In November, the Australian Dollar rose from USD 0.6564 to USD 0.6515. Stock indices and other benchmarks performed as follows (total returns including dividends):

US Dollar Indices

MSCI World Index (gross): 3.77%

S&P 500: 5.87%

HFRI Hedge Fund Index: 1.51% (forecast)

Australian Dollar Indices

ASX 200: 3.96%

Target Portfolio: 2.43% (forecast)

Australian 60/40 benchmark: 2.47%

We gained 5.89% in Australian Dollar terms or 5.10% in US Dollar terms. So we outperformed all benchmarks apart from the S&P 500. This was the best month ever in dollar terms with a return of AUD 332k (previous best 192k in July 2022, 333k in currency neutral terms, previous best 225k in April 2020). In percentage return terms this was only the 16th best month, but the highest since 2015. We simply have a less volatile portfolio these days. We also went over the next million Australian dollar milestone.

The SMSF returned 11.38%, its best performance to date, compared to Unisuper at 1.76% and PSS(AP) at 2.29%. I had to extend the y-axis on the rate of return graph twice:

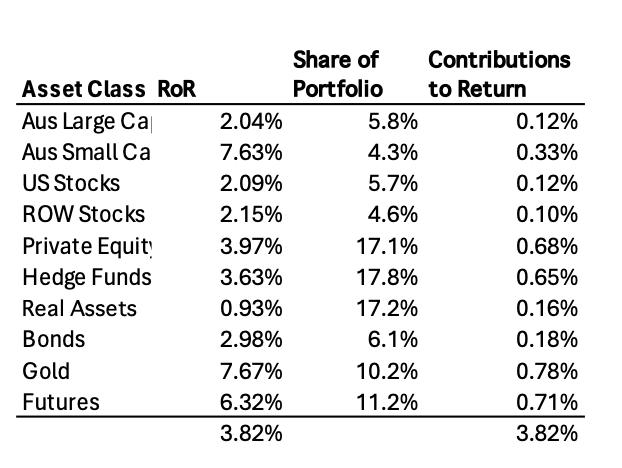

Here is a report on the performance of investments by asset class:

The asset class returns are in currency neutral terms as the rate of return on gross assets and so the total differs from the Australian Dollar returns on net assets mentioned above. RoW stocks (mostly Defi Technologies) and futures (mostly bitcoin) both gained more than 20%. Gold was the only asset class that lost money.

Things that worked well this month:

- Bitcoin and Defi Technologies gained AUD 226k and 182k, respectively. These are 3-4 times more than the biggest monthly gain on an individual investment previously. Also gaining more than AUD 10k were 3i (III.L) at 36k, Pershing Square Holdings (PSH.L) at 29k, PSS(AP) 12k, and Unisuper at 11k.

What really didn't work:

- Gold (-AUD 24k), Tribeca Global Resources (TGF.AX, -20k), and Regal Investment Fund (RF1.AX, -13k) all lost more than AUD 10k.

Here are the investment performance statistics for the last five years:

The top three lines give our performance in USD and AUD terms, while the last three lines give results for three indices. Our performance fell back this month compared to the ASX200 but, as we have much lower volatility, we have a higher Sharpe ratio of 0.93 vs. 0.55. But as we optimize for Australian Dollar performance, our USD statistics are much worse. We do beat the HFRI hedge fund index in terms of return, but at the expense of much higher volatility. We have a positive alpha relative to the ASX200 of 3.97% with a beta of only 0.47.

We moved away our target allocation this month as our bitcoin and Defi Technologies positions grew. We are most underweight cash and most overweight futures. Our actual allocation currently looks like this:

We receive employer superannuation contributions every two weeks. We contribute USD 10k each quarter to the Unpopular Ventures Rolling Fund and less frequently there will be capital calls from Aura Venture Fund II. This month we received tax refunds of AUD 27k. I made the following additional moves this month:

- I paid an AUD 37.5k capital call from Aura.

- I sold 10k shares of Hearts and Minds (HM1.AX).

- I sold 400 shares of the Putnam BDC ETF (PBDC).

- I redeemed AUD 60k of units in the Winton Global Alpha Fund.

- I took part in the Regal Investment Fund (RF1.AX) share purchase plan, buying AUD 30k of shares.

- I bought 500 shares of the Fidelty Bitcoin ETF (FBTC). We now have 5,500 shares, which is close to 5 bitcoins.