhere else with lower taxes? Hide their wealth well.

Fed Day

Today is the day of the Federal Reserve statement - at 2:15pm - and it will be Ben Bernanke's first... The buzz on Silicon Investor and my own read of the markets is that investors and traders are very wary about what will be in the statement that accompanies the change in interest rates. Last year my Intro Economics class was 2-4pm on Tuesday and Friday and we followed the Fed decision live and its impact on the market. Pity I can't do that this time.... but will definitely be paying close attention at that time. Plan to show my students on Thursday what happened. The Aussie Dollar is up overnight... which is a nice change after I bought more Aussie Dollars. One of my best months ever from an Aussie Dollar perspective, but down in US Dollars... maybe a natural rebound after overselling... or a forecast that US interest rates will rise less? Or a response to the gold price? Maybe a bit of the latter but this morning the US Dollar is down across the board....

Update 5:41pm EST - the market eventually did go in the direction I expected after the Fed announcement. But I made a short bet on GOOG and it went the wrong way... oh well...

Update 5:41pm EST - the market eventually did go in the direction I expected after the Fed announcement. But I made a short bet on GOOG and it went the wrong way... oh well...

Friday, March 24, 2006

International Barriers and Bridges

Yesterday I decided to cancel a trip to speak at a university in the southern US. They told me that as I wasn't a US citizen (but am an H1-B, green card approved but no card yet, have a SSN, and am resident for US tax purposes) they couldn't reimburse my expenses. Instead they would have to pay through my university but I would have to fill out a pile of bureaucracy delving into my tax and visa issues and then set up all kinds of bureaucractic stuff between the universities.... I just wasn't going to put up with this and even though it will cost me $130 in cancellation and change fees on the flight I decided to pull the plug. Was sorry for the guy who invited me as he is an H1-B himself. Just wasn't going to put up with more of this stuff. At a committee meeting at this university today we were presented on the barriers the US is putting in the way of foreign researchers and students and how foreign competition in the university sector is catching up and overtaking the US.... nothing really of news to me on that (unlike some of the Americans at the table...)...

Anyway, have assembled a pile of US dollars in my HSBC account and tomorrow will transfer them to Australia. The Australian Dollar has been falling sharply this month. Ostensibly because the Fed is going to raise interest rates much more than the Reserve Bank of Australia will. I have saved $A15,000 so far this month, but am down in US Dollar terms as a result. So at least make lemonade from lemons and try to buy more Aussie Dollars cheap... They will then go to paying down my margin loan in Aus. Last night I sent a fax to my broker in Aus to withdraw $A8000 from two Aussie mutual funds and put that towards margin loan reduction. The Australian All Ords index reached the magical 5000 mark for the first time. My technical analysis model is "flashing" a sell signal. So I have to act. I need to keep some money in those two funds as they are closed to new investors like all good funds eventually are. Large size in mutual funds is detrimental to performance. Good managers call a halt to the inflows at some point.

My mother and brother went to see a potential money manager yesterday. Got the info he sent on fees and performance of managers he outsources to. We know this guy from his previous job with Citibank. Could be good.... need to hear more details from them on what they discussed.

Anyway, have assembled a pile of US dollars in my HSBC account and tomorrow will transfer them to Australia. The Australian Dollar has been falling sharply this month. Ostensibly because the Fed is going to raise interest rates much more than the Reserve Bank of Australia will. I have saved $A15,000 so far this month, but am down in US Dollar terms as a result. So at least make lemonade from lemons and try to buy more Aussie Dollars cheap... They will then go to paying down my margin loan in Aus. Last night I sent a fax to my broker in Aus to withdraw $A8000 from two Aussie mutual funds and put that towards margin loan reduction. The Australian All Ords index reached the magical 5000 mark for the first time. My technical analysis model is "flashing" a sell signal. So I have to act. I need to keep some money in those two funds as they are closed to new investors like all good funds eventually are. Large size in mutual funds is detrimental to performance. Good managers call a halt to the inflows at some point.

My mother and brother went to see a potential money manager yesterday. Got the info he sent on fees and performance of managers he outsources to. We know this guy from his previous job with Citibank. Could be good.... need to hear more details from them on what they discussed.

Wednesday, March 22, 2006

Thursday, March 16, 2006

Daytrading vs. Savings Accounts

Stealthbucks commented that he was curious that so many personal finance bloggers seem really excited about savings accounts from Emigrant Bank, ING, HSBC etc that are offering interest rates in the 4-5% range. don't get me wrong, I recently opened such an account with HSBC. With interest rates higher than they were a few years ago it makes sense to park cash temporarily in such an account. And for those just starting out on the saving and investing journey it makes sense to do this before taking the plunge into more sophisticated investments. Also I have long had a Cash Management Trust account (a Money Market account in American) with Adelaide Bank in Australia (and Macquarie Bank before that).

What is stunning though is comparing my recent day-trading with such a savings account. I have really improved my performance and I hope this keeps up... I am still kind of skeptical. I was always skeptical in the past of people who claimed such high rates of return... It so goes against everything taught in finance theory too... The key is risk control combined with excellent pattern recognition and letting winners run.

Anyway, basically I am taking $10,000 and then using daytrading buying power I can borrow $30,000 extra. If I make 1% in a day's trading as I mentioned in a previous post I have made $400 on the $10,000. Today I made $600. You can't expect to make money every day wins and losses have to average out. But that is a 4% rate of return in one day! if you put the $10,000 in a savings account you get 4% in one year!

Maybe there is something wrong here? Of course this is a reward to skill rather than to capital. If you randomly make daytrades even with stops you will lose money. If you got caught in the huge downdraft in GOOG a couple of weeks back you could have lost $7000 of your $10000 in a few minutes. Even with a stop in place the loss would likely be in the thousands due to the extreme rapidity of the collapse. So you only want to put a fraction of your total capital on the line and keep packing profits back into other investments (as well as spending and taxes). This is the risk control strategy of most professional traders. I first read the ideas in Teresa Lo's writing.

What is stunning though is comparing my recent day-trading with such a savings account. I have really improved my performance and I hope this keeps up... I am still kind of skeptical. I was always skeptical in the past of people who claimed such high rates of return... It so goes against everything taught in finance theory too... The key is risk control combined with excellent pattern recognition and letting winners run.

Anyway, basically I am taking $10,000 and then using daytrading buying power I can borrow $30,000 extra. If I make 1% in a day's trading as I mentioned in a previous post I have made $400 on the $10,000. Today I made $600. You can't expect to make money every day wins and losses have to average out. But that is a 4% rate of return in one day! if you put the $10,000 in a savings account you get 4% in one year!

Maybe there is something wrong here? Of course this is a reward to skill rather than to capital. If you randomly make daytrades even with stops you will lose money. If you got caught in the huge downdraft in GOOG a couple of weeks back you could have lost $7000 of your $10000 in a few minutes. Even with a stop in place the loss would likely be in the thousands due to the extreme rapidity of the collapse. So you only want to put a fraction of your total capital on the line and keep packing profits back into other investments (as well as spending and taxes). This is the risk control strategy of most professional traders. I first read the ideas in Teresa Lo's writing.

Wednesday, March 15, 2006

$A400,000

Looks like I just went over $A400,000 in net worth... Three hundred thousand US Dollars remains elusive though due to the weakness in the Aussie Dollar. Did some GOOG daytrading again today - made money but could have done a lot better by just holding onto my position from the beginning of the day to the end. The stock soared when a judge released a fairly favorable opinion on the case between DoJ and Google. I sold into that spike and then did a couple of bad trades before buying into the final upswing of the day and selling 70 of my 100 shares at the close. Using daytrading buying power that allows additional intraday borrowing is on the one hand dangerous on the other hand it imposes discipline to close overly large positions by the end of the day.

Also am almost finished Mark Tier's book "Becoming Rich". Don't be put off by the title and somewhat self-helpy style. It really is an excellent book on developing an investing/trading philosophy. Of coruse there are some contradictions here and there in some of the things he said. The key messages are a delineation of the the main components of master investors' systems - primarily Buffett and Soros are discussed and finding where you have an edge in investing and focus on that just as the masters do. In my strategy I don't any more try to pick what I call "industrial stocks" for long term investment. I can see what is a lousy firm to invest in but don't know what is neccesarily the best opportunity. I focus instead on:

1. Picking good managers for long-term investment

2. Using my knowledge of macroeconomics etc. to try to time the market

3. Use my knowledge of time series analysis, pattern recognition etc. to do short-term trading.

Some people are good at real estate, some in the stock market etc. There isn't anything you have to invest in, despite what people commonly say. If you can't see where you have an edge then focus on finding good managers and advisers. Easterling's book which I completed reading mainly drives home the point that you need a very long term horizon for passive index style investing to work for you. If you are in your 20s and don't want to retire till 60 at least you will probably do fine (but could do better). Dollar cost averaging will help you. Rebalancing and bond strategies the book discusses will help more. But if your time horizon is 10-20 years you may need something more radical given the probable secular bear market that we are in....

Also am almost finished Mark Tier's book "Becoming Rich". Don't be put off by the title and somewhat self-helpy style. It really is an excellent book on developing an investing/trading philosophy. Of coruse there are some contradictions here and there in some of the things he said. The key messages are a delineation of the the main components of master investors' systems - primarily Buffett and Soros are discussed and finding where you have an edge in investing and focus on that just as the masters do. In my strategy I don't any more try to pick what I call "industrial stocks" for long term investment. I can see what is a lousy firm to invest in but don't know what is neccesarily the best opportunity. I focus instead on:

1. Picking good managers for long-term investment

2. Using my knowledge of macroeconomics etc. to try to time the market

3. Use my knowledge of time series analysis, pattern recognition etc. to do short-term trading.

Some people are good at real estate, some in the stock market etc. There isn't anything you have to invest in, despite what people commonly say. If you can't see where you have an edge then focus on finding good managers and advisers. Easterling's book which I completed reading mainly drives home the point that you need a very long term horizon for passive index style investing to work for you. If you are in your 20s and don't want to retire till 60 at least you will probably do fine (but could do better). Dollar cost averaging will help you. Rebalancing and bond strategies the book discusses will help more. But if your time horizon is 10-20 years you may need something more radical given the probable secular bear market that we are in....

Credit Scores

Good article by David Bach on credit scores. I don't like a lot of what this guy writes, particularly on housing, but seems there is a lot of sense in this article. Some of the people playing the credit card arbitrage game should read this and learn more. I fell into some of these traps without knowing. Am not planning on buying a house till 2009-10 at the earliest so hopefully can clean things up by then. Hopefully my balance sheet will be taken into account too!

PS: A whole new credit scoring system was announced today by the three major agencies.

PS: A whole new credit scoring system was announced today by the three major agencies.

Sunday, March 12, 2006

Trade Analysis

Most people probably don't analyse their investment performance as much as I do. My motives are to find what works and see whether I can viably some day be self-employed as a trader-investor. Over time my investments have made money and beaten the relevant indices while my trading has lost me money. The question is: Am I improving? and: Which kind of trades are profitable for me?

Using the spreadsheets that I set up for the Schedule D of my tax returns in the last two years I computed the rate of return on each trade held for less than a year - just gain or loss divided by cost of investment. Overall I found that there was a negative correlation between period held and rate of return! Looking at just day trades they on average returned 0.78%. Those this year have averaged 1% and there is a correlation of 0.33 between date of trade and rate of return. So I am profitable and learning on day trades.

I am usually trading about $30000 or 10% of my net worth on each day trade. A 1% rate of return is $300 per day or $75000 a year which is my current salary. So if I can maintain that over time (this sample is just 42 day trades), it would be a viable occupation.

Longer trades lost money. However, when I excluded the worst two trades that happened last year, the return was a little greater than 1%. The correlation with date was zero. So I am not learning there... but if I can exclude these worst disasters by setting some kind of wide stop on trades I should be able to make money on that too.

I also separated out option trades. These also lost money. But excluding the three worst where the option expired worthless they earned close to 2%. Key here also seems to hold for a short period, though probably more than a day. I have never day traded an option.

If you are an active trader have you tried analysing your trades? It's one good use to put the Schedule D to!

Using the spreadsheets that I set up for the Schedule D of my tax returns in the last two years I computed the rate of return on each trade held for less than a year - just gain or loss divided by cost of investment. Overall I found that there was a negative correlation between period held and rate of return! Looking at just day trades they on average returned 0.78%. Those this year have averaged 1% and there is a correlation of 0.33 between date of trade and rate of return. So I am profitable and learning on day trades.

I am usually trading about $30000 or 10% of my net worth on each day trade. A 1% rate of return is $300 per day or $75000 a year which is my current salary. So if I can maintain that over time (this sample is just 42 day trades), it would be a viable occupation.

Longer trades lost money. However, when I excluded the worst two trades that happened last year, the return was a little greater than 1%. The correlation with date was zero. So I am not learning there... but if I can exclude these worst disasters by setting some kind of wide stop on trades I should be able to make money on that too.

I also separated out option trades. These also lost money. But excluding the three worst where the option expired worthless they earned close to 2%. Key here also seems to hold for a short period, though probably more than a day. I have never day traded an option.

If you are an active trader have you tried analysing your trades? It's one good use to put the Schedule D to!

Saturday, March 11, 2006

Leverage

Some posters on NetWorthIQ have criticized my use of margin or said: "well it's not for me - good luck". Leverage through margin loans, options etc. as well as funds that have built in leverage is both dangerous and useful. It needs to be used judiciously. In today's markets I don't think you want to buy stocks for the long-term on margin. That worked in the 1980s and 90s but expected rates of return are just not good enough now. But when the market is in rally mode as it was from late 2002 to 2004 or 2005 depending on the index some leverage can add to returns. In Australia the standard model is to set the loan so the interest equals the dividend earned and then you are basically looking for capital appreciation and in Aus. surplus tax credits from the dividends (unfortunately the US still has double taxation of dividends instead). Margin also allows you to short either to hedge your long holdings or to speculate which should be done cautiously. At the moment I am using little and fluctuating margin depending on what trades I am doing. Soros' model was to invest one's net worth in longer term investments and then borrow a little against it to trade which is roughly what I am doing at the moment.

However, if the market should crash I would then have a lot of reserve firepower to buy stocks cheap... that is something to think about. You don't have to use a margin facility just because you have it.

What I certainly will do then is move most of my mutual funds and retirement funds from the bond dominated diversified funds they are currently in to a fund called CFS Geared Share Fund which is a leveraged stock fund. Rydex provides somewhat similar products in the US. The difference is the CFS fund is actively managed and Rydex is an index product.

However, if the market should crash I would then have a lot of reserve firepower to buy stocks cheap... that is something to think about. You don't have to use a margin facility just because you have it.

What I certainly will do then is move most of my mutual funds and retirement funds from the bond dominated diversified funds they are currently in to a fund called CFS Geared Share Fund which is a leveraged stock fund. Rydex provides somewhat similar products in the US. The difference is the CFS fund is actively managed and Rydex is an index product.

Friday, March 10, 2006

Bullish Percentage

Yeah, I am getting bashed in the markets, giving up profits I made earlier this and last month, though as only a fraction of my net worth is in trading and most is in fairly conservative at the moment long-term investments the overall damage is not too severe.

Another interesting indicator I follow is the Bullish Percentage. This one is for the NASDAQ 100 index. It tracks what percentage of the point and figure charts of the stocks in the index in the question currently yield bullish recommendations. It is read in a contrarian fashion. When most charts look bullish according to the P&F methodology the market is overbought and will fall. This shows that P&F is mostly not a very useful methodology except used very carefully and differently, for example, in this way...

Another investment book arrived yesterday from Amazon. This one is by Mark Tier. Glanced through - a little "self helpy" but pretty useful I think. More later on this when I have read it. First need to read more of Easterling which I have started.

Another interesting indicator I follow is the Bullish Percentage. This one is for the NASDAQ 100 index. It tracks what percentage of the point and figure charts of the stocks in the index in the question currently yield bullish recommendations. It is read in a contrarian fashion. When most charts look bullish according to the P&F methodology the market is overbought and will fall. This shows that P&F is mostly not a very useful methodology except used very carefully and differently, for example, in this way...

Another investment book arrived yesterday from Amazon. This one is by Mark Tier. Glanced through - a little "self helpy" but pretty useful I think. More later on this when I have read it. First need to read more of Easterling which I have started.

Thursday, March 09, 2006

McClellan Summation

Just was checking out the McClellan Oscillator and Summation as I do most days. One of the most powerful tools for medium term trades of the indices and determining overall direction in the markets. At the moment the oscillator is getting pretty extreme to the downside showing a short-term bottom in the market is near. Did several trades today, ending with my Ameritrade account more to the long-side. Only one short now. I don't post all my trades here by any means. Just a few to explain my thinking on investing and trading.

I am expecting the markets to rally here till the end of the month. Based on the McOscillator and other technical indicators and looking at a lot of different securities and Elliott Wave Theory. My short term trading is mostly on technicals and the macro picture. A few news stories about individual stocks (like GOOG). But I won't trade if I don't see a good technical set-up as well as the story.

I am expecting the markets to rally here till the end of the month. Based on the McOscillator and other technical indicators and looking at a lot of different securities and Elliott Wave Theory. My short term trading is mostly on technicals and the macro picture. A few news stories about individual stocks (like GOOG). But I won't trade if I don't see a good technical set-up as well as the story.

Wednesday, March 08, 2006

Unexpected Returns

Received the copy of Unexpected Returns by Ed Easterling I ordered from Amazon and started reading. The book looks at longer term cycles in the stock market and the justification for hedge fund type investing instead of buy and hold. Buy and hold works in the long bull markets such as from 1982 to 2000 in the US, but maybe we are now in a protracted sideways bear period as occurred in the 1960s and 1970s and buy and hold could provide dividends and interest but little long term capital appreciation.

Monday, March 06, 2006

IYS

Just bought some shares of "Infrastructure Yield Securities" (IYS.AX). This is listed on the Australian Stock Exchange but is actually a complicated real estate investment. I originally bought some in the IPO in 2000 but had to sell in 2002. They have certain tax advantages. But what is interesting now is that there is an offer to roll up the fund with a final distribution greater than what I just paid. And there should be a scheduled distribution still for this month. Seems an interesting trade. There never was great interest in these securities. Deutsche Bank never managed to issue all of them despite the very high after tax yields they offered. This would qualify for my "core investments" I discussed recently if I didn't think the scheme was soon to be closed. So I am considering this a trade. For my NetWorthIQ pages I am listing this as a stock as that is how it is listed on the exchange.

Moomins

So why the names Moomin Valley and moominoid? The moomins are characters in the books (and other spin-offs) created by the Finnish (but Swedish speaking) author Tove Jansson. They live an idyllic life of leisure and adventure in Moomin Valley. They don't care too much about material things but like a comfortable life. They don't care what other people think about them. They don't appear to do any productive work. They are very open-minded and caring about other creatures they encounter. I seem to have a lot in common with a couple of the characters and I guess my dream is to live a life as happy as that of the moomins.... So the aim of getting rich is not for material benefits but in order to live a life more like that of the moomins :)

Sunday, March 05, 2006

Berkshire Hathaway

I am reading Warren Buffett's annual letter and for a change I like what I see. I also checked the chart of Berkshire stock and maybe now is the time to buy. Both I and my Mom have been Berkshire shareholders but we both sold. I needed the money during my 2002 financial crisis and my Mom sold all her shareholdings in individual stocks after my father died.

Berkshire is the kind of stock that I am beginning to collect for a core portfolio, the aim of which is quality assets which shouldn't fluctuate too much with the stock market and can be held indefinitely for tax effective income and long-term capital gains and don't need to be traded in and out of with market conditions. Another recent buy was Clime Capital in Australia (CAM.AX). The manager of that firm - whom I met and actually applied for a job with - is a Buffett worshipper. It is basically a closed end fund and he is doing well so far with his portfolio but the stock price is far below NTA. The price has gone up since I bought. Other assets in this class I own are:

Loftus Capital (LCP.AX) - current strategy is to be a micro size down under version of AMG

Platinum Capital (PMC.AX) - effectively a listed global long-short hedge fund

Everest Brown Babcock (EBB.AX) - a security that includes a 30% share of a manager of funds of hedge funds and a share in such a portfolio of hedge funds

Challenger Infrastructure Fund (CIFCA.AX) - invests in infrastructure including gas pipelines, broadcast towers, and now bidding on a ports deal all in the UK.

All these except PMC.AX are trading below NTA.

Another thing that all these businesses have in common is that the managers have significant stakes in the shares. This is of course true of Berkshire too. Berkshire is likely undervalued relative to the assets it holds.

The TIAA Real Estate Fund might also fall into this class. At least I am thinking of it in that way.

All of them only constitute about 14% of net worth at the moment.

I am looking to add more of these type of investments in any upcoming market downturn.

Berkshire is the kind of stock that I am beginning to collect for a core portfolio, the aim of which is quality assets which shouldn't fluctuate too much with the stock market and can be held indefinitely for tax effective income and long-term capital gains and don't need to be traded in and out of with market conditions. Another recent buy was Clime Capital in Australia (CAM.AX). The manager of that firm - whom I met and actually applied for a job with - is a Buffett worshipper. It is basically a closed end fund and he is doing well so far with his portfolio but the stock price is far below NTA. The price has gone up since I bought. Other assets in this class I own are:

Loftus Capital (LCP.AX) - current strategy is to be a micro size down under version of AMG

Platinum Capital (PMC.AX) - effectively a listed global long-short hedge fund

Everest Brown Babcock (EBB.AX) - a security that includes a 30% share of a manager of funds of hedge funds and a share in such a portfolio of hedge funds

Challenger Infrastructure Fund (CIFCA.AX) - invests in infrastructure including gas pipelines, broadcast towers, and now bidding on a ports deal all in the UK.

All these except PMC.AX are trading below NTA.

Another thing that all these businesses have in common is that the managers have significant stakes in the shares. This is of course true of Berkshire too. Berkshire is likely undervalued relative to the assets it holds.

The TIAA Real Estate Fund might also fall into this class. At least I am thinking of it in that way.

All of them only constitute about 14% of net worth at the moment.

I am looking to add more of these type of investments in any upcoming market downturn.

Saturday, March 04, 2006

Income and Expenditure

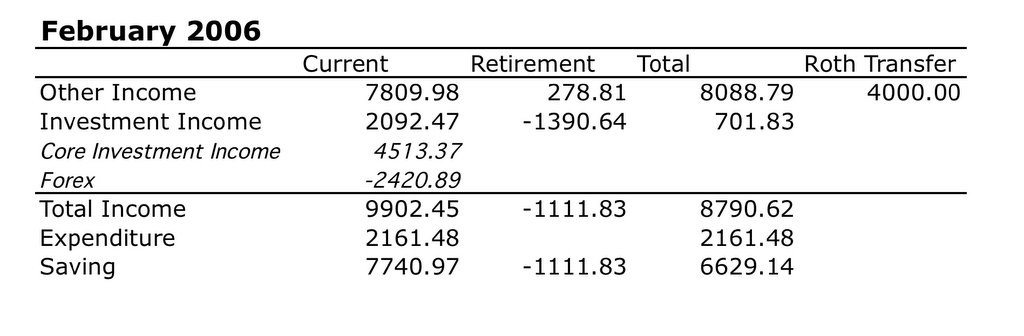

The table shows my income, expenditure, and saving for February. "Other income" includes salary and this month, for example, my expected IRS refund. Retirement "other income" are the contributions to my 403(b). I also contributed $4000 to my new Roth IRA which is a transfer from current savings to retirement savings and so isn't counted under retirement income which are pre-tax contributions. Investment income for current assets is broken down into the core investment earnings - realised and unrealised capital gains, dividends, and net interest etc - and foreign currency movements. The final total saving figure should equal the change in my net worth.

The key thing is my savings rate is around 75% from total income this month. This really is the trick to building net worth fast. Of course, there have been months when total income is negative, so this isn't neccessarily a very typical figure, but certainly not unusual.

Unlike some bloggers out there I don't work hard at avoiding spending. I am single and live in a cheap area. My rent is only $600 in the nicest building in my downtown. I don't own a car. I am naturally pretty frugal I think. Things I focus on more are trying to increase investment income and maximizing tax efficiency.

I probably don't really NEED to save much aside from those 403(b) contributions in my particular circumstances. My dream is though to get to independently wealthy status earlier than I otherwise would.

Friday, March 03, 2006

Alpha and Beta

Just updating my spreadsheets ready for March which includes reporting on performance etc. I keep track of the two best known parameters in modern portfolio theory - alpha and beta. The chart shows my alpha and beta estimated over the 36 months preceding each data point. So March 2006's data point is based on a regression from April 2003 to March 2006 on monthly data. The regression compares my portfolio performance to my MSCI World Index benchmark. Alpha is reported as the annual risk adjusted rate of return by which I exceed the benchmark index.

The interesting thing about this is that recently my alpha has been very positive - i.e. adjusted for risk I easily beat the market. The other interesting thing is that alpha is rising over time. This is a beautiful example of a learning curve :)

Another Wild and Wooly Day

In trade in Google stock. I was long and added shares before the big run up and then was short when it started to fall. Couple of missteps since and ended the day short 50 shares and my Ameritrade account up $1600 or so. This chart is from the Ameritrade Streamer:

Thursday, March 02, 2006

February Investment Performance

Calculated my investment return in February: a measly 0.24%. But the MSCI World Index (Gross including before tax reinvested dividends - which is the benchmark I measure myself against) was down 0.11%. So I beat the index (not unusual...). My performance was mainly affected negatively by the fall in the Australian Dollar over the month. In Aussie Dollar terms I was up 2.14%. The biggest positive contributer was trading in Google. The net result of everything else was a slight negative (before foreign currency adjustment).

Wednesday, March 01, 2006

A Very Different Day

Today the stockmarket has been very volatile and in particular GOOG and the rest of the internet sector. I went into the day short GOOG and shorted more. Initially the stock went against me. But then it just collapsed - amazing to see. The CFO said something negative about growth. I didn't get the full down move. I bought to cover more than $10 from the bottom. Since then I have been doing a rapid succession of long and short trades and am up thousands of dollars on the day. Most daytrading days are not like this. This is very unusual! If I had been long it would have been disastrous - even with a stop in place it might take a while to fill while the stock was falling dollars per minute...

Most of my other positions are down so I am up about $2000 on my Ameritrade account at this point in the day...

It's the end of the month and in the next few days I will work out my accounts and investment performance for February. More on that then. Looks like I am now $24,000 towards this year's net worth goal.

Most of my other positions are down so I am up about $2000 on my Ameritrade account at this point in the day...

It's the end of the month and in the next few days I will work out my accounts and investment performance for February. More on that then. Looks like I am now $24,000 towards this year's net worth goal.

Tuesday, February 28, 2006

More daytrading and mutual funds

Today I did a couple more GOOG trades. Buying 80 GOOG, selling 100, shorting 80 and then buying back 50. So I ended the day short 30 GOOG. The first trade made about $180 and the second lost about $20. This is pretty typical of daytrading I think. Trading tens of thousands of dollars of stock for a couple of hundred dollars gain. Nothing glamorous. But if you worked at it every day and made $200 a day, that is $50,000 a year... I trade purely on technical analysis. A mixture of my own proprietary indicator, the basic indicators any charting program gives you - stochastics, MACD etc. - and Elliott Wave and traditional pattern based TA. You have to synthesize all that data together.

On mutual funds, yesterday I downloaded the last few months of prices for several funds in the Australian funds family I am invested in (Colonial First State). I analyse the funds I actually own plus some others I might think of buying. The analysis includes looking at how they perform in up and down markets, a correlation analysis, and a crude estimate of "alpha".

The correlation analysis is just the correlations computed using Excel of their daily rates of return over a five year period. To compute alpha, I regress the daily returns of each fund on the returns of their Diversified Fund.

Most of the funds I tested with the exception of their "High Growth Fund" have positive alpha relative to the Diversified Fund - i.e. adjusted for risk they outperform it. I don't even bother analysing their international stock funds. Those are so lousy it isn't even worth it - they are a top manager of Australian and resource stocks but not of general international stocks.

The update pretty much confirmed my previous analysis that the Future Leaders, Developing Companies, and Global Resources Fund have a relatively low correlation to each other and to the Conservative, Diversified, Imputation, and Geared Funds. The Geared Share Fund borrows on margin to buy Australian Shares and otherwise is pretty similar to the Imputation Fund. The Conservative Fund is 30% stock and 70% bonds and cash. These four funds are fairly highly correlated with each other and Conservative, Geared, and Imputation outperform Diversified. Therefore, my market timing strategy includes having the core of my portfolio in either the Geared Share or Conservative Fund and maintaining positions in Future Leaders, Developing Companies, and Global Resources for diversification purposes.

I perform a similar analysis also on my TIAA-CREF funds. Currently I hold CREF Bond Market and TIAA Real Estate in my 403(b). Neither has a high correlation with each other or much correlation with the general stock market or my own performance.

My own performance using monthly data has about a 50% correlation with the MSCI global index and in the last three years strong and increasing alpha. This is good news it shows I am improving in skill. Maybe if I could be bothered I could be a hedge fund manager :)

On mutual funds, yesterday I downloaded the last few months of prices for several funds in the Australian funds family I am invested in (Colonial First State). I analyse the funds I actually own plus some others I might think of buying. The analysis includes looking at how they perform in up and down markets, a correlation analysis, and a crude estimate of "alpha".

The correlation analysis is just the correlations computed using Excel of their daily rates of return over a five year period. To compute alpha, I regress the daily returns of each fund on the returns of their Diversified Fund.

Most of the funds I tested with the exception of their "High Growth Fund" have positive alpha relative to the Diversified Fund - i.e. adjusted for risk they outperform it. I don't even bother analysing their international stock funds. Those are so lousy it isn't even worth it - they are a top manager of Australian and resource stocks but not of general international stocks.

The update pretty much confirmed my previous analysis that the Future Leaders, Developing Companies, and Global Resources Fund have a relatively low correlation to each other and to the Conservative, Diversified, Imputation, and Geared Funds. The Geared Share Fund borrows on margin to buy Australian Shares and otherwise is pretty similar to the Imputation Fund. The Conservative Fund is 30% stock and 70% bonds and cash. These four funds are fairly highly correlated with each other and Conservative, Geared, and Imputation outperform Diversified. Therefore, my market timing strategy includes having the core of my portfolio in either the Geared Share or Conservative Fund and maintaining positions in Future Leaders, Developing Companies, and Global Resources for diversification purposes.

I perform a similar analysis also on my TIAA-CREF funds. Currently I hold CREF Bond Market and TIAA Real Estate in my 403(b). Neither has a high correlation with each other or much correlation with the general stock market or my own performance.

My own performance using monthly data has about a 50% correlation with the MSCI global index and in the last three years strong and increasing alpha. This is good news it shows I am improving in skill. Maybe if I could be bothered I could be a hedge fund manager :)

Sunday, February 26, 2006

Tax Day

8:30pm

Decided to do my tax returns today... I do them myself and use Excel to keep records and calculate. This year I added to my spreadsheet, worksheets for each of the six federal tax forms I need (1040, A, B, C, D, and 4952). Took about 4 hours to do the federal form. Most of the work is done by record keeping on those spreadsheets throughout the year, which I improve from year to year. So why learn Quicken or something? My expected federal refund is $3745 - about double last year. I'm including the expected refund in my net worth from today. I don't count my implicit tax assets and liabilities though as it is too much hassle to calculate.... and the value is uncertain depending on future tax rates, AMT etc....

Something interesting was figuring whether I needed to do the form 6251 for the AMT. If I had managed to reduce my tax bill by about another $3000 I would have to fill that form. $10000 of mortgage interest and property taxes would about do the trick I figure... That's not a very expensive property.

Now about to have dinner and then do my state return which should be pretty quick.

11:25pm

OK done my state tax now - no spreadsheet needed just the calculator on my Mac and my federal return....

I ended up owing the state government $5.92 :(

That is the first time in my life that I have had to pay any government rather than get a refund!

Decided to do my tax returns today... I do them myself and use Excel to keep records and calculate. This year I added to my spreadsheet, worksheets for each of the six federal tax forms I need (1040, A, B, C, D, and 4952). Took about 4 hours to do the federal form. Most of the work is done by record keeping on those spreadsheets throughout the year, which I improve from year to year. So why learn Quicken or something? My expected federal refund is $3745 - about double last year. I'm including the expected refund in my net worth from today. I don't count my implicit tax assets and liabilities though as it is too much hassle to calculate.... and the value is uncertain depending on future tax rates, AMT etc....

Something interesting was figuring whether I needed to do the form 6251 for the AMT. If I had managed to reduce my tax bill by about another $3000 I would have to fill that form. $10000 of mortgage interest and property taxes would about do the trick I figure... That's not a very expensive property.

Now about to have dinner and then do my state return which should be pretty quick.

11:25pm

OK done my state tax now - no spreadsheet needed just the calculator on my Mac and my federal return....

I ended up owing the state government $5.92 :(

That is the first time in my life that I have had to pay any government rather than get a refund!

Saturday, February 25, 2006

Daytrading

Some times I do a daytrade for fun. Today I traded Google. Bought 70 shares alongside the 30 I already had and then at the end of the day I sold 80 for a small profit. There were a couple of opportunities during the day to make a few hundreds of profit and I missed them :( Oh well, at least I ended up by a few tens of dollars...

The money for the trade was borrowed on margin using "day-trading buying power". This means you have to close the trade by the end of the day or get a margin call... so it really is pretty much educated gambling on how fast the stock will move in the direction you expect.

The money for the trade was borrowed on margin using "day-trading buying power". This means you have to close the trade by the end of the day or get a margin call... so it really is pretty much educated gambling on how fast the stock will move in the direction you expect.

Friday, February 24, 2006

Americans' Net Worth Trends

This article shows just how unusual most of the posters on NetWorthIQ who have multiple entries are:

http://money.cnn.com/2006/02/23/pf/consumer_fedsurvey/index.htm

Most show strongly rising net worth. However the median of all posters at $79500 is not that far from the national median of $93000. It is pretty obvious that people making an effort to increase their net worth are the types to track their progress on such a website...

http://money.cnn.com/2006/02/23/pf/consumer_fedsurvey/index.htm

Most show strongly rising net worth. However the median of all posters at $79500 is not that far from the national median of $93000. It is pretty obvious that people making an effort to increase their net worth are the types to track their progress on such a website...

Goals

The net worth goals might seem rather high and they do depend on everything going right.

The goal for this year is based on:

Current savings from salary: $20,000

Retirement contributions: $7,000

Investment returns: $30,000

Inheritance: $20,000 ($7,000 of which has materialized the other is a guess of the value of my share of a land sale)

Exchange rate change: $23,000

I'd be happy with a lot less - say a $50,000 gain instead of the $100,000 gain. But with $16,000 added to net worth so far this year I am right on track for the $100,000 goal.

The decade-end goal is dependent on there being a new stock bull market in 2007-8. This is what I expect based on the four year stock cycle. Based on the 2002-5 bull market I could double whatever wealth I have at the beginning of such a bull market. If that happens, the $1 million goal will not be so hard to achieve.

At the moment I am mainly trying to preserve capital against a potential downturn this year. You have to be very daring and right to make money in a down market...

The goal for this year is based on:

Current savings from salary: $20,000

Retirement contributions: $7,000

Investment returns: $30,000

Inheritance: $20,000 ($7,000 of which has materialized the other is a guess of the value of my share of a land sale)

Exchange rate change: $23,000

I'd be happy with a lot less - say a $50,000 gain instead of the $100,000 gain. But with $16,000 added to net worth so far this year I am right on track for the $100,000 goal.

The decade-end goal is dependent on there being a new stock bull market in 2007-8. This is what I expect based on the four year stock cycle. Based on the 2002-5 bull market I could double whatever wealth I have at the beginning of such a bull market. If that happens, the $1 million goal will not be so hard to achieve.

At the moment I am mainly trying to preserve capital against a potential downturn this year. You have to be very daring and right to make money in a down market...

Trading

Difficult trading environment at the moment. My trading positions are pretty much hedged between long and short at this point. Last night took a hit on my News Corp puts... this morning news from Toll Brothers is good as I am long WLS (William Lyon Homes). Nursing a long Blackrock (after trading it both ways last week). Was expecting a bounce on technicals.... Short SBUX very bad.... Long AAPL, HHH, and GOOG doing great. This morning AAPL announced new product announcements coming on Feb 28. Short DCX has been bad up till the last few days when plenty of analysts downgraded the stock...

On the investment side my current positions are pretty conservative with a bias towards bond mutual funds and listed hedge fund type investments. More on all this at month end.

PS 3pm - bought an extra 100 shares of AAPL

On the investment side my current positions are pretty conservative with a bias towards bond mutual funds and listed hedge fund type investments. More on all this at month end.

PS 3pm - bought an extra 100 shares of AAPL

Thursday, February 23, 2006

This and that

A great blog on the world markets, investment strategy, and China, from one of my old friends at Silicon Investor:

http://worldmarket.blogspot.com/

The Australian Dollar has been going down and foreign currency has a big impact on my net worth calculation. This month so far I am down $US 1,000 but up approximately $A 9,000...

http://worldmarket.blogspot.com/

The Australian Dollar has been going down and foreign currency has a big impact on my net worth calculation. This month so far I am down $US 1,000 but up approximately $A 9,000...

Thursday, February 16, 2006

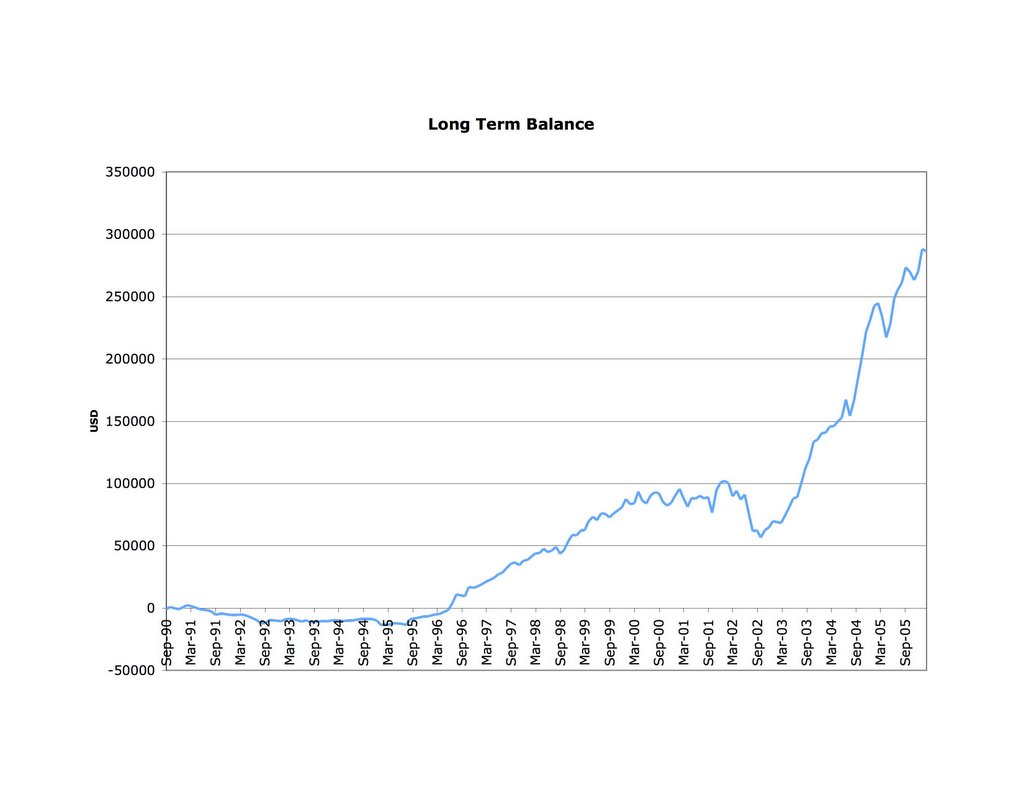

Long Term Net Worth

This chart shows my net worth in the 12 years or so before NetWorthIQ's accounting starts. Starts with a period as a grad student and post doc where I go into and then out of debt and then a gradual increase in the last ten years. Big dip in 2002 due to no employment, a crashing stockmarket and a worldwide job search. Flew more miles that year including two round the world trips in the first three months of the year than I did before or since... Rate of accumulation since moving to the US (in 2002) has been faster than in Australia (1996-2002) where I earned less.

Welcome

This is my blog - I just got it so I can answer other blogs - I will probably occasionally post some personal finance stuff here to complement my profile on NetWorthIQ.

Subscribe to:

Posts (Atom)